In a landmark development that signals the accelerating convergence of traditional banking and the digital asset economy, global financial giant Standard Chartered has announced a strategic partnership with Circle, the issuer of the USD Coin (USDC). This collaboration marks the first time a Global Systemically Important Bank (G-SIB) has integrated direct USDC minting and redemption services into its institutional banking infrastructure. By streamlining the path for institutional capital to enter the stablecoin market, the partnership is poised to fundamentally shift how multinational corporations and financial institutions engage with blockchain-based liquidity.

The Core Partnership: Simplifying Institutional Access

For years, the hurdle for institutional adoption of stablecoins has been the operational complexity of managing digital asset infrastructure alongside legacy banking systems. Previously, institutions wishing to use USDC were required to establish distinct, often siloed relationships directly with Circle, involving separate compliance, KYC/AML procedures, and technical integration layers.

Under the new framework, Standard Chartered is effectively collapsing these silos. By embedding USDC access directly into its institutional banking suite, the bank allows its clients to mint and redeem USDC through existing bank-led rails. This means that an institution can leverage its existing Standard Chartered account to handle the conversion of fiat currency into USDC and vice versa, without the friction of navigating external crypto-native platforms.

The service is launching initially within the Dubai International Financial Centre (DIFC), a strategic move given Dubai’s progressive regulatory environment for virtual assets. Following this initial rollout, the bank plans to expand the service across its global network, potentially opening the door for seamless cross-border stablecoin settlements.

A Chronology of the Stablecoin Evolution

The path to this partnership did not happen overnight; it represents the culmination of a multi-year shift in how global financial institutions perceive digital assets.

- 2020–2022: The "Niche" Phase: Stablecoins were largely viewed as instruments for crypto-native traders, used primarily for liquidity on centralized exchanges or for participation in Decentralized Finance (DeFi) protocols. During this period, major global banks maintained a cautious "wait-and-see" approach.

- 2023: The Regulatory Thaw: As jurisdictions like the UAE, the European Union (with its MiCA framework), and parts of Asia began clarifying stablecoin regulations, institutional interest pivoted from curiosity to operational strategy.

- Mid-2024: Infrastructure Development: Standard Chartered began quietly building out its digital asset custody and service layers, preparing to move beyond mere "crypto-friendly" banking into active participation in the stablecoin lifecycle.

- July 2026: The Milestone: The formal announcement of the partnership confirms that the infrastructure is now production-ready. The move signifies a transition from experimental pilot programs to full-scale institutional integration.

