The cryptocurrency market is currently defined by a profound paradox. While recent weeks have seen a dramatic surge in price action—sparked by institutional optimism surrounding Bitcoin spot ETF filings—a deeper examination of liquidity, regulatory pressures, and macroeconomic headwinds suggests that this rally may be built on a fragile foundation.

Main Facts: The Institutional Catalyst

The primary driver of the current market optimism is a sudden, high-profile interest from traditional finance (TradFi) giants. BlackRock, the world’s largest asset manager, ignited a firestorm of speculation in June by filing for a Bitcoin spot ETF. This move was swiftly mirrored by Fidelity, another titan of the investment world.

These filings represent more than just corporate interest; they signal a potential pivot toward the long-awaited legitimization of Bitcoin as a standard asset class for retail and institutional investors alike. Further bolstering this sentiment was the launch of EDX Markets, a new digital asset exchange backed by a consortium of heavyweight firms, including Charles Schwab, Citadel Securities, and Fidelity.

However, the market’s reaction—a 20% surge in Bitcoin and a 16% jump in Ether over a three-week window—has been met with skepticism by seasoned analysts. The central question remains: Is the promise of an ETF, which faces an arduous path through the Securities and Exchange Commission (SEC), worth such a significant premium?

Chronology of the Recent Rally

- Early June 2023: The market begins to stir as institutional interest gains momentum, despite an increasingly aggressive regulatory climate.

- Mid-June 2023: BlackRock and Fidelity officially file for spot Bitcoin ETFs, causing an immediate decoupling of crypto prices from broader, more cautious market indicators.

- June 2023 (Regulatory Onslaught): The SEC files formal lawsuits against Coinbase and Binance, alleging massive securities violations. Despite the gravity of these charges, crypto prices remain surprisingly resilient.

- Late June 2023: Reports surface that the SEC deems the initial ETF filings "inadequate," requesting more detail on surveillance-sharing agreements.

- July 2023: Market participants observe that while Bitcoin and Ether hold their gains, liquidity across centralized exchanges remains at its lowest point since 2020.

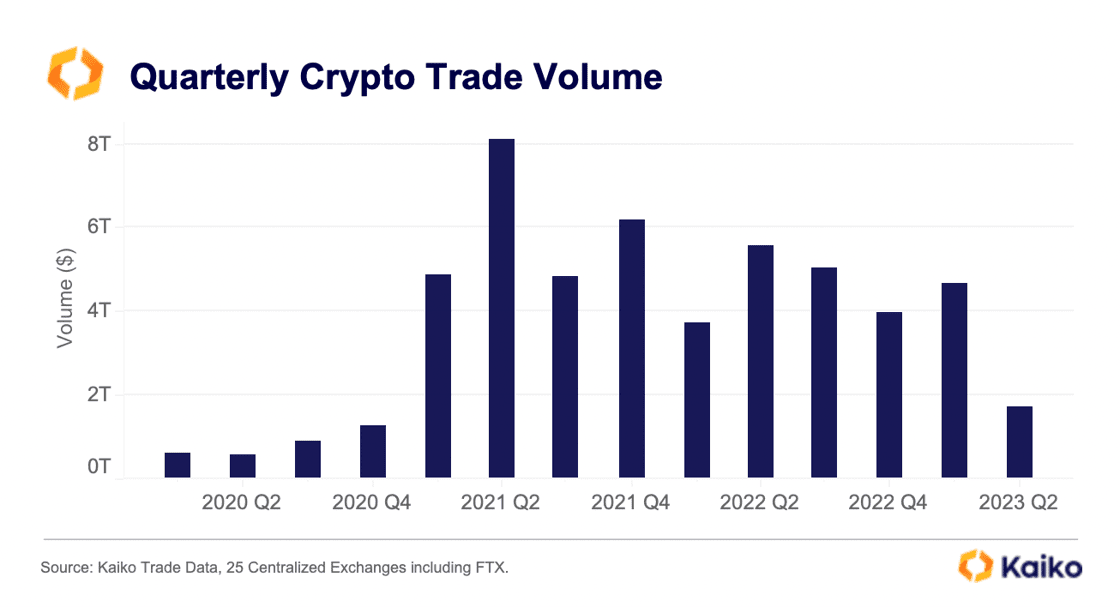

Supporting Data: The Liquidity Drought

The most alarming aspect of the current market cycle is the state of liquidity. Data from Kaiko indicates that trading volumes on centralized exchanges have plummeted, reaching lows not seen since before the 2020 bull run. When liquidity is thin, price volatility is inevitably amplified; smaller buy or sell orders can trigger disproportionately large price swings.

