The Indian cryptocurrency landscape is currently gripped by a peculiar and concerning phenomenon: a massive, sustained premium on Tether (USDT). While stablecoins are designed to maintain parity with the U.S. Dollar, the price of USDT on Indian exchanges has surged to levels over 8.5% higher than the official USD/INR exchange rate. This is not a mere market glitch; it is a manifestation of a profound structural imbalance driven by regulatory tightening, a scarcity of capital inflows, and a desperate struggle to maintain access to dollar-pegged liquidity.

Main Facts: The Anatomy of a Price Disconnect

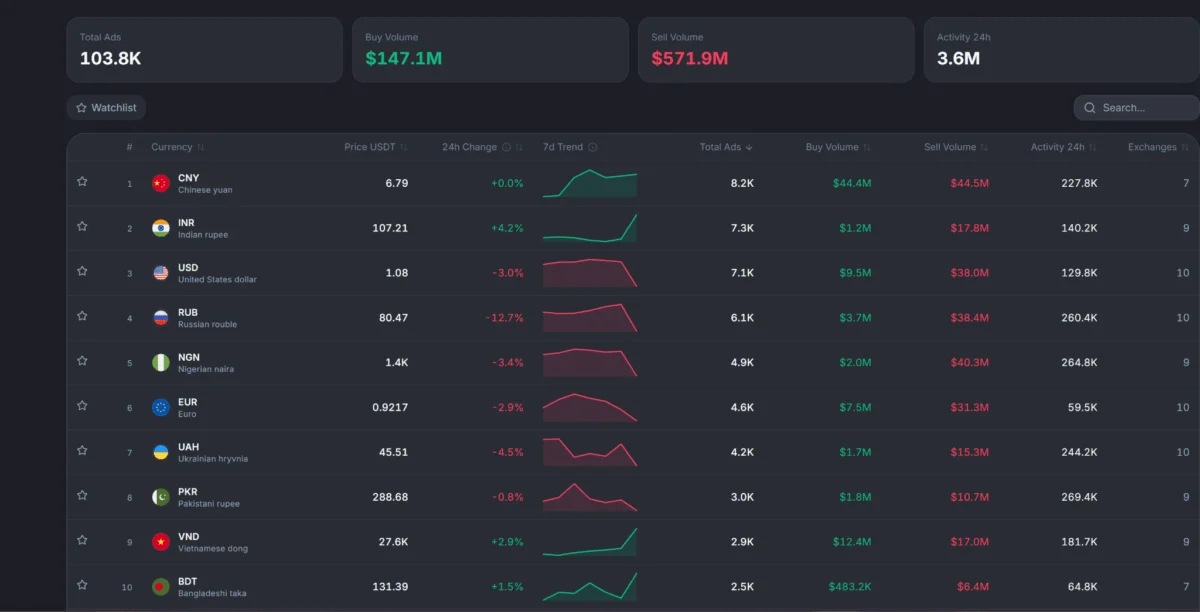

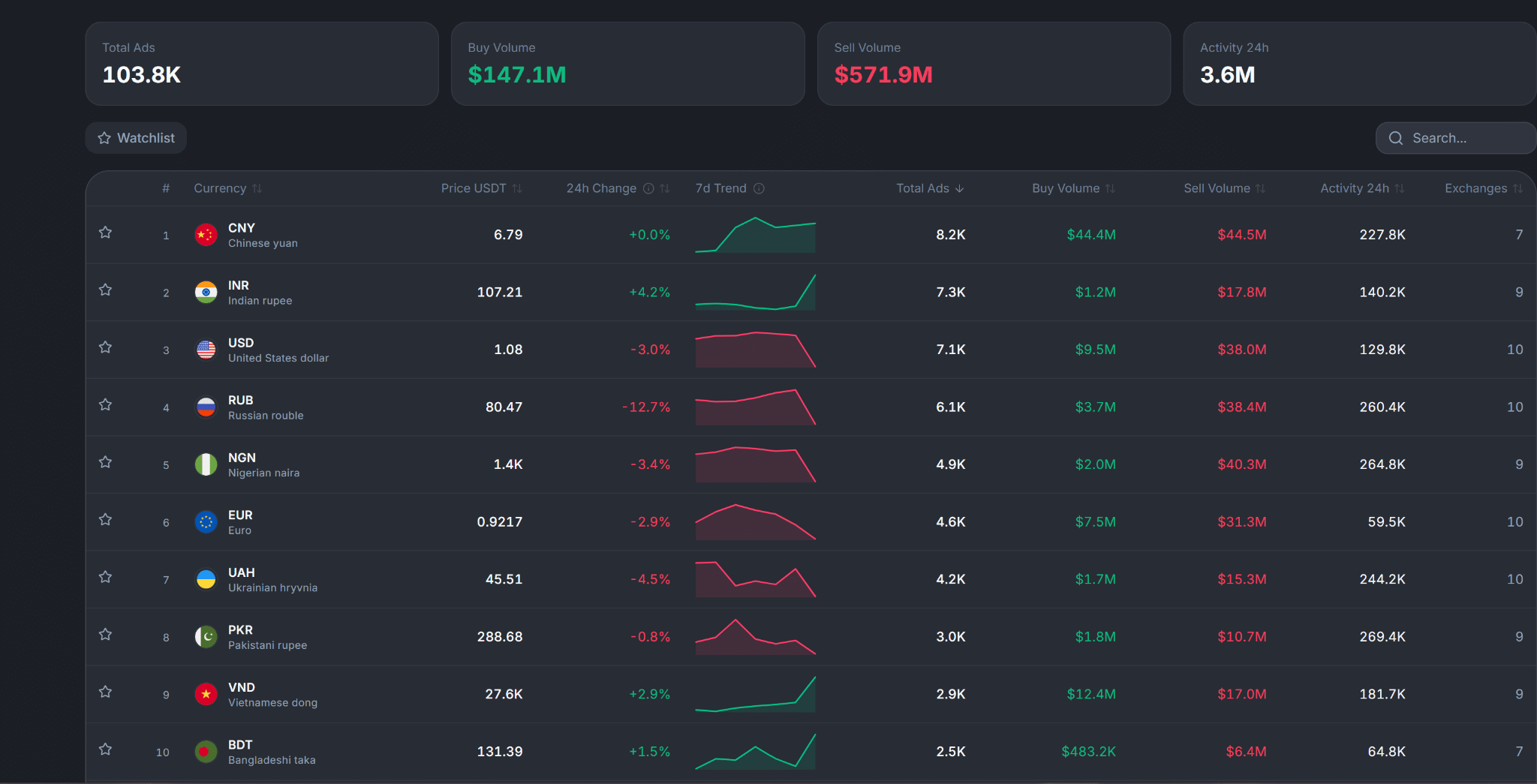

At the heart of the current crisis is the widening chasm between the official forex rate and the street price of USDT. As of the latest market assessments, USDT is trading at approximately ₹102.88, significantly higher than the official USD/INR reference rate of ₹94.65.

Typically, the premium for USDT in India hovers within a 3–4% range, a spread largely attributed to the friction involved in moving capital into the crypto ecosystem. However, the current climb to over 8.5% signals that the market is struggling to function efficiently. This surge is directly correlated with a contraction in the domestic supply of stablecoins. Regulatory bodies in India have increased their oversight of Virtual Digital Asset (VDA) platforms, leading to enforcement actions that have effectively throttled the "on-ramps" that typically allow for the smooth entry of liquidity into the Indian crypto market.

Chronology: From Stablecoin Utility to Regulatory Bottleneck

To understand how the market reached this point, one must look at the evolution of the Indian regulatory environment over the last 18 months:

- The Growth Phase: Following the post-pandemic digital asset boom, India emerged as one of the world’s most active hubs for P2P (Peer-to-Peer) crypto trading. Businesses and individuals increasingly relied on USDT for cross-border settlements and as a hedge against rupee volatility.

- The Regulatory Shift: Faced with concerns over money laundering and capital flight, Indian financial authorities and tax agencies intensified scrutiny. The implementation of stringent Tax Deducted at Source (TDS) on VDA transactions and the freezing of bank accounts associated with suspicious P2P activity set the stage for a liquidity drought.

- The Enforcement Surge: Recent months have seen high-profile investigations into VDA transfers, including scrutiny over an estimated ₹2,500 crores in transactions. These actions served as a deterrent for market makers and institutional liquidity providers who were previously the primary conduits for USDT inflows.

