The stablecoin landscape—a critical pillar of the global digital asset economy—is undergoing a seismic shift. On June 30, Circle Internet Financial, the issuer of the USD Coin (USDC), saw its stock (CRCL) plummet by 17.5%, closing at $62.63. This sharp correction represents the most significant single-day decline for the company since March, signaling a growing apprehension among investors regarding the future of Circle’s market dominance in an increasingly crowded and institutionalized ecosystem.

While the volatility of the crypto-adjacent stock market is rarely tied to a single event, the timing of this downturn is far from coincidental. It follows the high-profile unveiling of a new, formidable challenger: Open USD (OUSD). Backed by an unprecedented coalition of 140 industry titans—including financial heavyweights like Visa, Mastercard, BlackRock, and Google—OUSD represents a strategic attempt to bridge the gap between traditional finance and decentralized infrastructure.

Main Facts: The Anatomy of a Sell-Off

The 17.5% decline on June 30 was not merely a reaction to market sentiment; it was a response to a fundamental structural shift in the stablecoin sector. The market has become hyper-sensitive to regulatory and competitive developments. In March, Circle faced a similar, though less sustained, downward pressure when a draft proposal suggested a potential ban on stablecoin yield for idle balances. That event sparked fears that USDC’s utility—and consequently, its revenue—would be severely hampered.

However, the late June sell-off was driven by a more tangible threat: the erosion of Circle’s "moat." By introducing a stablecoin that promises zero transfer fees and a profit-sharing model among its 140 partners, the consortium behind OUSD has directly attacked the traditional revenue-generation model that Circle has relied upon for years. For investors, the concern is clear: if institutional adoption shifts toward a collaborative, fee-free model, where does that leave the current leaders, Tether and Circle?

Chronology: From Regulatory Headwinds to the Rise of OUSD

To understand the current state of play, one must look at the timeline of events that have shaped the stablecoin industry since 2025:

- March 2026: Initial regulatory jitters emerge. A draft proposal aimed at restricting yield on idle stablecoin balances causes a 20% drop in CRCL stock, highlighting the market’s fragility regarding legislative interference.

- 2025 (Post-GENIUS Act): The passage of the GENIUS Act creates a more defined, albeit highly competitive, regulatory environment. This framework spurred rapid innovation and attracted legacy financial institutions to the space.

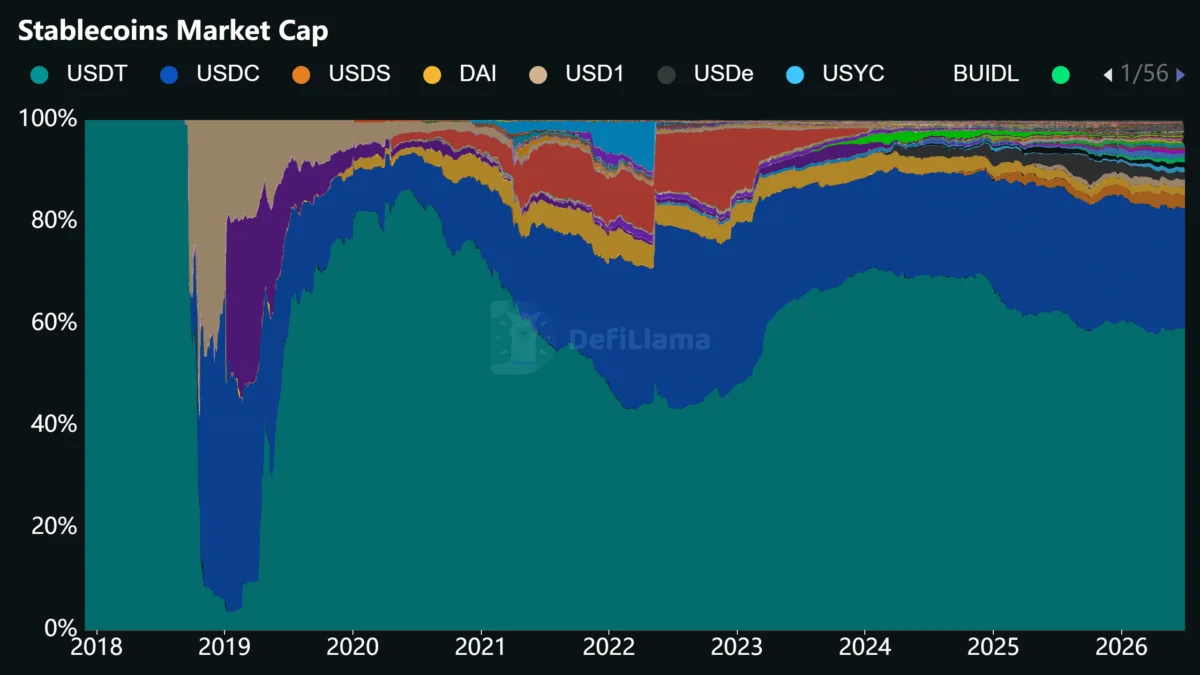

- Early 2026: Tether (USDT) experiences a contraction in market share, falling from 62% to 59%, while Circle (USDC) manages to capture more ground, peaking at a 25% share before stabilizing at 24%.

