As of July 18, 2027, the U.S. financial landscape finds itself at a critical juncture. The GENIUS Act—the landmark federal framework designed to govern the burgeoning payment stablecoin sector—has reached its first major milestone date. While the legislation was hailed as a "watershed moment" for the digital asset economy upon its passage one year ago, the reality of its implementation has proven to be a complex, multi-layered regulatory marathon.

With the first anniversary of the Act now behind us, the industry is left balancing optimism for long-term growth against the frustration of delayed rulemaking. As regulators scramble to finalize the granular details of compliance, market participants are looking for clarity on how the future of the $300 billion stablecoin industry will be shaped.

The Chronology of Compliance: A Three-Year Roadmap

The GENIUS Act was never intended to be a "flip-the-switch" regulation. Instead, it was architected as a progressive, multi-phase framework designed to allow both the government and private entities time to adjust to the new paradigm of digital asset oversight.

Phase 1: The Initial Rulemaking (Year One)

The first 12 months, concluding on July 18, 2027, were dedicated to the "Finalization Period." During this time, the Federal Reserve, the Office of the Comptroller of the Currency (OCC), and other relevant federal agencies were mandated to finalize the primary rulemaking requirements. These rules cover the essential infrastructure of the Act: reserve transparency, redemption rights, and capital requirements for stablecoin issuers.

Phase 2: The Implementation Phase (18 Months)

By January 2027, the framework was intended to begin its transition into full effect. The expectation was that once regulators published their final rules, issuers would immediately begin aligning their operational workflows to meet these new standards. This phase serves as the bridge between theoretical compliance and practical application, forcing firms to reconcile their existing business models with the new federal expectations.

Phase 3: Total Compliance (Year Three)

The transition period is slated to culminate by mid-2028. Once this date passes, the regulatory grace period will officially expire. From that point forward, any firm offering or handling stablecoins within the United States must be fully compliant with the GENIUS Act. Failure to adhere to these mandates will effectively ban non-compliant firms from participating in the U.S. market, marking the end of the "wild west" era of stablecoin operations.

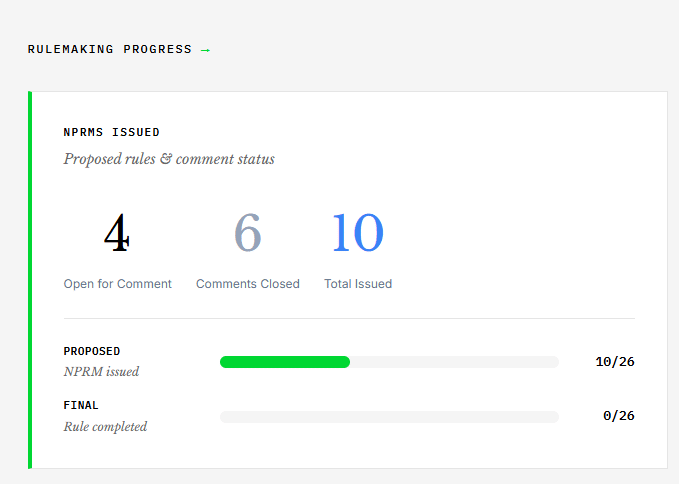

The Regulatory Bottleneck: Why Finalization Is Stalled

Despite the clear timeline, the bureaucracy has encountered significant friction. Six major regulatory bodies have introduced a total of 10 rulemaking proposals. As of mid-July 2027, none of these proposals have reached the finish line of official completion.

The Status of Proposals

While six of the ten proposals have successfully concluded their public comment periods—meaning they are currently in the final review stages and could be signed into law at any moment—four critical proposals remain stuck in the comment phase.

Among these open items are regulations concerning the Bank Secrecy Act (BSA) and specific sanction compliance protocols for FDIC-supervised stablecoin issuers. The complexity of these issues cannot be overstated; regulators are attempting to balance the need for national security and anti-money laundering (AML) controls with the desire to foster innovation in a decentralized ecosystem.

Congressional Pressure and the Fed’s Stance

The pressure to move forward is palpable. Federal Reserve Chairman Kevin Warsh recently addressed the stall in a Congressional hearing, emphasizing the urgency of the task. "We’re racing to put that out (the final rules) by this deadline," Warsh remarked, signaling that the Fed is acutely aware of the market’s impatience. However, the sheer volume of technical feedback from the banking sector has necessitated a more cautious approach than initially anticipated.

