The digital asset landscape is currently witnessing a profound transformation, anchored by the massive expansion of the stablecoin sector. As of the latest market data, stablecoins remain the bedrock of the tokenization movement, boasting a combined market capitalization of $315.62 billion. This sector has evolved from a niche utility for crypto traders into a critical infrastructure layer for global finance. While Tether’s USDT continues its reign as the undisputed market leader with a 59% dominance, Circle’s USDC maintains a firm second place at 24%. However, recent market dynamics reveal a stark divergence in the trajectories of these established giants compared to newcomer institutional offerings like PayPal’s PYUSD.

Main Facts: The Current State of the Stablecoin Economy

Stablecoins serve as the bridge between traditional fiat currencies and the decentralized blockchain ecosystem. Their utility in providing liquidity, enabling cross-border payments, and serving as a safe haven during periods of market volatility has solidified their position as the most successful application of blockchain technology to date.

The current market hierarchy is clear: Tether (USDT) is the titan of the industry, commanding the lion’s share of liquidity and daily volume. USDC, known for its transparency and regulatory compliance, continues to attract institutional capital. Meanwhile, the entry of traditional financial institutions—most notably PayPal with its PYUSD stablecoin—initially signaled a potential shift in how retail and institutional users interact with digital dollars. Yet, as the market matures, the "first-mover advantage" of USDT and the "compliance-first" strategy of USDC appear to be creating a moat that is difficult for newer entrants to cross.

Chronology: The Rise and Retrenchment of PYUSD

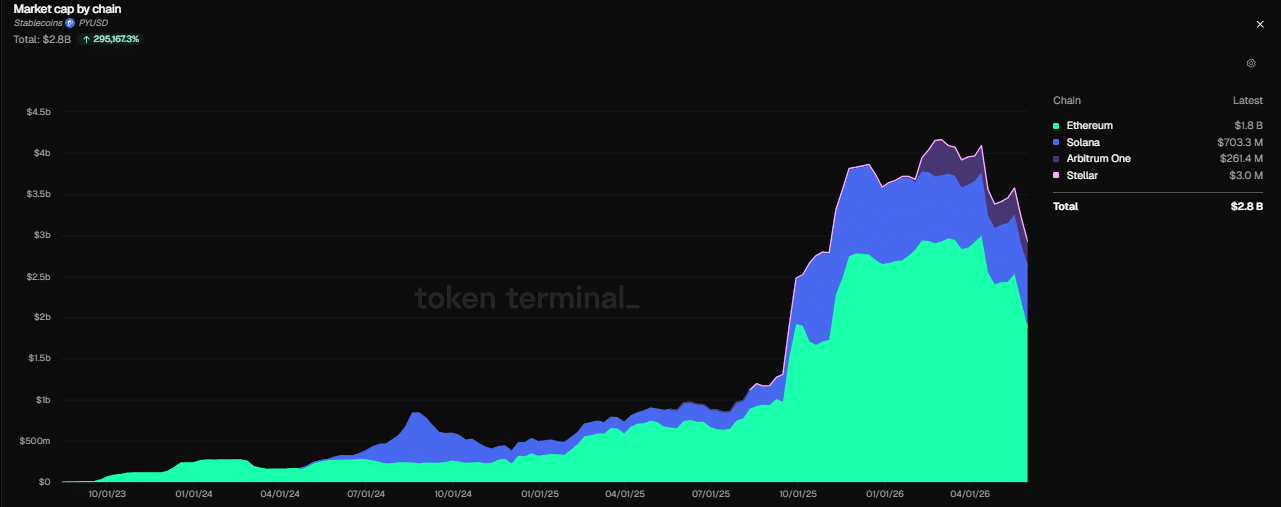

The journey of PayPal’s PYUSD serves as a compelling case study for the volatility inherent in the stablecoin sector. Following its launch, the asset saw rapid adoption, fueled by the vast user base of the PayPal ecosystem. By March, PYUSD reached a historic milestone, hitting an all-time high market capitalization of $4.20 billion.

However, the momentum proved fleeting. In the months following that peak, PYUSD entered a period of significant contraction, shedding approximately 35% of its market value. Currently, the asset’s market cap has consolidated to roughly $2.47 billion. A breakdown of its distribution reveals its reliance on the Ethereum (ETH) network, which hosts $1.80 billion of its supply. Meanwhile, its presence on other major chains—Solana (SOL), Arbitrum One (ARB), and Stellar Lumens (XLM)—stands at $703 million, $261 million, and $3 million, respectively.