- The Current Standoff: As of June 2026, the cumulative effect of these actions has led to a stagnant supply side. With fewer new USDT entering the Indian market, the remaining tokens are being bid up by a base of users whose demand for dollar-pegged assets remains inelastic, regardless of the price.

Supporting Data: Liquidity Under Siege

Data from P2P marketplaces and on-chain analysis paints a grim picture of market health. Despite the high price, the actual volume of successful trades is telling a story of scarcity.

Recent P2P transaction data reveals an INR/USDT rate of roughly ₹107.21 during peak volatility. While the daily transaction count remains high—frequently exceeding 140,000 transactions—the total dollar value moving through these channels is remarkably thin.

The disparity in order books is perhaps the most damning metric. Recent snapshots show buy volume at a mere $1.2 million, contrasted against a massive $17.8 million in sell volume. This reflects a total breakdown in market-making capacity. Under normal circumstances, arbitragers would step in to sell USDT in the Indian market to capture the premium, thereby increasing supply and pushing the price down. However, the current regulatory climate makes it too risky for professional market makers to bridge the gap. Consequently, the "buy" side is left to compete for a dwindling pool of existing stablecoins, while the "sell" side is inhibited by the fear of regulatory freezes on their INR bank accounts.

Official Responses and the Regulatory Stance

While the Reserve Bank of India (RBI) and the Financial Intelligence Unit (FIU) have not commented on the specific USDT premium, their broader stance on Virtual Digital Assets remains cautious and restrictive.

The official narrative centers on "Financial Stability" and "Anti-Money Laundering" (AML) compliance. Regulators have consistently warned that the decentralized nature of P2P platforms makes them conduits for illegal capital outflows. By enforcing strict KYC and AML protocols, authorities have successfully slowed down the rapid movement of capital.

However, industry participants argue that this approach is akin to using a sledgehammer to crack a nut. The "enforcement-first" strategy has inadvertently penalized legitimate businesses—such as small-to-medium enterprises that use stablecoins for international trade settlements—who now find themselves unable to access foreign exchange at reasonable rates. There is a growing call from industry associations for a more nuanced framework that separates illicit activity from legitimate liquidity provisioning, which would allow for a more stable and regulated flow of capital.

Implications: The Long-Term Cost of Inefficiency

The current situation carries significant implications for the future of India’s digital economy:

1. The Rise of Informal Channels

If the premium remains elevated for an extended period, market participants will inevitably pivot away from regulated exchanges toward "shadow" or informal trading channels. This undermines the very regulatory objectives the government is trying to achieve, as it pushes activity further into the dark where it cannot be monitored or taxed.

2. Erosion of Market Competitiveness

For Indian businesses, the 8.5% premium acts as an "invisible tax" on international operations. If it becomes significantly more expensive to hold or transfer value in USDT compared to international counterparts, Indian startups and cross-border service providers will find themselves at a competitive disadvantage.

3. The "Brain Drain" of Capital

When capital markets become inefficient, capital finds a way to leave. If the domestic market cannot provide a safe, stable, and cost-effective way to store value, high-net-worth individuals and corporate entities will increasingly seek to offshore their dollar liquidity. This could result in a permanent reduction in the depth and vitality of the Indian crypto sector.

4. The Path to Restoration

The solution to the current impasse is two-fold: regulatory clarity and market access. If authorities were to provide a clear, compliant pathway for licensed entities to act as liquidity providers, the premium would likely evaporate as arbitrage opportunities returned.

Without such intervention, the market is poised to remain in a state of high-cost inefficiency. The resilience of active wallet addresses suggests that the demand for USDT in India is not going away; it is simply being forced to pay an increasingly high price for the privilege of access.

Final Summary: The Need for Equilibrium

The ongoing spike in India’s USDT premium is a symptom of a larger struggle between digital innovation and traditional financial regulation. The data is clear: when supply is constrained by fear and regulatory ambiguity, price discovery breaks down, and the cost of capital skyrockets.

For the Indian crypto market to regain its efficiency, the current "wait and see" approach from both regulators and the private sector must transition into a more collaborative framework. Whether this is achieved through clearer definitions of VDA trading, the integration of compliant banking gateways, or a more surgical approach to enforcement, the outcome remains the same: a return to a 3-4% premium range would signify a healthy, functioning market. Until then, the 8.5% premium remains a high-cost reminder that the regulatory landscape is currently the most significant barrier to the maturation of India’s digital asset ecosystem.