The fundamental narrative governing the digital asset ecosystem is undergoing a profound metamorphosis. For the better part of the last decade, stablecoins—predominantly Tether (USDT) and USD Coin (USDC)—served as the lifeblood of the crypto-native economy, acting primarily as liquidity engines for decentralized exchanges, leverage trading, and yield farming. Today, however, that paradigm is shifting toward a utility-first framework. As adoption matures, stablecoins are increasingly being integrated into the plumbing of the traditional financial system, facilitating cross-border remittances, institutional treasury management, and 24/7 global settlement networks.

This transition marks a departure from the "crypto-for-crypto" loop, moving toward a reality where stablecoins function as an efficient, programmable settlement layer for real-world financial activity.

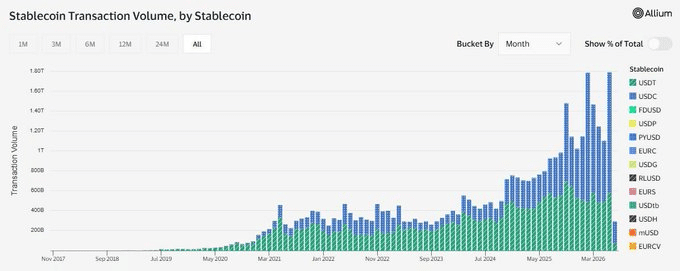

A Record-Breaking June: The Data Behind the Shift

The evidence for this structural pivot is found in the latest market data. According to statistics from Allium, adjusted stablecoin transaction volume soared to a record $1.79 trillion in June. This figure is not merely a statistical anomaly; it represents a staggering 63% increase from May and a 125% year-over-year surge.

This acceleration confirms that market participants are increasingly utilizing stablecoins as a medium of exchange and settlement rather than merely as a parking lot for idle capital during volatile periods. While the broader cryptocurrency market experienced a "risk-off" sentiment, with the total market capitalization contracting by over 18%—the largest monthly outflow since February—stablecoin transactional activity moved in the opposite direction. This divergence suggests that while speculative capital is fleeing the market, utility-driven capital is finding a permanent home within the stablecoin ecosystem.

Chronology: The Evolution of Stablecoin Utility

To understand how we reached this point, it is necessary to examine the trajectory of stablecoin adoption:

- 2017–2020: The Liquidity Provision Era. Stablecoins were largely relegated to centralized and decentralized exchanges (DEXs) to facilitate trading pairs for Bitcoin and Ethereum. Their primary value proposition was providing a "safe haven" during market crashes.

- 2021–2023: The DeFi Expansion. As decentralized finance (DeFi) protocols grew, stablecoins became the foundational collateral for lending, borrowing, and liquidity pools. Their usage was still largely contained within the "walled garden" of the blockchain industry.

- 2024–2025: The Institutional Integration Phase. Major financial institutions began testing stablecoins for treasury management, cross-border payments, and settlement.

- June 2026: The Utility Decoupling. The current data shows a widening gap between market capitalization (total supply) and transaction volume. This indicates that the same dollar of stablecoin is being "recycled" more frequently for actual economic activity rather than sitting dormant in exchange wallets.

Layer 1 Competition: The Race for Settlement Dominance

As stablecoin activity migrates from speculative liquidity to institutional utility, Layer 1 (L1) blockchain networks are vying to become the preferred settlement layers. This has turned the infrastructure layer of crypto into a competitive landscape where network speed, cost, and regulatory compliance determine the winner.

The Open Network (TON) serves as a prime example of this trend. Recent data shows that the native stablecoin supply on the TON blockchain increased by 8% in just one week, surpassing the $810 million mark. This influx is not driven by speculative fervor alone, but by the network’s integration with high-volume messaging platforms, which allows for seamless, user-friendly payments. Other networks, including Solana, Base, and Ethereum, are engaged in similar "stablecoin wars," aggressively courting issuers to host their supply on-chain to attract the massive transaction fees and ecosystem stickiness that accompany these assets.

The Macro Backdrop: Dollar Strength and Global Pressure

The shifting dynamics of stablecoins cannot be viewed in a vacuum; they are inextricably linked to the broader macroeconomic environment. The U.S. Dollar Index (DXY), which tracks the value of the greenback against a basket of foreign currencies, has shown consistent strength, posting back-to-back monthly gains. In June alone, the DXY rose more than 2.25%.

This strength has created a "dollar squeeze" in emerging markets. Currencies like the Japanese Yen have plummeted to multi-decade lows, and other sovereign currencies are struggling to maintain value against the surging dollar. In such an environment, the demand for USD-pegged stablecoins in countries with high inflation or currency volatility acts as a digital safety valve. Users in these regions are increasingly bypassing local banking infrastructure in favor of stablecoins, which provide direct access to the world’s reserve currency.

Implications: A Looming Divergence or a New Normal?

Despite the record transaction volumes, the stablecoin market is facing a contraction in its total market capitalization. Over the past two months, the combined market cap of USDT and USDC has declined by nearly $11 billion.

1. The Contradiction of Usage vs. Liquidity

The fact that stablecoin usage (transaction volume) is hitting all-time highs while market cap (total supply) is shrinking presents a paradox. It suggests that while the "velocity of money" within the crypto ecosystem is increasing, the "on-ramp" of new capital from the traditional financial system is slowing down. This suggests that the current stablecoin ecosystem is being sustained by existing capital circulating more efficiently rather than an influx of fresh fiat currency.

2. Bearish Signals for H2

If this trend of declining market cap persists, it could pose a significant headwind for the crypto market in the second half of the year. Stablecoins serve as the primary "dry powder" for traders. When stablecoin market caps shrink, it implies that capital is being withdrawn from the ecosystem, potentially leading to lower liquidity for major assets like Bitcoin and Ethereum.

3. Institutional Maturity

On the positive side, the shift toward utility implies that the sector is moving toward a more mature, revenue-generating business model. Stablecoin issuers are no longer solely dependent on the "bull market" cycle to thrive. Instead, they are benefiting from a consistent stream of transaction fees generated by real-world payments, remittances, and B2B settlements.

Official and Industry Perspectives

Market analysts remain divided on the long-term impact of this decoupling. Some argue that the decline in market cap is a healthy "deleveraging" event, clearing out the speculative froth that characterized the 2021 bull run. Others warn that the lack of new capital inflow is a "red flag" that could limit the upside for the crypto market during the remainder of 2026.

Regulators, meanwhile, are closely monitoring these trends. The increasing utility of stablecoins in cross-border payments has prompted central banks and international bodies to accelerate the development of Central Bank Digital Currencies (CBDCs) and stricter stablecoin frameworks. The message from the regulatory front is clear: the integration of stablecoins into the global financial system is inevitable, but it must occur within a framework that ensures consumer protection and financial stability.

Conclusion: Navigating the Second Half of 2026

As we look toward the second half of 2026, the stablecoin sector finds itself at a critical juncture. The shift from a liquidity-driven asset class to a utility-driven infrastructure layer is a sign of long-term health and institutional legitimacy. However, the current contraction in total market supply serves as a cautionary tale.

For investors and developers, the key to navigating this environment lies in monitoring the divergence between transaction volume and capital supply. If the current trajectory continues, we may see a market that is more efficient, more useful, and more deeply integrated into the global economy—even if it is temporarily smaller in terms of total dollars held. The "Great Decoupling" is not just a trend; it is the inevitable maturation of a technology that is finally finding its real-world purpose.