In the rapidly evolving landscape of Decentralized Finance (DeFi), "capital efficiency" has long been the industry’s holy grail. The promise of concentrated liquidity—a feature pioneered to allow Liquidity Providers (LPs) to allocate funds within specific, high-traffic price ranges—was meant to revolutionize how Automated Market Makers (AMMs) function. By focusing capital where trading volume is most intense, LPs were expected to maximize their fee generation while traders enjoyed reduced slippage.

However, a sobering new report from Dune Analytics paints a starkly different reality. Far from the optimized ecosystem envisioned by developers, a significant portion of the liquidity currently fueling major decentralized exchanges (DEXs) is effectively dormant, failing to generate value for its providers or support the underlying trading infrastructure.

The State of Idle Capital: A Quantifiable Crisis

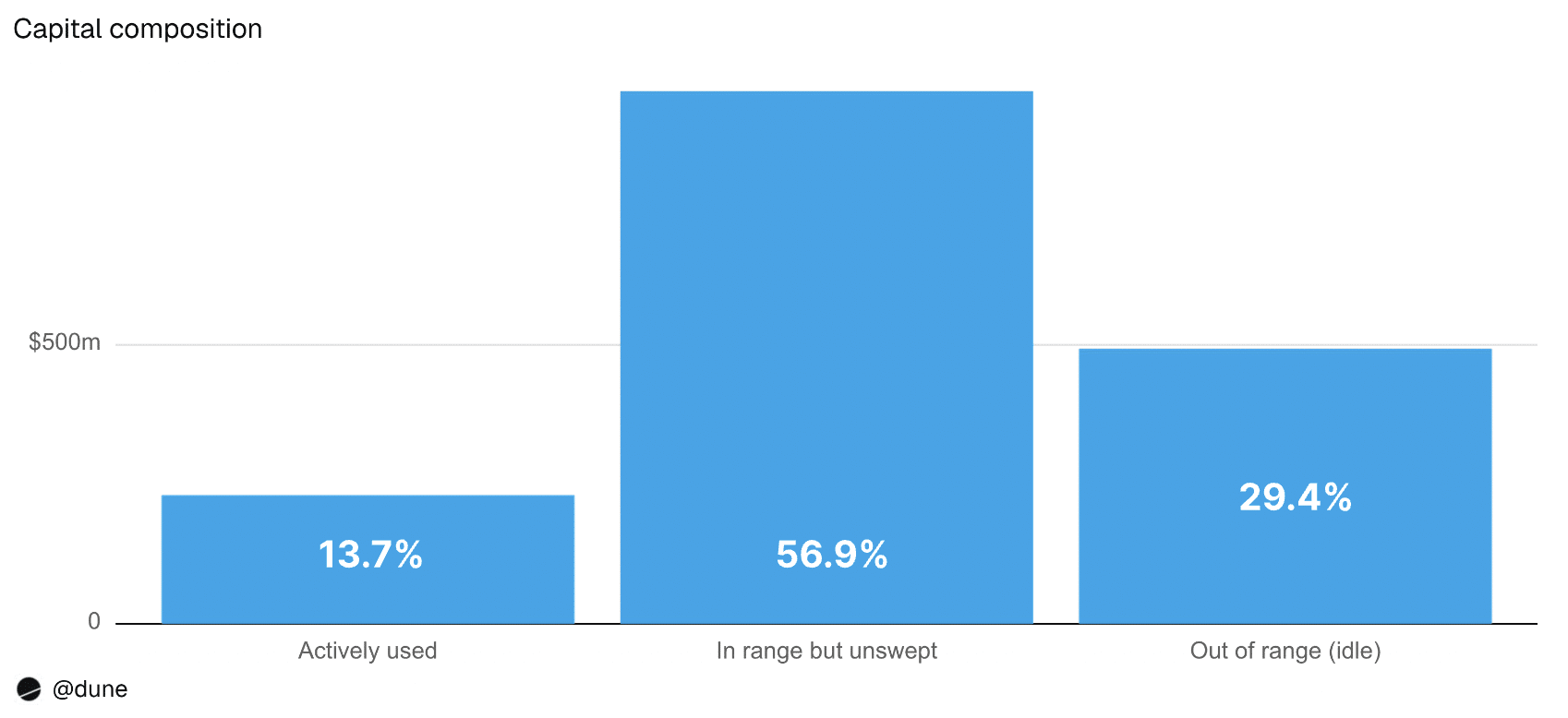

The Dune report, which analyzed data from the first half of 2026, reveals a systemic inefficiency across four major protocols: Uniswap v3, Uniswap v4, PancakeSwap v3, and Aerodrome Slipstream. The findings indicate that, on average, 29.4% of the total liquidity provided to these platforms sits entirely outside the range of active trading.

When liquidity falls outside the active price range, it becomes "idle." It contributes nothing to the depth of the order book and, more importantly, earns zero trading fees for the provider. The financial scale of this stagnation is staggering: approximately $542 million in capital sits idle every single week. On an annual basis, this translates to an estimated $150 million in lost fee revenue for liquidity providers—a massive drain on potential yield in an industry built on the premise of maximizing returns.

