The global financial landscape is currently undergoing a silent but seismic transformation as stablecoins cement their position as the bedrock of the digital asset ecosystem. With a total market capitalization reaching a staggering $315.62 billion at the time of writing, stablecoins have moved beyond mere speculative tools to become the primary medium of exchange in the burgeoning world of tokenized finance. However, beneath the surface of this massive aggregate valuation, a dramatic divergence is occurring. While legacy giants Tether (USDT) and Circle (USDC) continue to solidify their dominance, institutional experiments like PayPal’s PYUSD are facing significant headwinds, signaling a challenging environment for newcomers attempting to disrupt the established duopoly.

Main Facts: The Pillars of Digital Liquidity

The stablecoin sector currently functions as the primary bridge between traditional fiat currencies and decentralized finance (DeFi). Tether remains the undisputed titan of the industry, commanding a dominant 59% market share. Its closest competitor, Circle’s USDC, holds a 24% share, effectively creating a two-horse race that controls over 80% of the entire stablecoin market.

The primary function of these assets—maintaining a 1:1 peg with the U.S. dollar—has provided a safe haven for investors during periods of high volatility in the broader crypto markets. As institutions have begun to integrate blockchain technology into their core treasury operations, the demand for high-liquidity, regulated stablecoins has reached an all-time high. Yet, the recent contraction of PayPal’s PYUSD serves as a stark reminder that brand recognition and institutional backing alone are insufficient to displace entrenched market leaders in the highly competitive liquidity landscape.

Chronology: The Rise and Retrenchment of PYUSD

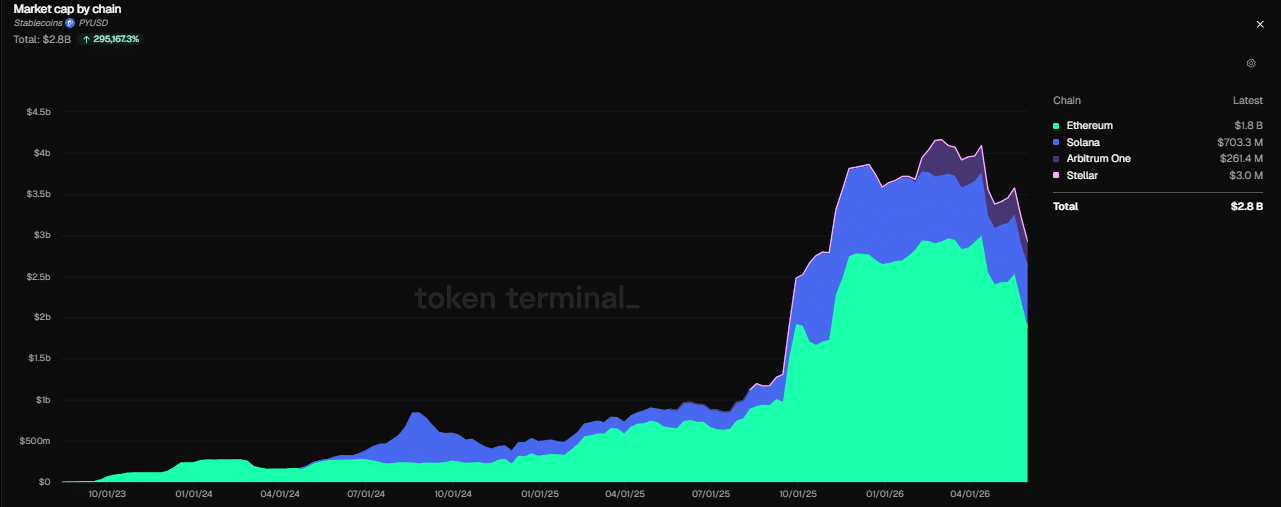

The journey of PayPal’s PYUSD provides a compelling case study in the difficulties of stablecoin adoption. After its high-profile launch, the project saw an meteoric rise, peaking in March with an all-time high market capitalization of $4.20 billion. This period of rapid expansion was fueled by expectations that PayPal’s massive global user base would seamlessly transition into on-chain finance.

However, the subsequent months have painted a much grimmer picture. PYUSD has experienced a sharp contraction, with its market cap collapsing by approximately 35%. Currently, the asset trades at a valuation of $2.47 billion. A breakdown of its distribution reveals its struggle to gain widespread traction across major chains:

- Ethereum (ETH): The majority of the supply, totaling $1.80 billion, remains anchored to the Ethereum network.

- Solana (SOL): Despite the network’s high transaction speed and low fees, PYUSD has only managed to secure $703 million in market cap.

- Arbitrum One (ARB): The layer-2 solution currently holds $261 million.

- Stellar Lumens (XLM): Minimal adoption persists, with a market cap of just $3 million.

