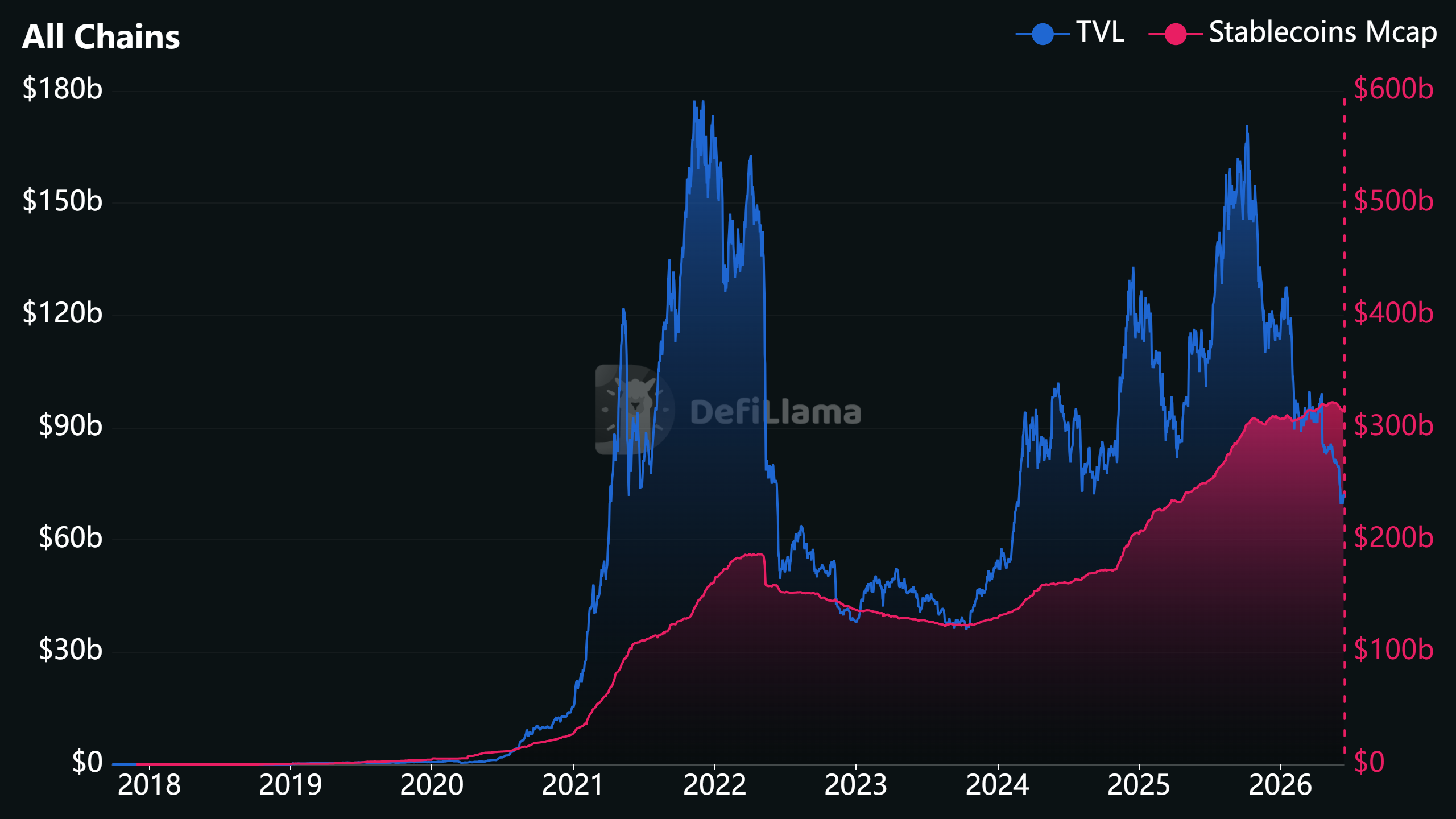

The decentralized finance (DeFi) sector, once the high-growth engine of the cryptocurrency industry, is currently undergoing a period of profound recalibration. Following a sustained decline from its late-2025 peak, the ecosystem’s Total Value Locked (TVL) has plummeted from a staggering $178 billion to approximately $72.5 billion. This contraction is not merely a localized correction; it is a structural shift in how liquidity is deployed across the blockchain landscape.