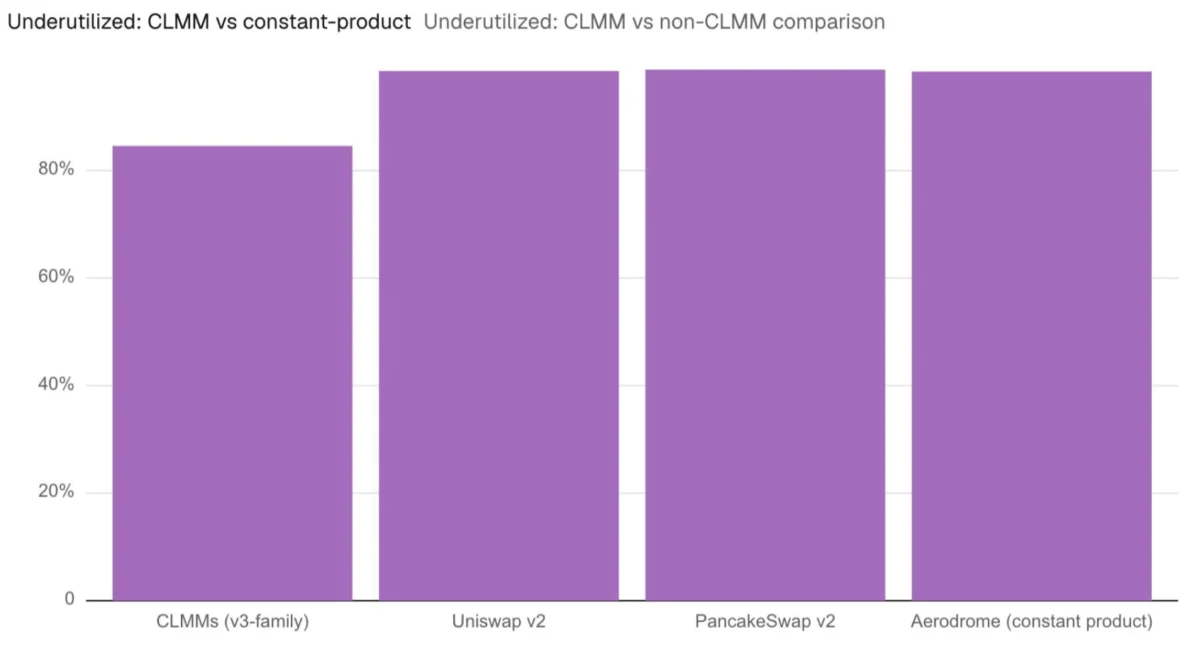

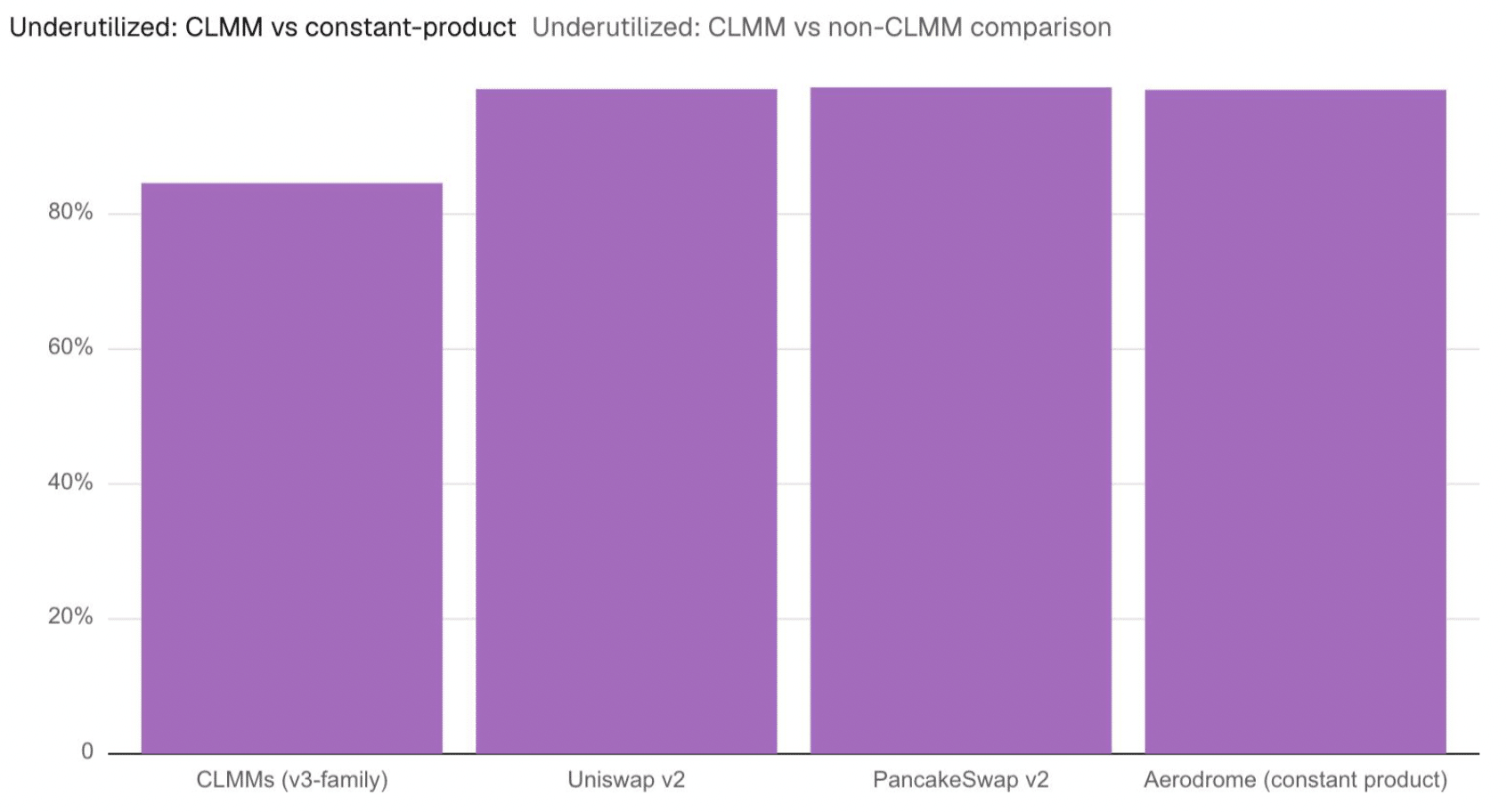

Perhaps most damning is the discovery that when considering liquidity that is technically available but rarely utilized, the rate of underutilization spikes to roughly 85%. This suggests that the problem is not merely a transient issue of market volatility, but a fundamental failure in how capital is being deployed by the average user.

Chronology of a Structural Flaw

The trajectory toward this inefficiency began with the introduction of concentrated liquidity models. While these models theoretically offer higher returns, they demand active, hands-on management. Unlike older "v2" models where capital was spread across the entire price curve from zero to infinity, the "v3" and "v4" architectures require LPs to be active participants in market making.