- Late June 2026: The coalition of 140 firms officially announces the launch of Open USD (OUSD). The market reacts instantly, with Circle’s stock suffering its largest decline since the March incident.

Supporting Data: A Shifting Market Share

The battle for stablecoin supremacy is essentially a battle for liquidity and trust. Data provided by DeFiLlama indicates that the market is currently in a state of flux. Tether, the industry’s long-standing titan, has long held a commanding lead. However, the rise of regulatory clarity following the 2025 GENIUS Act has allowed institutional-grade competitors like Circle to challenge that lead.

Yet, as Circle expanded its footprint—growing its market share from 19% to 25% over the past year—it also painted a target on its back. The introduction of OUSD arrives at a time when the market is clearly cooling on the "issuer-takes-all" model. While Tether remains the dominant force by total market capitalization, its share reduction from 62% to 59% suggests that users and institutions are increasingly willing to diversify their holdings.

Analysts are keeping a close eye on these metrics. While the short-term outlook for CRCL has turned bearish, the long-term consensus remains surprisingly resilient. MarketBeat reports a consensus price target of $120 for Circle’s stock, which implies an approximate 91% upside from current levels. This suggests that while the market is currently factoring in the "OUSD risk," analysts believe the fundamental value of Circle’s infrastructure remains intact.

Official Responses and Expert Analysis

The reaction from industry experts has been swift and largely focused on the existential threat posed by the OUSD consortium. Matthew Sigel, the Head of Digital Research at VanEck, was one of the first to point out the direct correlation between the announcement of OUSD and the slide in Circle’s valuation.

"The backing of OUSD by heavyweights like Stripe, Coinbase, and BlackRock changes the math for everyone," noted Sam Ruskin, an investment associate at Reciprocal Ventures. "This will either force Circle to pivot toward more aggressive revenue-sharing agreements or push them to find entirely new distribution channels. Regardless of the tactical response, the current landscape is undeniably bearish for Circle’s traditional model."

The implication is that the days of stablecoin issuers operating in a vacuum are over. The entry of firms like Visa and Google into the issuance side of the market suggests that stablecoins are transitioning from "crypto tools" to "financial infrastructure."

Implications: What Does This Mean for the Future?

The emergence of OUSD carries three primary implications for the industry:

1. The Death of the "Fee" Model

For years, the business model for stablecoins has been built on interest rate differentials and transaction fees. With OUSD proposing zero transfer fees and a reserve-sharing model, the "profit center" of the industry is under fire. Circle will likely have to innovate beyond its current offerings to remain competitive, perhaps by leaning into B2B financial services or deep integration with enterprise treasury management software.

2. Institutionalization vs. Decentralization

The involvement of BlackRock and Google in OUSD highlights a broader trend: the "Wall Street-ification" of crypto. While this brings legitimacy and scale, it also raises questions about centralization. If 140 firms control a stablecoin, is it still "crypto," or is it simply a new layer of the traditional banking system? This tension will define the narrative for the next decade.

3. The Enterprise Treasury Shift

OUSD is explicitly targeting enterprise treasury management. This is a massive market segment that both USDC and USDT have been trying to penetrate. If corporations decide that a consortium-backed coin is more "stable" or "compliant" than a retail-focused one, we could see a massive migration of capital away from existing stablecoins.

Conclusion: A Turning Point for Circle

Circle finds itself at a critical juncture. The market reaction on June 30 was a wake-up call, signaling that the era of uncontested growth for USDC is ending. Whether Circle can maintain its 24-25% market share in the face of a coalition backed by the world’s largest financial entities will depend on its ability to adapt its product roadmap and perhaps, its fee structure.

While the bearish sentiment is currently dominating the headlines, the 91% upside target suggests that Wall Street still sees potential in Circle. However, the path forward is no longer paved with the ease of early adoption; it is now a battleground of giants. As we move into the latter half of 2026, the question is not just whether Circle can survive, but how the entire stablecoin industry will be redefined by the institutional giants now entering the arena.