The global cryptocurrency landscape is currently navigating a period of profound recalibration. As market volatility remains a defining feature of the digital asset sector, stablecoins—digital assets pegged to fiat currencies—have emerged as the ecosystem’s most resilient pillar. Far from being mere vehicles for speculative trading, stablecoins have evolved into a sophisticated layer of global financial infrastructure, bridging the gap between traditional finance and the nascent world of decentralized digital assets.

Recent data suggests that while the aggressive "bull market" inflows of the past have moderated, the structural demand for stablecoins remains remarkably robust. This shift indicates a maturing market, where liquidity is increasingly being deployed with strategic precision rather than frantic, speculative exuberance.

Main Facts: The Resilience of the Stablecoin Market

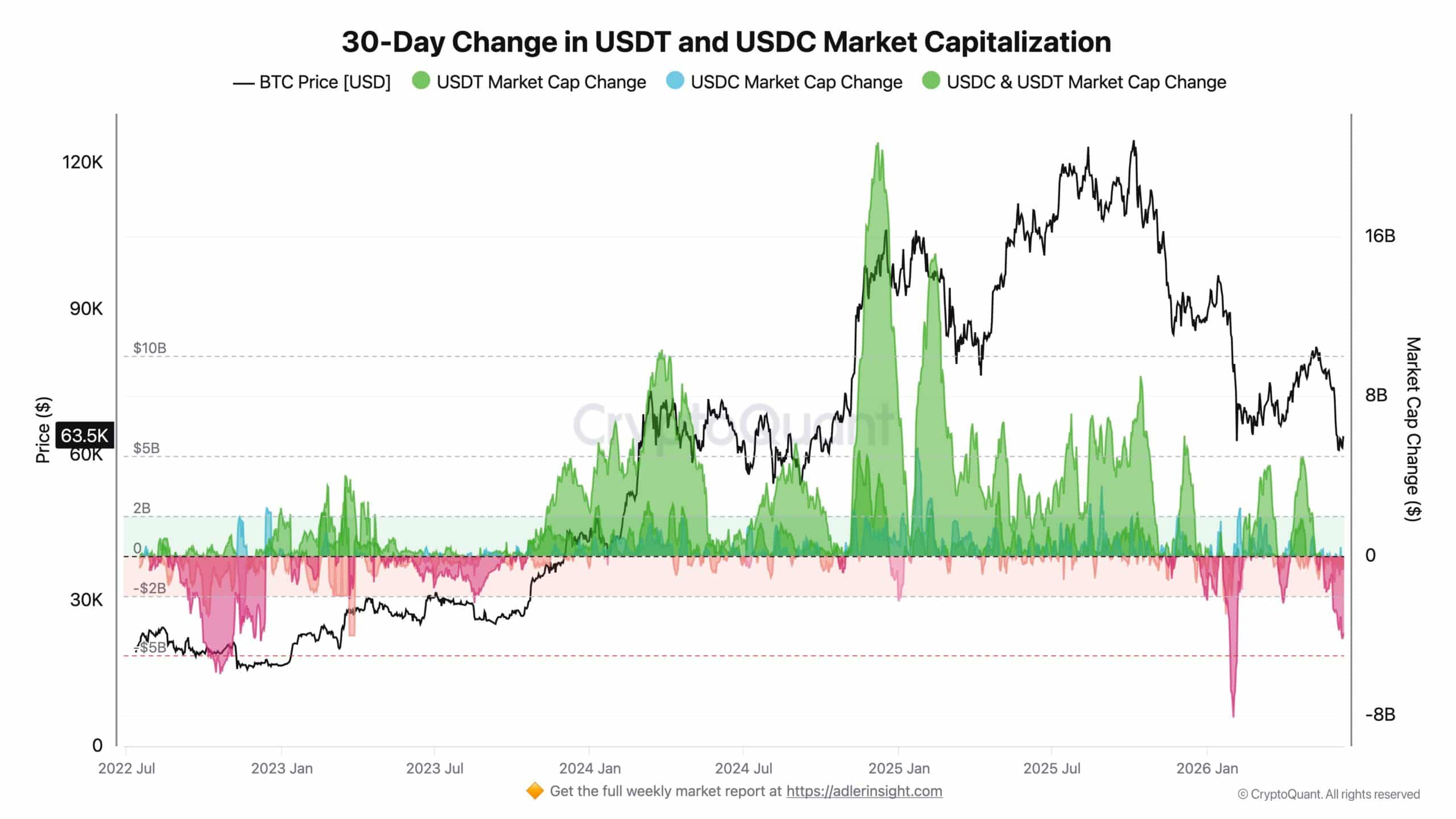

The broader stablecoin market, currently valued at approximately $315 billion, serves as a testament to the enduring utility of these assets. Despite persistent weakness across the wider crypto markets, the supply of major stablecoins—most notably Tether (USDT) and USD Coin (USDC)—has largely stabilized.

Historically, periods of significant crypto-market downturns have often triggered massive capital flights. Earlier in February, the market witnessed monthly liquidity outflows from USDT and USDC approaching $8 billion. However, that figure has since halved, with outflows currently hovering around $4 billion. This deceleration in capital exit suggests that the ecosystem has reached a state of "liquidity equilibrium," where the assets remain parked within the ecosystem, awaiting clearer market signals.

The fundamental value proposition of stablecoins remains unchanged: they provide a reliable, low-volatility medium of exchange that allows investors to navigate the high-beta environment of crypto-assets without exiting the blockchain environment entirely.

Chronology: Tracing the Flow of Capital

To understand the current state of the market, one must look at the historical trajectory of exchange activity.