The 90-Day Warning Sign

The data indicates that over $200 million of idle liquidity has remained in a stagnant state for more than 90 days without being repositioned. This inactivity serves as a smoking gun for a deeper issue: the majority of individual LPs lack the technical infrastructure or the time required to manage their positions effectively. As market prices shift, these positions quickly fall out of range, yet the providers fail to adjust their parameters, essentially "setting and forgetting" their capital in a way that guarantees obsolescence.

The Rise of the Automated Manager

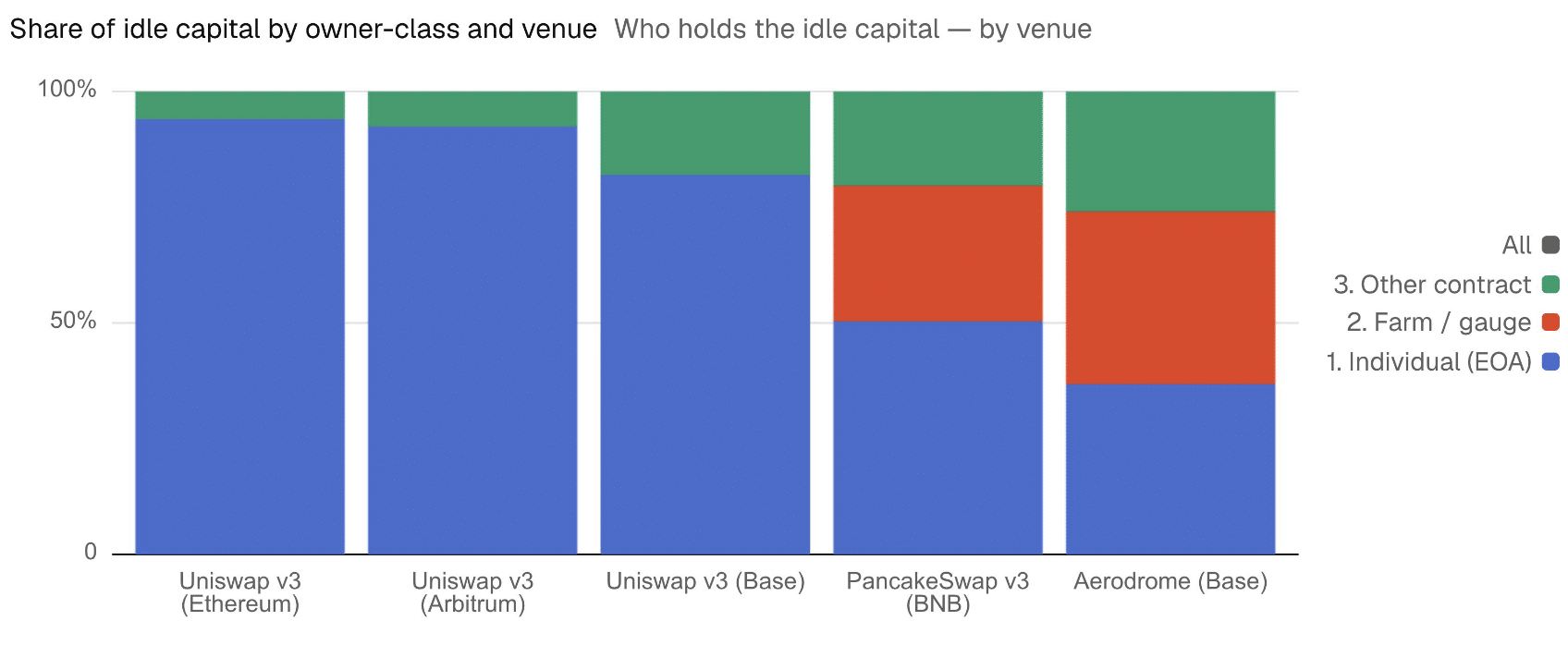

While individual users struggle to keep pace with market fluctuations, a clear divergence has emerged between retail LPs and institutional-grade automated liquidity managers. The study highlights that automated managers—smart contracts and algorithms designed to rebalance positions in real-time—have maintained significantly higher capital activity.