As capital retreats from lending platforms, liquid staking protocols, and cross-chain bridges, market observers are left to reconcile a puzzling paradox: while DeFi protocol participation is evaporating, the aggregate supply of stablecoins remains stubbornly high at roughly $315 billion. This divergence suggests that the current downturn is not a result of a liquidity crunch or a fundamental collapse in infrastructure, but rather a deliberate, risk-averse pivot by market participants.

Main Facts: The Anatomy of the Decline

The current state of the DeFi ecosystem is defined by three primary variables: a shrinking TVL, stagnant stablecoin reserves, and a compressed yield environment.

- TVL Erosion: The drop from $178 billion to $72.5 billion represents a significant withdrawal of capital. Unlike previous market cycles where specific sectors—such as algorithmic stablecoins or specific L1 ecosystems—bore the brunt of the losses, the current decline is broad-based. Lending, decentralized exchanges (DEXs), and bridge protocols are all seeing consistent outflows.

- The Liquidity Gap: The fact that $315 billion in stablecoin capital sits on the sidelines—or in centralized exchanges—while DeFi TVL falls indicates that capital is not leaving the crypto ecosystem entirely. Instead, it is being held in "dry powder" format, waiting for more favorable risk-adjusted returns.

- Broad Ecosystem Weakness: Participation is shrinking across the board. The lack of sector-specific resilience suggests that the "DeFi-native" user base is collectively de-risking, prioritizing capital preservation over the pursuit of speculative yields.

Chronology: A Quarter of Cascading Challenges

The path to the current $72.5 billion valuation has been marked by a series of compounding pressures that began in the latter half of 2025.

- Late 2025 – The Peak: Driven by bullish sentiment and aggressive yield farming incentives, TVL reached its zenith. At this stage, capital was flowing freely into experimental protocols and complex recursive leverage strategies.

- Q1 2026 – The Yield Compression: As macroeconomic conditions tightened and inflationary pressures forced a reassessment of interest rates, the yield environment for DeFi protocols began to sour. Borrowing demand on major lending platforms plateaued, causing supply-side interest rates to collapse from double-digit highs to the current 3.5%–9% range.

- Q2 2026 – The Security Crisis: The decline accelerated sharply during the second quarter of 2026. The industry faced a wave of exploits that saw nearly 70 protocols compromised, resulting in approximately $746 million in losses. While individual hacks were often smaller than the historic "mega-hacks" of the past, the sheer frequency of these events shattered the illusion of "code is law" for many institutional and retail participants.

- Present Day: The market is now in a state of consolidation. Investors are no longer chasing the "next big protocol" but are instead retreating to the safety of core network assets like Ethereum and Solana, effectively stripping away the layers of DeFi complexity that characterized the previous cycle.

Supporting Data: The Risk-Reward Mismatch

The core of the issue lies in the diminishing incentive structure. In a healthy market, investors demand a "risk premium"—extra yield to compensate for the dangers of smart contract bugs, liquidation risk, and bridge failures.

Currently, that premium has evaporated. With stablecoin lending rates struggling to break the 9% ceiling on major platforms, the effort and risk required to manage a DeFi portfolio often outweigh the returns. When an investor can earn a comparable or slightly lower yield in a safer, traditional-finance-adjacent stablecoin environment—or simply hold the underlying asset—the incentive to provide liquidity to a risky smart contract diminishes.

Furthermore, the persistent $315 billion in stablecoin supply acts as a barometer for market sentiment. If the crypto market were truly in a "death spiral," we would expect to see massive redemptions of stablecoins into fiat currency. The stability of this figure confirms that the capital is present, but it has become increasingly selective and conservative.