The Surge Phase

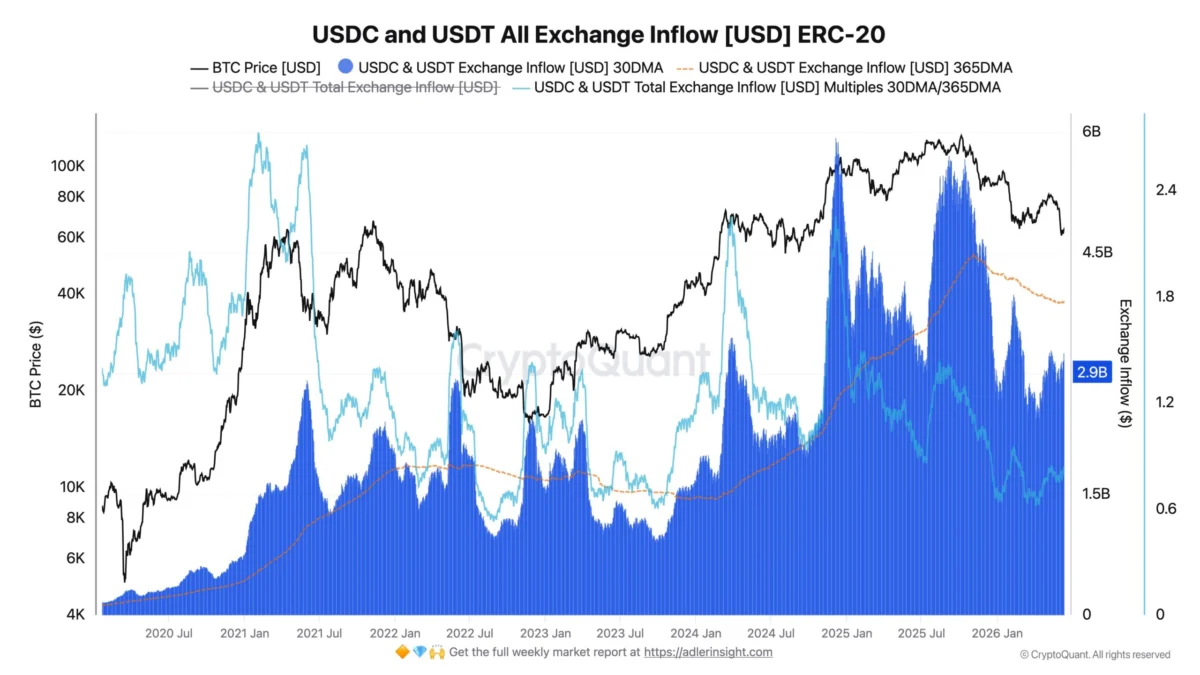

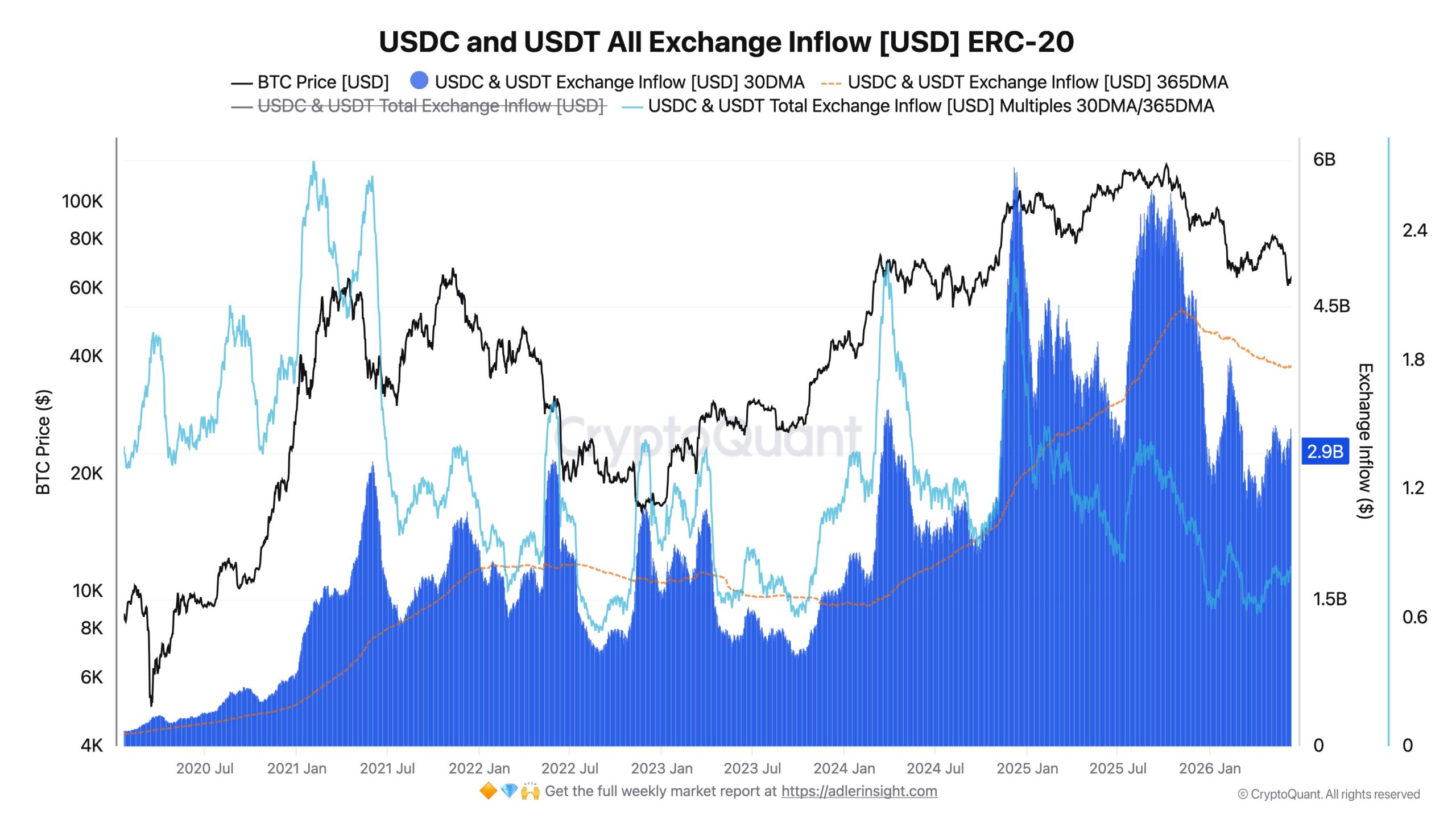

During the market’s most explosive periods, exchanges saw monumental inflows. At the peak of recent cycles, monthly inflows of USDT and USDC surged to as much as $5.7 billion, with 30-day spikes occasionally eclipsing $15 billion. These periods of heavy, consistent inflow historically coincided with Bitcoin’s strongest rallies, as investors funneled capital into stablecoins as "dry powder" to capture further upside.

