The digital asset ecosystem is currently witnessing a defining moment in the evolution of tokenized value. As of the latest market readings, the stablecoin sector—the backbone of decentralized finance (DeFi) and cross-border digital payments—has reached a formidable market capitalization of $315.62 billion. This massive pool of liquidity acts as the primary bridge between traditional fiat currencies and the volatile, high-growth world of blockchain technology.

However, beneath the surface of this aggregated figure, a clear hierarchy has emerged. Tether (USDT) continues to cement its position as the undisputed market leader, commanding a 59% market share, while Circle’s USDC holds a firm second place with 24%. Yet, the narrative of late has been defined by a striking divergence: the contraction of PayPal’s PYUSD and the aggressive, large-scale expansion of Circle’s USDC infrastructure.

Main Facts: The Current Landscape of Stablecoin Liquidity

The stablecoin market has moved far beyond its origins as a mere hedging tool for crypto traders. It has transformed into a global settlement layer. The dominance of Tether and Circle is not accidental; it is the result of years of institutional integration, regulatory navigation, and liquidity depth.

Recent market data reveals that while total capitalization continues to grow, the distribution of that growth is uneven. PayPal, which initially entered the space with significant fanfare, aimed to leverage its massive user base to capture market share through its PYUSD offering. Despite a promising trajectory that saw the asset peak at a $4.20 billion market cap in March, the project has faced significant headwinds.

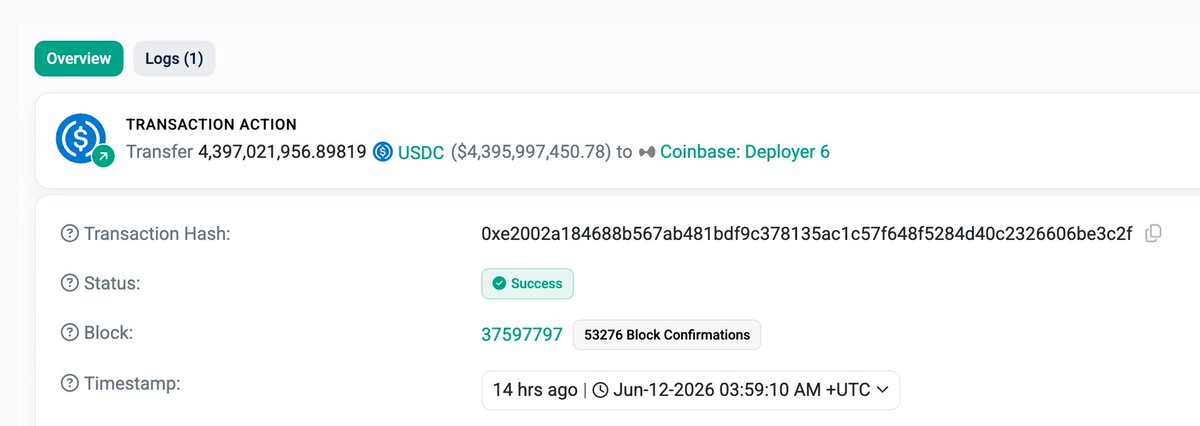

Conversely, Circle has demonstrated its commitment to high-velocity liquidity. In a move that signaled a massive shift in capital, Circle recently executed its largest transfer in history—moving $4.40 billion in USDC to the Coinbase Hyperliquid deployer. This single transaction underscores the changing nature of institutional stablecoin utility, moving away from simple retail holding toward complex, high-frequency decentralized exchange (DEX) liquidity provision.

Chronology: The Rise and Retrenchment of PYUSD

To understand the current state of the market, one must look at the timeline of PYUSD’s recent performance.

- March 2024: PYUSD reaches its all-time high, peaking at a market capitalization of $4.20 billion. At this stage, it appeared that PayPal’s integration into the Ethereum ecosystem would challenge the duopoly of Tether and USDC.

- Q2 2024: The momentum stalls. Following the peak, PYUSD began a period of contraction. Market analysts noted a lack of deep-rooted utility beyond the PayPal app itself, which hindered the token’s ability to circulate within the broader DeFi ecosystem.