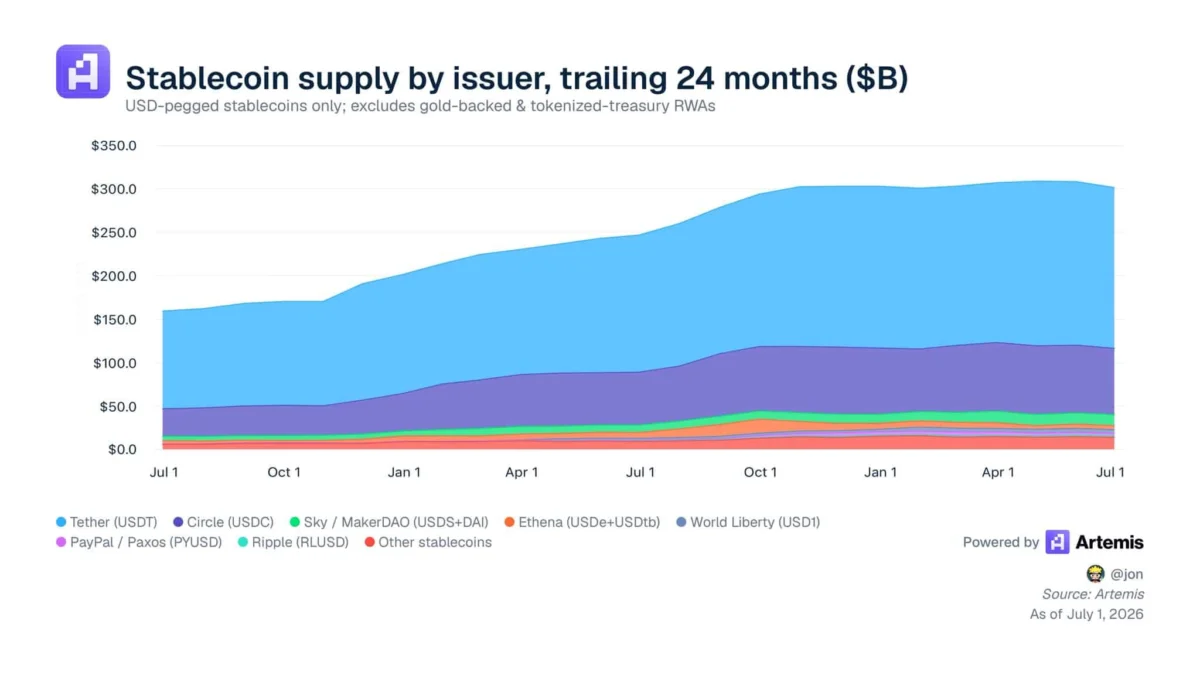

Supporting Data: The Explosion of the Stablecoin Market

The timing of this partnership is far from coincidental. Stablecoins have evolved from speculative tokens into essential components of the global financial plumbing. According to data provided by Artemis, the total supply of USD-pegged stablecoins has experienced a staggering trajectory over the last two years.

In July 2024, the total market capitalization of stablecoins stood at approximately $160 billion. By July 2026, that figure had nearly doubled to $300 billion. This rapid growth suggests that the demand for programmable, high-speed, 24/7 dollar-denominated liquidity is no longer a niche requirement but a macroeconomic necessity.

While Tether (USDT) continues to hold the largest share of the market, USDC has maintained its position as the preferred choice for institutional and regulated entities due to its transparent reserve reporting and robust compliance framework. Despite new competitors entering the market, USDC supply has remained remarkably resilient, holding steady in the $70 billion to $80 billion range. This stability in the face of increased competition underscores the "network effect" that Circle has successfully built—a factor that made it the most attractive partner for a tier-one institution like Standard Chartered.

Official Responses and Strategic Vision

The leadership teams at both Standard Chartered and Circle have framed this partnership as an essential step toward the "modernization of the global financial system."

In a press release detailing the launch, Standard Chartered highlighted that the integration goes beyond simple transaction processing. By embedding USDC access into its institutional offering, the bank is unifying its banking, custody, and digital asset service layers. This "all-in-one" approach is designed to mitigate the risks associated with third-party providers, giving corporate clients the security of a G-SIB-regulated environment while enjoying the speed and efficiency of a blockchain-based asset.

For Circle, this partnership is a realization of its long-term strategy to become the "internet’s financial layer." By partnering with a bank of Standard Chartered’s stature, Circle effectively validates the utility of USDC as a legitimate, institutional-grade payment instrument. The partnership is expected to eventually evolve to support complex payment-related use cases, including real-time cross-border settlements and automated treasury management.

Strategic Implications: Why This Changes Everything

The implications of this partnership are profound, touching on several key areas of the global financial landscape:

1. The Death of Settlement Friction

Currently, international wire transfers can take days to clear, especially across different time zones and banking systems. By utilizing USDC as a settlement rail, Standard Chartered can provide its clients with near-instantaneous settlement capabilities. This is a game-changer for multinational corporations that manage global payroll, supply chain payments, and inter-company liquidity.

2. Trust and Compliance

One of the primary deterrents for corporate adoption of stablecoins has been the fear of regulatory blowback and counterparty risk. By routing USDC transactions through a G-SIB, the regulatory oversight is baked into the process. The bank acts as the gatekeeper, ensuring that all minting and redemption activities adhere to the highest standards of anti-money laundering (AML) and know-your-customer (KYC) requirements.

3. Institutionalizing DeFi

While the initial phase of the partnership focuses on minting and redemption, the long-term potential is the integration of stablecoins into broader financial services. If a bank can hold, move, and provide access to USDC, it can theoretically offer products that interface with the burgeoning world of institutional DeFi, such as automated lending, liquidity provisioning, or tokenized trade finance.

4. A Template for Future Banking

Standard Chartered is effectively setting a template for how traditional banks can survive in a decentralized future. Rather than fighting the tide of blockchain technology, the bank is absorbing it. We can expect other major financial institutions to follow suit, likely seeking their own partnerships with issuers like Circle or developing proprietary stablecoin rails to compete.

Conclusion: The Path Ahead

The partnership between Standard Chartered and Circle is more than just a press release; it is a signal that the "digital dollar" is entering the boardroom. As the supply of stablecoins continues to climb toward the $300 billion mark and beyond, the role of commercial banks in bridging the gap between legacy fiat and blockchain-based assets will become the defining feature of the next decade of finance.

For now, the focus will remain on the rollout in Dubai—a pilot that will serve as the stress test for this new model of institutional engagement. If successful, the integration of USDC into the core of Standard Chartered’s global operations will likely be viewed in hindsight as the moment when the traditional banking sector finally embraced the inevitability of the digital asset era.

As we look toward the remainder of 2026 and into 2027, the question is no longer whether institutional stablecoin adoption will occur, but how quickly the legacy financial system can adapt to keep pace with the efficiency of the blockchain. Through this alliance, Standard Chartered has made it clear that they intend to lead that transition, rather than be disrupted by it.