For example, on the Ethereum network, individual wallets held a staggering 94% of idle capital and 91% of Uniswap v3 liquidity. The story is similar on the Arbitrum network, where individuals control 92% of idle liquidity. Even on the Base network, where smart contracts hold roughly 50% of total liquidity, individual users still oversee 82% of the total idle capital.

The contrast is stark: automated managers see only 6.5% of their positions fall out of range, compared to the nearly 30% failure rate among individual retail wallets. This gap highlights a growing "competence divide" in DeFi, where passive retail participants are increasingly at a disadvantage compared to algorithmic competitors.

Supporting Data: The Disparity Across Networks

The report breaks down the distribution of inefficiency across various chains, providing a clear picture of where the capital is most stagnant.

| Metric | Individual Wallet Performance | Automated Manager Performance |

|---|---|---|

| Out-of-Range Rate | ~30% | 6.5% |

| Capital Utilization | Low (High Stagnation) | High (Optimized) |

| Response Time | >90 Days (avg) | Near Real-Time |

This data confirms that the issue is not a flaw in the blockchain architecture itself, but rather in the user-experience layer. The complexity of managing concentrated liquidity is currently beyond the scope of the average retail investor, leading to a massive misallocation of resources that could otherwise be utilized to foster deeper, more liquid markets.

The Uniswap v4 Paradox: Innovation vs. Adoption

One might assume that the transition to Uniswap v4, with its introduction of "hooks"—programmable, customizable features that allow for more complex liquidity management—would solve the idle capital issue. However, the data suggests otherwise.

Even with the advanced capabilities of v4, roughly 30.5% of its liquidity remains out of range. While hooks were designed to allow developers to move idle capital into external yield-bearing strategies (such as lending protocols or automated rebalancing pools), the adoption of these features has been sluggish. Only 10% of v4’s Total Value Locked (TVL) currently utilizes these hooks, and as of the mid-2026 report, none of these active hooks were successfully generating yield from idle capital.

This implies that the "v4 solution" to the idle liquidity problem remains theoretical. Without a significant shift in how liquidity providers interact with these tools, the protocol—despite its technological superiority—continues to suffer from the same fundamental inefficiencies that plagued its predecessor.

Implications for the Future of DeFi

The implications of these findings are profound for the broader DeFi ecosystem.

1. The Death of "Set-and-Forget" Liquidity

The era of passive, concentrated liquidity provision is effectively over. For individual investors, the "concentrated liquidity" model has become a trap. Without the ability to rebalance positions in response to market volatility, retail LPs are losing significant potential income. This creates a barrier to entry that favors professional market makers and institutional-grade algorithmic funds.

2. The Need for "Abstracted" Liquidity

The industry must move toward liquidity abstraction. If individual users cannot manually manage their ranges, the protocols themselves must integrate automatic rebalancing by default. Projects that succeed in building "set-and-forget" products that actually work—perhaps by wrapping individual liquidity into larger, professionally managed vaults—will likely dominate the next cycle of DeFi growth.

3. A Call for Protocol-Level Intervention

The fact that Uniswap v4 hooks are not yet solving the issue suggests that the responsibility may need to shift from the end-user to the protocol developers. We may see a push for "passive concentrated liquidity" models, where protocols automatically move capital based on historical volatility metrics, reducing the burden on the user and ensuring that liquidity is always working.

4. Impact on Market Health

Finally, idle capital is not just a loss for the LP; it is a detriment to the trader. When liquidity is out of range, it does not provide the "depth" required to absorb large trades. This increases slippage for the average user, making the DEX less attractive compared to centralized exchanges or more efficient competitors.

Conclusion: A Turning Point for DEXs

The Dune report is a wake-up call for the decentralized exchange sector. While the industry has made monumental strides in throughput, security, and smart contract innovation, the basic economic efficiency of capital remains a major hurdle.

The transition from the "growth at all costs" phase of DeFi to a "maturity and efficiency" phase requires addressing this half-billion-dollar-a-week leakage. Whether through better user-facing tools, more widespread adoption of automated management, or fundamental changes to how liquidity is programmed at the protocol level, the message is clear: if DeFi is to scale to the masses, it can no longer afford to leave 30% of its capital sitting on the sidelines. The future of decentralized liquidity must be intelligent, automated, and, above all, active.