In a move that signals a tectonic shift in the European digital asset landscape, Revolut—the continent’s largest fintech platform—has officially confirmed it will discontinue support for Tether (USDT). The decision marks a significant turning point for the crypto-finance ecosystem, as institutional platforms grapple with the rigorous requirements of the European Union’s Markets in Crypto-Assets (MiCA) regulation.

Starting August 31, 2026, USDT will be fully delisted from the Revolut platform. For users, the transition is immediate: deposits for the stablecoin are being disabled by the end of July, and any remaining balances held after the August deadline will be automatically liquidated and converted into fiat currency. This move, while unexpected by some, highlights the growing friction between decentralized stablecoin issuers and the increasingly stringent European regulatory environment.

The Chronology of Compliance: From Expansion to Exit

The relationship between Revolut and Tether has been characterized by a recent, short-lived period of optimism. Not long ago, the fintech giant had doubled down on its commitment to crypto accessibility, introducing zero-fee transfers and seamless 1:1 swaps between Tether (USDT) and Circle’s USD Coin (USDC).

However, the regulatory winds shifted rapidly as the MiCA framework began its full implementation phase. Analysts have pointed to a clear timeline of "compliance-driven reversal."

- Pre-2026: Revolut fosters an inclusive environment, integrating various stablecoins to cater to a global user base.

- Early 2026: MiCA regulations move from theoretical frameworks to active enforcement. Compliance teams across European fintechs begin auditing stablecoin reserves against EU standards.

- July 2026: Revolut announces the cessation of USDT deposits, signaling the beginning of the end for the asset on their platform.

- August 31, 2026: The final cutoff date. All remaining USDT positions are slated for mandatory conversion to fiat, effectively removing the asset from the platform’s ecosystem.

Market analyst Max Karpis noted that this is a classic case of "compliance hits again." According to Karpis, the delisting is primarily a risk-mitigation strategy. By removing an asset that does not—or cannot—fully adhere to the specific, restrictive provisions of MiCA, Revolut is shielding itself from potential regulatory penalties that could jeopardize its broader banking operations.

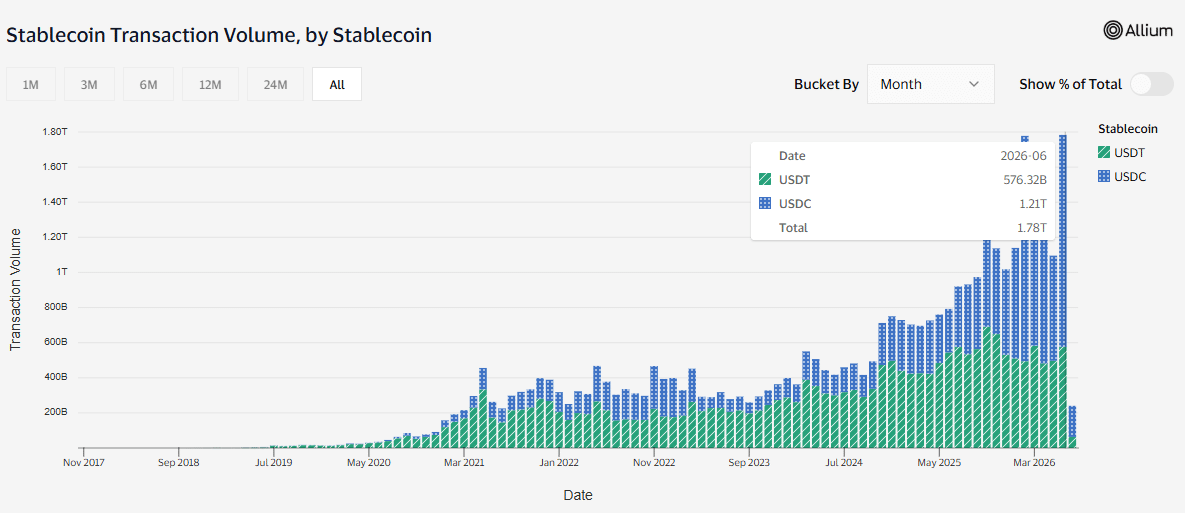

Supporting Data: The Rising Dominance of USDC

While the headlines are dominated by the departure of USDT, the underlying data suggests a broader market migration. As European platforms align with MiCA, Circle’s USDC has emerged as the clear institutional beneficiary.

According to recent data from Visa, the transfer volume for USDC in June reached a staggering $1.21 trillion, effectively doubling that of USDT. This figure represents the second-highest monthly volume for the stablecoin, trailing only the record-breaking $1.28 trillion recorded in February.

The trend is even more pronounced when examining the early days of July, where USDC’s transaction volume surged to three times that of USDT. This delta underscores a decisive shift: as platforms across the EU restrict or delist non-compliant stablecoins, users—particularly those involved in cross-border settlement and institutional trading—are migrating to assets that operate within the "regulatory perimeter" of the EU.

