In a landmark shift for traditional corporate finance, South Korean automotive giant Hyundai has announced a major expansion into the world of stablecoins. By leveraging blockchain technology for internal capital transfers between its international subsidiaries, Hyundai is moving beyond experimental pilot programs and toward a future where digital assets replace legacy interbank systems. This transition marks a significant milestone in enterprise adoption, signaling that the global financial architecture may be on the cusp of a decentralized evolution.

Main Facts: The Shift from SWIFT to Blockchain

For decades, the global movement of capital between international business units has been tethered to the traditional banking system. These legacy methods—often relying on the SWIFT network and a web of correspondent banks—are notoriously sluggish, frequently requiring four hours or more, and often taking several business days to finalize.

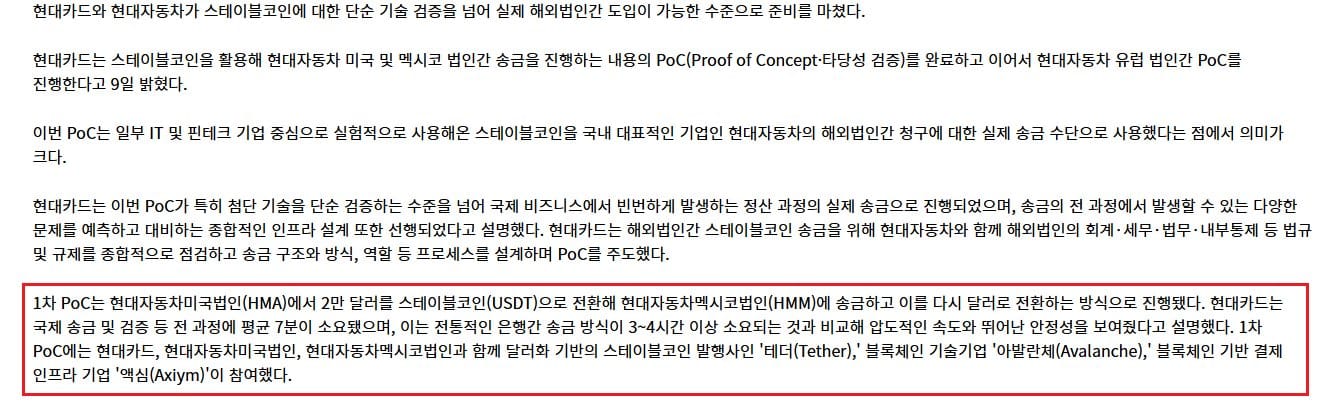

Hyundai’s recent pilot program, conducted in collaboration with its credit card arm, Hyundai Card, has shattered these historical benchmarks. By utilizing Tether’s USDT on the Avalanche blockchain, the automaker successfully transferred funds between its U.S. and Mexico offices in approximately seven minutes.

The pilot was a collaborative effort involving a high-profile consortium:

- Hyundai Motor Group: The parent entity providing the logistical infrastructure.

- Hyundai Card: The financial services arm spearheading the integration.

- Avalanche: The high-speed, scalable blockchain network serving as the settlement layer.

- Tether: The provider of the USDT stablecoin.

- Axiym: The payment integration firm bridging the gap between traditional enterprise resource planning (ERP) systems and blockchain protocols.

By bypassing the traditional banking layer, Hyundai has demonstrated that stablecoins offer "overwhelming speed and superior stability" compared to conventional wire transfers, effectively eliminating the friction that has long plagued multinational treasury operations.

Chronology of Innovation: A Multi-Phase Rollout

Hyundai’s foray into digital assets is not an isolated experiment but part of a structured, multi-phase strategy aimed at modernizing its global treasury.

Phase 1: The North American Pilot

The initial test, conducted in the first half of 2026, focused exclusively on the US-Mexico corridor. The objective was to validate whether stablecoin transfers could meet the stringent regulatory and internal compliance standards required for a major automotive manufacturer. The success of this pilot, achieving a 7-minute settlement time, confirmed the viability of the architecture.

Phase 2: European Expansion and Diversification

Following the success of the USDT trial, Hyundai has set its sights on the European market. By the end of July 2026, the automaker will initiate a secondary pilot program involving Circle’s USDC in partnership with global payments leader Visa. This phase is critical; by testing a different stablecoin (USDC) and a different payment partner (Visa), Hyundai is ensuring that its infrastructure is "chain-agnostic" and capable of supporting multiple digital assets.