This lack of market depth is compounded by a massive exodus of stablecoins from exchanges. Over the last six months, exchange-held stablecoin balances have dropped by approximately 60%, representing a $26 billion outflow. This suggests that the "dry powder" typically used to fuel aggressive buying is simply not present in the same capacity as it was during the height of the pandemic-era rally.

Conversely, derivatives markets have shown a degree of resilience, with volume significantly higher than in the second half of 2022. This divergence suggests that professional traders are still hedging and positioning themselves, even if the "spot" market—where actual assets change hands—remains stagnant and wary.

Regulatory Implications: The SEC’s Dual Front War

The regulatory environment has shifted from a nuisance to a central structural threat. The SEC’s legal action against Binance is largely viewed as a crackdown on a global entity that has long operated in legal grey zones. However, the lawsuit against Coinbase is fundamentally different.

By targeting Coinbase—a publicly traded company in the United States that has spent years attempting to work within the SEC’s established framework—the regulator has sent a clear message: the existing classification of "crypto assets as securities" is not up for negotiation. The irony of the situation is palpable; the SEC presided over Coinbase’s IPO in 2021, effectively validating its business model, only to label its core operations as illegal two years later.

For investors, the implication is stark. While Bitcoin seems to have carved out a unique position in the eyes of regulators, the rest of the altcoin market is effectively in limbo. When the SEC labels tokens as securities, it forces exchanges to delist them, draining liquidity and forcing retail investors into corners of the market that are increasingly difficult to access.

Macroeconomic Headwinds: The Fed’s Shadow

While the crypto market has been focused on ETF filings, the macroeconomic reality remains grim. The Federal Reserve’s "pause" in interest rate hikes has been widely misinterpreted by some as a signal of a pivot. In reality, Fed Chair Jerome Powell has been explicit: the pause is a strategic breather, not a cessation of policy tightening.

Fed futures indicate an 86% probability of a 25-basis-point hike in the coming weeks. The market is pricing in a "higher-for-longer" interest rate environment, which traditionally acts as a gravity well for risk assets like Bitcoin. The surge in crypto prices over the last month has occurred despite these rising interest rate expectations, creating a dangerous divergence between crypto sentiment and the broader economic reality.

The "Crypto to Crypto" Phenomenon: Is it Sustainable?

The common refrain in the industry is that "crypto is going to crypto," implying that the market operates on its own internal logic, often disconnected from fundamental analysis or macroeconomic trends. While this has been true in the past, the current market structure is different.

The reliance on a potential ETF approval as a singular catalyst for growth is a high-risk gamble. As noted in the SEC’s feedback, the "surveillance-sharing agreements" required for an ETF to function are not a formality—they are a complex hurdle that the industry has failed to clear for years. Fidelity’s own application was rejected in 2022 for similar reasons.

If the market is betting on the inevitability of the ETF, it may be right in the long term, but disastrously wrong in the short term. The capital outflow from exchanges, the drying up of liquidity, and the ongoing legal battles suggest that the current price rally is an anomaly, not the start of a sustained bull market.

Final Analysis: Navigating the Murky Waters

Investors should view the current "greed" in the market with extreme caution. The Fear and Greed Index currently sits at 61, indicating a sentiment shift that lacks a solid foundation in liquidity or macroeconomic stability.

Monetary policy operates with a significant lag. We are currently navigating the effects of one of the most aggressive interest rate hiking cycles in modern history. The full impact of these rates—moving from zero to above 5% in such a short window—has yet to be fully felt in the real economy.

When you combine this with the regulatory crackdown that threatens to reshape the landscape of digital asset trading, the outlook becomes significantly more complex. The current surge might be fueled by institutional headlines, but the "under the hood" metrics suggest a market that is thin, reactive, and vulnerable to external shocks. As the industry moves into the second half of 2023, the gap between the perceived excitement and the reality of the balance sheets is a gap that every participant must navigate with care.

For those looking to the future, the focus should not just be on whether the ETF is approved, but on whether the underlying liquidity of the market can actually support the next wave of institutional adoption. Until those foundations are shored up, the current "greed" remains a dangerous guide.