The Moderation Phase

Following the peak, these inflows began a steady, predictable decline. As market momentum shifted, the urgency to deploy capital waned. Currently, monthly deposits have leveled off at approximately $2.9 billion. Furthermore, the annual average for these inflows has contracted from roughly $4.47 billion to $3.87 billion.

The Current Divergence

The current 0.77 ratio—a metric comparing current inflows against historical averages—highlights a marked slowdown in capital deployment. This is not necessarily a bearish signal; rather, it indicates a shift in investor behavior. Market participants are no longer blindly "chasing risk." Instead, they are demonstrating a more calculated, patient approach to liquidity deployment, keeping their capital in stable assets until the risk-reward profile of volatile assets becomes more attractive.

Supporting Data: Why Liquidity Remains Tethered

The persistence of $315 billion in total stablecoin supply, even amidst lukewarm market performance, serves as a critical indicator of institutional and retail "stickiness." When capital leaves the crypto ecosystem, it typically moves back into traditional fiat banking systems. The fact that the stablecoin supply has not entered a sustained, sharp decline suggests that investors are keeping their funds on-chain, effectively "waiting out" the volatility.

Furthermore, the diversification of stablecoin use cases—beyond pure exchange-based trading—provides a floor for demand. According to recent industry analysis, while exchange inflows have cooled, the volume of stablecoins utilized for cross-border settlements, remittances, and decentralized finance (DeFi) protocols has remained elevated. This implies that even if the "speculative" usage of stablecoins has tapered, the "functional" usage is growing, providing a necessary buffer against broader market downturns.

Institutional Adoption and Regulatory Integration

Perhaps the most significant development in the stablecoin sector is the deepening integration with institutional finance. The "wild west" era of crypto is being rapidly supplanted by an era of regulated, institutional-grade participation.

A landmark example of this shift is the recent SEC approval of the T. Rowe Price Active Crypto ETF. This decision represents a watershed moment: for the first time, a major, traditionally regulated asset manager has received the green light to hold stablecoins as part of its actively managed investment strategy. This move legitimizes stablecoins as a tool for liquidity management and operational efficiency within a highly scrutinized, regulated framework.

This development is not an isolated event. It is part of a broader trend where traditional financial giants are recognizing that stablecoins can optimize portfolio operations, facilitate near-instant settlement, and reduce the counterparty risks associated with legacy banking systems.

Implications: A New Era of Payment Infrastructure

Beyond the world of investment portfolios, stablecoins are aggressively moving into the realm of real-world payments. A recent report from McKinsey underscores a critical reality often overlooked by market analysts: the "real-world" transaction volume for stablecoins reached approximately $390 billion in 2025.

From Trading to Transactions

The implications for this are profound. When a financial asset moves from being a speculative instrument on an exchange to being a payment mechanism for businesses and consumers, it gains an intrinsic, non-speculative value. This transition suggests that stablecoins are effectively becoming the "TCP/IP of money"—the foundational infrastructure upon which a new, faster, and more transparent global payment system is being built.

Reducing Reliance on Speculative Cycles

As businesses adopt stablecoins for payroll, supply chain settlements, and B2B payments, the demand for these assets becomes decoupled from the price fluctuations of Bitcoin or Ethereum. This decoupling is essential for the long-term viability of the digital asset industry. If the utility of stablecoins is tied to their function as a payment rail, then the market value of the sector will eventually be driven by global transaction velocity rather than the sentiment-driven bull and bear markets of crypto-assets.

Conclusion: The Path Forward

The data suggests that the stablecoin market is in a state of healthy, albeit slower, transition. The cooling of exchange inflows is a symptom of a market that has matured past its initial "gold rush" phase. However, the sustained total supply and the increasing integration of stablecoins into regulated ETFs and global payment networks point toward a much larger, more stable future.

For investors, policymakers, and market observers, the takeaway is clear: stablecoins have survived the "hype cycle" and are now entering the "utility cycle." As the ecosystem continues to integrate with traditional finance, stablecoins are no longer just a way to hold cash in a crypto-native way—they are becoming the bedrock upon which the future of global finance is being constructed.

The focus has shifted from how much money is entering the casino to how much utility is being built into the rails. In that regard, the stablecoin market is not just surviving the current crypto weakness; it is quietly preparing for a much larger, more permanent role in the global economy.