Official Responses and Expert Consensus

Industry analysts at platforms like DeFiLlama have pointed to this trend as a "maturation phase." As one researcher noted, "The era of ‘yield at any cost’ is over."

Many protocol developers have attempted to combat this by introducing loyalty programs, governance token airdrops, and improved security audits. However, the data suggests that these incentives are failing to move the needle. Institutional players, who were expected to be the next wave of DeFi growth, have expressed a preference for "permissioned" or "regulated" DeFi environments, leaving the permissionless, open-source protocols to contend with a shrinking retail audience.

The prevailing view among venture capital firms in the space is that the current infrastructure is not broken, but the "product-market fit" for many protocols has shifted. Developers are now under immense pressure to prove that their protocols can provide utility beyond simple yield generation, such as facilitating real-world asset (RWA) tokenization or enabling cross-border payments.

Ethereum and Solana: The Anchor of Conviction

Amidst the general exodus from DeFi, there is a striking divergence in how users treat base-layer assets. While protocol-level TVL is down, staking participation on primary networks remains remarkably robust.

- Ethereum: Roughly one-third of the total ETH supply is currently staked. This indicates that long-term holders are not selling their assets; they are merely choosing to secure the network directly rather than layering their capital into secondary DeFi lending markets.

- Solana: Staking participation remains near 68%, signaling an incredibly high level of network confidence.

This data provides a critical insight: investors have not lost faith in the blockchain revolution. They have simply lost faith in the complexity of the DeFi ecosystem. They are choosing the "risk-free rate" of network staking—which provides consistent, protocol-level rewards—over the variable and increasingly dangerous yields offered by dApps.

Implications: The Future of the Ecosystem

The implications of this shift are profound and likely to shape the next several years of crypto development.

1. The Death of Speculative Yield

The unsustainable "high-yield" farming era is effectively over. Future DeFi growth will likely be driven by real economic activity—such as decentralized exchanges handling genuine trading volume or lending protocols supporting legitimate borrowing for enterprise-grade operations—rather than artificially inflated token incentives.

2. A "Flight to Security"

As the memory of the Q2 2026 exploits lingers, security will become the primary competitive advantage. Protocols that can demonstrate formal verification, multi-layer audits, and institutional-grade insurance will likely win the battle for the remaining liquidity. "Move fast and break things" has been replaced by "audit thoroughly and stay solvent."

3. The Institutional Pivot

The current environment is accelerating the transition toward "DeFi 2.0," or what some call "Institutional DeFi." This involves protocols that integrate KYC/AML (Know Your Customer/Anti-Money Laundering) features to appease regulators. While this may alienate the purist "crypto-anarchist" demographic, it is the only path forward for the massive $315 billion in sidelined stablecoin capital to re-enter the DeFi ecosystem.

4. Consolidation of Protocols

We are likely to see a significant "survival of the fittest." Protocols with low activity and poor security records will continue to see their TVL dwindle to zero. Only the most battle-tested, blue-chip protocols (the likes of Aave, Maker, or Uniswap) are likely to retain their dominance as the ecosystem contracts into a leaner, more resilient structure.

Conclusion

The contraction of DeFi’s Total Value Locked from $178 billion to $72.5 billion is not a sign of an impending industry collapse. Rather, it is a necessary, albeit painful, maturation process. By shedding the layers of speculative, high-risk activity that defined the previous bull market, the sector is forcing itself to return to its core value proposition: providing decentralized financial services that are secure, transparent, and—above all—sustainable.

The capital remains, the networks are thriving, and the conviction of long-term investors in the underlying blockchains of Ethereum and Solana remains unshaken. The next chapter of DeFi will not be written by the flashiest yield farm, but by the protocols that can successfully navigate the current climate of risk aversion and emerge as the bedrock of a more disciplined, mature financial system.