Furthermore, industry reports from TRM Labs reveal that while USD-based stablecoin volumes have faced pressure, Euro-denominated stablecoins have seen an 11x increase in activity. This suggests that the regulatory pressure isn’t just favoring one dollar-pegged coin over another; it is actively steering the European market toward native, compliant, Euro-denominated assets.

The Tether Perspective: A Clash of Ideologies

The decision to delist USDT has placed Tether CEO Paolo Ardoino at the center of a geopolitical and financial debate. Ardoino has been vocal in his opposition to the MiCA framework, characterizing it as not only "bad" but "dangerous" for the future of the stablecoin market.

The Reserve Dilemma

At the heart of Ardoino’s criticism is the MiCA requirement that 60% of stablecoin reserves be held in uninsured cash deposits within European banks. Ardoino argues that this creates a systemic vulnerability. "The problem I have with MiCA is that it is very dangerous for stablecoins," Ardoino stated. "What will happen next year is that a few banks in Europe will go belly up because of these requirements."

Ardoino points out a fundamental disconnect: major European banking institutions, such as UBS, are often unwilling to accept the "crypto-heavy" business model of stablecoin issuers. This leaves issuers to rely on smaller, potentially less resilient banks to hold their reserves. He warns that if a sudden, large-scale redemption event occurs—where users pull more than 20% of their holdings—it could trigger a liquidity crisis for these smaller banking partners, potentially destabilizing the broader financial system.

Sovereignty and the Digital Euro

Beyond the technical risks, Ardoino views MiCA as a strategic tool for the European Central Bank. He believes the regulation is designed to stifle private stablecoin innovation in favor of the upcoming Digital Euro, effectively allowing the state to maintain a tighter grip on capital flows.

In response, Tether has chosen to prioritize the emerging markets where USDT serves as a vital financial lifeline. For many in the Global South, where local currencies are often volatile, USDT is not merely an asset; it is a primary medium of exchange. By refusing to compromise its reserve structure to meet European standards, Tether is effectively opting out of the EU market to preserve its operational independence elsewhere.

Implications for the Future of Crypto in Europe

The removal of USDT from a platform as ubiquitous as Revolut serves as a bellwether for the European crypto industry. Several key implications emerge from this development:

1. The Fragmentation of Liquidity

As platforms bifurcate between "MiCA-compliant" and "Global" assets, liquidity may become fragmented. European users may find it harder to access the deep liquidity pools that USDT provides, potentially leading to higher slippage and increased costs for crypto-to-crypto trading.

2. The Institutionalization of USDC

Circle’s proactive approach to regulatory compliance has paid dividends. By securing the necessary licenses and aligning with MiCA, USDC has cemented its status as the "institutional stablecoin" of choice for the European region. The data from Visa confirms that institutional capital is risk-averse; when faced with regulatory uncertainty, it gravitates toward the path of least resistance.

3. The Shift to Euro-Denominated Assets

The 11x growth in Euro-denominated stablecoins is perhaps the most significant long-term indicator. If the EU succeeds in making the regulatory environment too hostile for USD-pegged coins, the market will naturally pivot to Euro-pegged alternatives. This would fulfill one of the implicit goals of MiCA: the promotion of European financial sovereignty in the digital age.

4. Risk for Non-Compliant Platforms

Platforms that continue to offer non-compliant assets risk the "Revolut treatment." As regulators tighten the screws, compliance will cease to be a competitive advantage and become a bare-minimum requirement for operation. Exchanges and fintechs will likely continue to audit their offerings, potentially triggering a "delisting cascade" for any asset that cannot provide transparent, bank-held reserves that meet the 60% threshold.

Conclusion: A New Era for Stablecoins

The delisting of USDT by Revolut is more than a mere administrative update; it is a reflection of a global financial system in transition. Tether’s defiance of MiCA, coupled with the regulatory embrace of USDC and other compliant stablecoins, illustrates two very different visions for the future of money.

On one side stands the decentralized, permissionless philosophy represented by Tether—a vision that prioritizes utility and global access, even at the cost of being shut out of major regulated markets. On the other side is the MiCA-compliant framework, which seeks to integrate crypto assets into the traditional banking fold, ensuring consumer protection and state oversight.

As of the end of August 2026, the European retail user will have significantly fewer ways to interact with the world’s most popular stablecoin. Whether this leads to a more stable, secure environment or merely drives activity to less regulated, riskier offshore platforms remains to be seen. What is certain, however, is that the era of "stablecoin Wild West" in Europe has effectively come to a close. Users must now prepare for a new, highly regulated landscape where compliance—not just adoption—defines the winners and losers of the digital asset revolution.