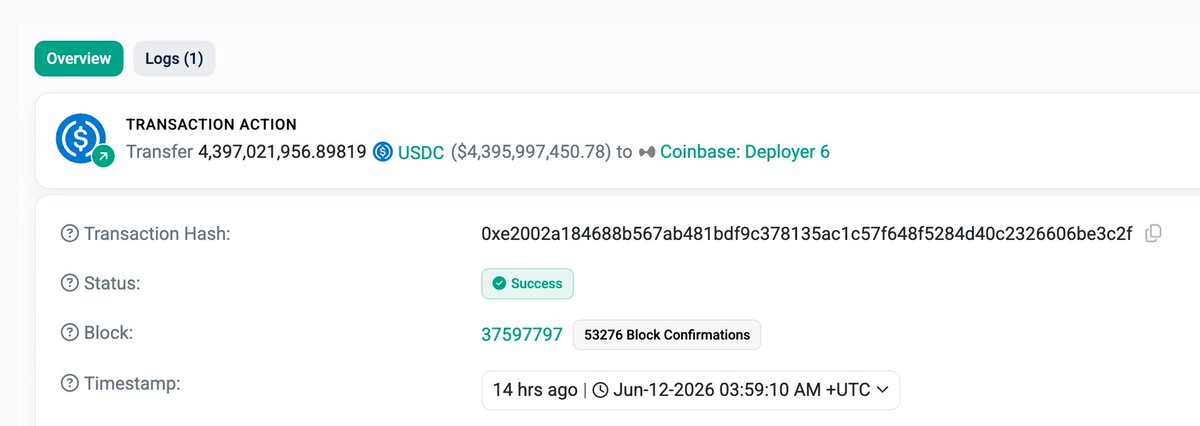

This contraction occurs against a backdrop of aggressive expansion by Circle. While PYUSD was retreating, Circle executed the largest single transfer in its history, moving $4.40 billion in USDC to the Coinbase Hyperliquid deployer. This move, combined with a fresh minting of $750 million in USDC on the Solana blockchain within a 24-hour window, has pushed Circle’s total market cap to $74.78 billion, underscoring the company’s commitment to maintaining its position as the primary competitor to Tether.

Supporting Data: Transactional Velocity and Network Growth

To understand the health of the stablecoin market, one must look beyond total market capitalization and examine on-chain activity and user growth. The transactional data for the past week highlights a consistent preference for the two industry incumbents.

USDC recorded an asset transfer count of $133.6 million, while Tether’s USDT surpassed this with $176.9 million. When viewing these figures through the lens of weekly asset transfer volume, the discrepancy becomes even more pronounced: USDT processed 176 million transfers compared to 392 million across the broader stablecoin issuer landscape, cementing the dominance of the top-tier assets.

Furthermore, the growth trends in user acquisition are telling. Over the past month, the USDC asset transfer count surged by 27%, reaching $466 million, while USDT’s growth remained steady at 2.1%, albeit on a much larger base of approximately $1.40 trillion. Perhaps most significantly, the user base for both assets is expanding, with USDT holders increasing by over 5% and USDC holders growing by 4.7%. These figures demonstrate that despite market fluctuations, the adoption of stablecoins is not merely a product of institutional movement but is increasingly driven by a growing retail and professional user base.

Official Responses and Industry Sentiment

While individual companies like Circle and Tether focus on liquidity and distribution, industry analysts are looking at the macro implications of this growth. The shift in stablecoin dynamics has not gone unnoticed by venture capital firms and financial strategists.

Rob Hadick of Dragonfly recently provided a bullish outlook on the sector, projecting a potential 10x growth for stablecoins as payment adoption broadens. Hadick argues that the current financial infrastructure, which relies on legacy banking systems, is ripe for disruption. By collapsing the complexity of these systems and reducing the need for intermediaries, stablecoins offer a path toward more efficient, borderless capital movement.

This sentiment is echoed by the emergence of niche players like Tempo. Although its current supply of $30 million is modest, the 35% surge in its stablecoin supply within a single week serves as a microcosm of the potential for specialized payment infrastructure. It suggests that while the "big two" (USDT and USDC) dominate the general-purpose market, there is an opening for specialized, regional, or use-case-specific stablecoins to thrive.

Implications: The Future of Global Finance

The trajectory of the stablecoin market holds profound implications for the future of global finance. Several key themes emerge from the current data:

1. The Institutional "Moat"

The contraction of PYUSD highlights that brand recognition alone is not enough to displace incumbents in the crypto space. Liquidity depth and multi-chain availability are the true determinants of success. For institutional players entering the space, the challenge lies in matching the technical agility and widespread acceptance that Tether and Circle have built over years of operation.

2. Multi-Currency Expansion

The stablecoin market is no longer a "USD-only" game. As the sector matures, we are seeing the rise of Euro-denominated and Yen-denominated stablecoins. This diversification is essential for stablecoins to fulfill their promise as a global currency replacement rather than a temporary digital proxy for the U.S. dollar. This expansion will likely lead to a more complex regulatory environment, forcing issuers to navigate a global patchwork of financial laws.

3. The Death of Intermediaries

As Rob Hadick noted, the ultimate goal of the stablecoin revolution is the reduction of reliance on traditional banking intermediaries. Every time a major liquidity movement occurs—such as Circle’s $4.40 billion transfer—it demonstrates that massive value can be settled on-chain without the friction of the SWIFT network or correspondent banking delays. As this efficiency becomes the standard, traditional banks will be forced to either integrate with this new architecture or risk obsolescence.

4. Regulatory Scrutiny

With a combined market cap exceeding $300 billion, stablecoins have officially become a systemic factor in the global economy. Regulators in the U.S., EU, and Asia are closely monitoring these flows. Future growth will be contingent on the ability of issuers to maintain transparency regarding their reserves and adhere to increasingly strict KYC/AML (Know Your Customer/Anti-Money Laundering) requirements.

Final Summary: A Market in Transition

The stablecoin sector is currently defined by a tension between consolidation and diversification. On one hand, the dominance of Tether and Circle continues to grow, as evidenced by their massive transactional volumes and increasing user bases. On the other hand, the struggle of newer entrants like PayPal’s PYUSD reveals that the "stablecoin war" is won through deep-rooted network effects and liquidity, rather than just market entry.

As the market approaches a potential 10x expansion, the focus will likely shift from simple market cap growth to utility. We are entering an era where stablecoins will be judged not by how much capital they hold, but by how effectively they facilitate the movement of value across the global economy. Whether it is through the growth of non-USD stablecoins or the rise of specialized payment infrastructures like Tempo, the future of money is increasingly being written in code. For investors and observers alike, the lesson of the current cycle is clear: in the digital economy, liquidity is the ultimate currency, and the race to capture that liquidity is far from over.