Industry Concerns: The Banking Sector’s Perspective

The banking industry, a primary stakeholder in this transition, has been vocal regarding its opposition to certain components of the GENIUS Act. Specifically, the "stablecoin yield loophole"—which allows certain non-bank entities to issue stablecoins while offering features that resemble interest-bearing accounts—has been a major point of contention.

Industry lobbyists have warned of three primary dangers if the final rules are not calibrated correctly:

- Regulatory Arbitrage: The potential for firms to move operations to jurisdictions with looser oversight, thereby undermining the intent of the U.S. framework.

- Uneven Playing Fields: Traditional banks argue that they are subject to stringent capital requirements that stablecoin issuers are currently bypassing, leading to a competitive imbalance.

- Incongruous Requirements: The concern that the final rules may be "unworkable," creating a scenario where compliance is technically possible but commercially ruinous.

Market Resilience: Growth Amidst Uncertainty

Despite the regulatory gridlock, the market’s reaction to the GENIUS Act has been overwhelmingly positive. Since the inception of the law, the total supply of stablecoins in the U.S. has expanded from $250 billion to over $300 billion. This $50 billion increase suggests that institutional and retail investors alike are gaining confidence in the long-term stability of the sector, viewing the GENIUS Act as a "seal of approval" rather than a hurdle.

Institutional Adoption

The most significant indicator of market health is the entry of legacy financial giants. Firms like Fidelity have begun launching stablecoin-related offerings, leveraging the security of the new regulatory framework to attract institutional capital. This shift from "crypto-native" firms to traditional financial behemoths signifies that stablecoins are becoming a core component of the modern financial infrastructure.

User Metrics

Crypto platforms are also reporting increased activity. For instance, the platform Phantom recently recorded a 20% surge in stablecoin balances—climbing from $2.33 billion to $2.82 billion. Such metrics demonstrate that despite the uncertainty surrounding the "final" rules, the demand for stable, blockchain-based liquidity is accelerating.

Implications: The Path Toward Global Leadership

Senator Bill Hagerty, a key architect and co-sponsor of the GENIUS Act, remains bullish on the framework’s potential to define the next decade of finance.

"The United States has the first comprehensive federal framework for payment stablecoins," Hagerty stated. "We are positioning America not just to participate in the digital asset economy, but to lead it. It was a watershed moment, and it’s only the beginning."

The Strategic Value of Clarity

The implications of the GENIUS Act extend far beyond the immediate regulation of tokens. By providing a clear, federally sanctioned path for stablecoin operation, the U.S. is positioning the dollar to remain the dominant currency in the digital age. As more global commerce moves to blockchain rails, the presence of a robust, transparent, and regulated stablecoin ecosystem will be essential for the continued dominance of the U.S. dollar.

The "Wait and See" Strategy

As the industry enters the second year of the GENIUS Act, the focus will shift from legislative debate to operational execution. The coming months will be defined by two key factors:

- The Publication of Final Rules: Once the remaining four proposals are finalized, the "guesswork" for firms will evaporate, likely triggering a new wave of capital allocation and product development.

- Enforcement Trends: As we move toward 2028, the focus will shift to how these rules are enforced. Will the regulators take a punitive approach, or will they act as partners to help firms transition?

Conclusion: A New Era of Digital Finance

The first year of the GENIUS Act has been characterized by high ambitions and a slow, methodical grind toward implementation. While the delay in finalizing key rules has created some friction, the underlying growth of the stablecoin market suggests that the regulatory framework is achieving its primary goal: fostering confidence.

As we look toward the 18-month and 36-month milestones, the U.S. is effectively building the plumbing for the future of finance. The transition will not be without its challenges—banks and crypto firms will continue to clash over the specifics of compliance—but the trajectory is clear. The GENIUS Act has established the ground rules for the digital asset economy, and the race is now on to see which institutions can best adapt to the new, regulated reality of the U.S. stablecoin market. The next year will be the true test of whether the United States can maintain its competitive edge in the global digital asset race.