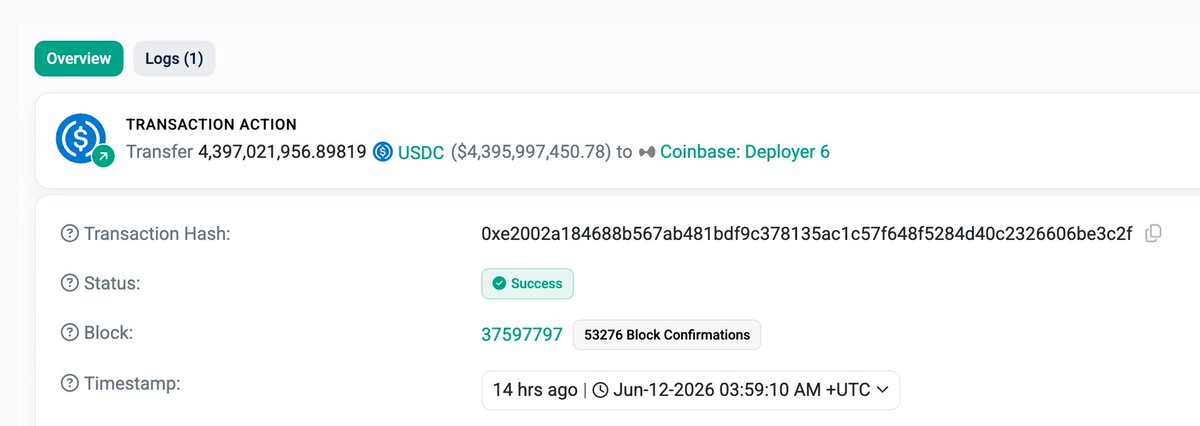

This cooling period for PYUSD stands in direct contrast to the aggressive maneuvers by Circle, which recently executed its largest historical transfer—moving $4.40 billion in USDC to the Coinbase Hyperliquid deployer. This move was not merely a logistical shift; it was a strategic consolidation of liquidity that reinforces Coinbase’s status as a central hub for USDC-denominated trading activity.

Supporting Data: The Dominance of the Incumbents

The divergence in performance becomes even more pronounced when analyzing on-chain transaction data. Tether and Circle continue to outperform all competitors in terms of both volume and network utility.

Weekly Asset Transfer Metrics

In the most recent weekly analysis, USDC recorded an asset transfer count of $133.6 million, trailing slightly behind USDT’s $176.9 million. When broadening the scope to look at the cumulative transfer counts of major issuers, USDT led with 176 million transactions compared to the aggregate 392 million across the broader stablecoin ecosystem, proving that the vast majority of stablecoin "work" is being performed by the top two assets.

Monthly Growth Trends

The momentum for the incumbents remains positive. Over the past 30 days:

- USDC: Asset transfer counts surged by 27%, reaching $466 million.

- USDT: Despite its already massive base, USDT saw a growth of 2.1%, with transfer volumes reaching approximately $1.40 trillion.

- User Adoption: Holder growth for USDT increased by over 5%, while USDC followed closely with a 4.7% increase in unique wallet addresses.

These statistics suggest that while the "hype" around new stablecoin projects may fluctuate, the underlying utility and network effects of USDT and USDC create a powerful "moat" that is increasingly difficult for newer entrants to cross.

Official Perspectives and Market Implications

The stablecoin market is no longer confined to the U.S. Dollar. Industry leaders are now looking toward a multi-currency future, with the issuance of Euro-denominated and Yen-denominated stablecoins gaining momentum.

Rob Hadick, a partner at the venture capital firm Dragonfly, has recently highlighted the transformative potential of this sector. Hadick predicts a potential 10x growth for the industry as payment adoption expands beyond speculative trading into real-world commercial settlements. His thesis rests on the idea that stablecoins act as "infrastructure-killers." By bypassing the legacy SWIFT and correspondent banking systems, stablecoins reduce dependency on high-cost intermediaries, allowing for near-instant, low-cost global value transfer.

While entities like Tempo have seen their supply surge by 35% in a single week—reaching $30 million—these smaller projects serve as a reminder that the niche for specialized, regional, or specific-use-case stablecoins still exists. However, they remain a drop in the ocean compared to the massive liquidity pools provided by USDT and USDC.

Future Outlook: Consolidation or Fragmentation?

The current market data suggests that we are moving toward a period of intense consolidation. The collapse of PYUSD’s market cap indicates that the market is "voting with its liquidity." Users and institutions alike prefer stablecoins that offer:

- High Liquidity Depth: The ability to move billions of dollars without significant slippage, as demonstrated by Circle’s recent $4.40 billion transfer.

- Network Ubiquity: The presence of the asset across multiple high-performance chains (Solana, Ethereum, Arbitrum).

- Regulatory and Financial Confidence: The established track record of USDT and USDC in maintaining their pegs despite global economic shocks.

As payment infrastructure continues to evolve, the "10x growth" predicted by experts like Hadick will likely be captured primarily by the incumbents who already possess the necessary regulatory frameworks and liquidity depth. For challengers, the barrier to entry is no longer just technology; it is the sheer scale of the network effect enjoyed by Tether and Circle.

The coming year will be decisive. Will we see a resurgence in institutional stablecoins, or will the market continue to funnel capital into the two established giants? The data from the last quarter provides a clear answer: in the high-stakes world of digital finance, liquidity is king, and the incumbents show no signs of yielding their crowns.

Summary of Key Findings

- Market Concentration: USDT and USDC dominate with over 80% of the total stablecoin market share.

- Institutional Struggles: PayPal’s PYUSD has shed 35% of its market cap since its March peak, highlighting the difficulty of gaining traction against incumbents.

- Liquidity Shifts: Circle’s record-breaking $4.40 billion transfer to Coinbase underscores the centralization of liquidity around established stablecoin providers.

- Growth Potential: Industry experts project a 10x growth for the sector as stablecoins evolve from speculative tools into primary infrastructure for global commercial payments.

- Operational Utility: On-chain data confirms that USDT and USDC are the primary engines of the crypto economy, with record-breaking transfer counts and consistent holder growth.