Phase 3: Future-Proofing Global Infrastructure

Looking toward the fourth quarter of 2026 and beyond, Hyundai has stated its intent to explore broader use cases. This includes the integration of stablecoins into international remittance services and the development of a proprietary payment infrastructure that could eventually serve not just internal subsidiaries, but potentially external suppliers and partners within the automotive supply chain.

Supporting Data: The Competitive Landscape of Stablecoins

The choice of stablecoins is not merely a technical decision; it is a strategic maneuver within a rapidly maturing market. As stablecoins transition from niche crypto assets to essential tools for liquidity, the rivalry between the two market leaders—Tether (USDT) and Circle (USDC)—has intensified.

The Rise of USDC

Recent data from the first half of 2026 shows a tectonic shift in market dynamics. For the first time, USDC has overtaken USDT in annual transaction volume.

- Total Annual Transaction Volume: Approximately $9 trillion.

- USDC Share: $6 trillion (63%).

- USDT Share: $3.3 trillion (36%).

This shift is largely attributed to the implementation of the Markets in Crypto-Assets (MiCA) regulation in the European Union. MiCA has provided a clear, institutional-grade framework for stablecoin issuers, and USDC’s regulatory-first approach has made it a preferred choice for entities operating within, or heavily interacting with, the European market.

While USDT remains the dominant force in liquidity and trading, the enterprise world—as evidenced by Hyundai’s upcoming European pilot—is increasingly gravitating toward USDC, citing the importance of regulatory transparency and compliance.

Official Responses and Industry Sentiment

The move by such a major industrial player has drawn significant praise from the crypto-native financial sector.

Paolo Ardoino, CEO of Tether, remarked on the development: "This is a quintessential example of real-world adoption. When companies like Hyundai—a pillar of the global economy—choose USDT to optimize their internal treasury, it validates years of infrastructure development. We are no longer talking about crypto-native use cases; we are talking about the optimization of global commerce."

Bo Hines, CEO of Tether U.S., echoed these sentiments, framing the development as a precursor to the next generation of global finance: "What we are witnessing is the blueprint for the future of finance. It’s about removing the friction of distance and the inefficiency of outdated settlement times. Hyundai is showing the way for the entire automotive and manufacturing sector."

Implications for Global Enterprise

The implications of Hyundai’s initiative are profound and extend far beyond the automotive industry.

1. The Death of the "Weekend Lag"

Traditional cross-border payments are often halted by bank holidays, time-zone differences, and weekend closures. Blockchain-based settlements occur 24/7/365. For a company like Hyundai, which manages complex, just-in-time supply chains, the ability to move capital instantly on a Saturday or a holiday provides a massive competitive advantage in cash management.

2. Regulatory Normalization

By working with established players like Visa and adhering to the frameworks of regions like the EU (MiCA), Hyundai is helping to "de-risk" the use of stablecoins for other Fortune 500 companies. As the legal status of stablecoins becomes clearer, the barrier to entry for other conservative, risk-averse multinational corporations will continue to drop.

3. Disintermediation of Banking

The most disruptive implication is the potential for large corporations to reduce their reliance on traditional correspondent banks. If a corporation can settle payments directly on a public or permissioned blockchain, the need for the costly, slow, and opaque intermediary banking layers diminishes. This could lead to a broader "banking revolution" where corporations act as their own financial hubs.

4. Supply Chain Finance

Hyundai’s explicit mention of "payment infrastructure" suggests that the company is looking at the entire supply chain. Future iterations could involve "smart contracts" where payment is automatically triggered upon the digital verification of a shipment, further automating the procurement process and reducing administrative overhead.

Conclusion: A Paradigm Shift

Hyundai’s transition to stablecoin-based transfers is more than a technical experiment; it is a clear signal that the financial infrastructure of the 20th century is being replaced. By successfully integrating USDT and preparing for USDC, the automaker is positioning itself at the forefront of a global shift toward programmable, high-speed money.

As companies continue to seek ways to mitigate the inefficiencies of the legacy banking system, the success of the Hyundai-Avalanche-Tether-Visa ecosystem will likely serve as a roadmap for the next wave of corporate adoption. The battle between USDT and USDC is not just a competition between two tokens; it is the catalyst that will ultimately define how the next $10 trillion of global trade is moved, settled, and secured.

For the automotive industry, and indeed for the global economy, the message is clear: the future is not just electric—it is digital.