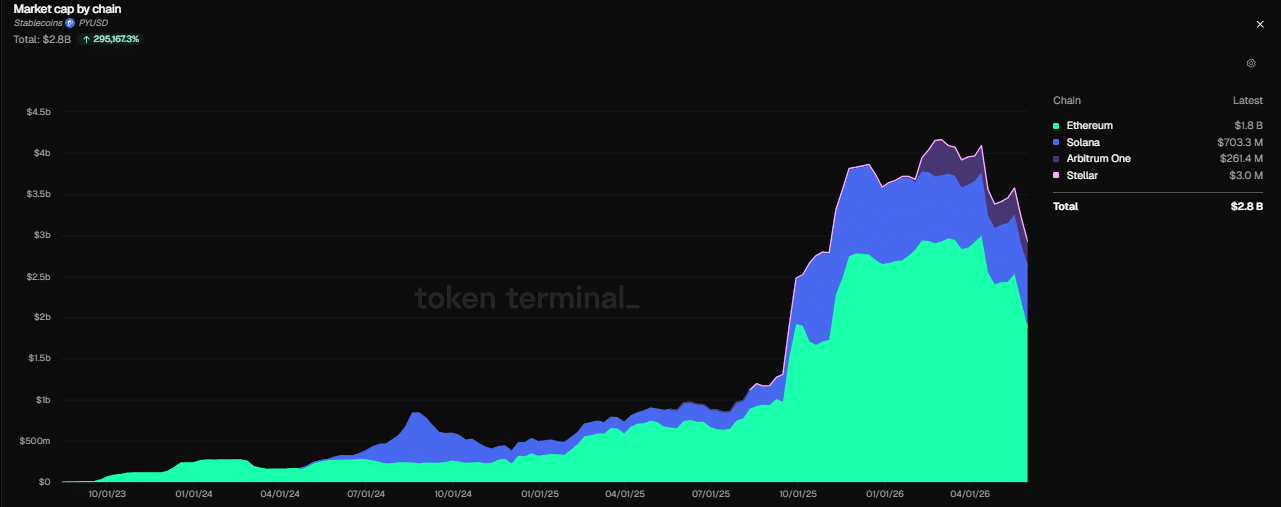

- Current Standing: The asset has seen a massive 35% contraction, with its market cap currently hovering at $2.47 billion. The distribution of this remaining supply is heavily skewed toward the Ethereum network, which holds $1.80 billion. Secondary deployments on Solana ($703 million), Arbitrum One ($261 million), and Stellar Lumens ($3 million) show that while the asset is multi-chain, it lacks the aggressive growth metrics seen in its competitors.

The contraction of PYUSD highlights a critical lesson in stablecoin economics: brand recognition alone is insufficient to sustain liquidity. Success requires deep integration into lending protocols, cross-chain bridges, and decentralized exchanges—areas where Tether and Circle have spent years perfecting their reach.

Supporting Data: The Dominance of the Incumbents

The divergence between PYUSD and the market leaders is further evidenced by the transaction volume data. When examining weekly asset transfer counts, the chasm between the leaders and the rest of the pack is stark.

For the past week, USDC recorded an asset transfer count of $133.6 million, while Tether outperformed it with $176.9 million. When looking at broader issuer metrics, the difference is even more pronounced: USDT recorded 176 million weekly transfers compared to a staggering 392 million across broader stablecoin issuer ecosystems.

Growth Metrics Comparison

- USDC: Over the last month, USDC’s asset transfer count surged by 27%, reaching $466 million. Furthermore, the holder base for USDC grew by 4.7%.

- USDT: Tether continues to grow at a massive scale, with a 2.1% increase in transfer volume, bringing its total to approximately $1.40 trillion. Its holder base saw an increase of over 5%, proving that even with a massive existing user base, the network effect of Tether remains potent.

Circle’s recent minting of $750 million in USDC on the Solana network within a 24-hour window serves as a tactical response to the increasing demand for high-speed, low-cost transaction environments. This brings their total market cap to approximately $74.78 billion, further solidifying their position as the go-to stablecoin for institutional developers.

Official Responses and Market Perspectives

Industry leaders remain bullish on the long-term prospects of the sector. The shift is no longer just about USD-pegged tokens; the market is seeing an expansion into Euro-pegged and Yen-pegged assets, reflecting a move toward a truly globalized digital financial system.

Rob Hadick, a general partner at Dragonfly, has been vocal about the transformative potential of this technology. Hadick suggests that the stablecoin market is poised for a 10x growth multiplier as payment adoption moves beyond speculative trading and into the realm of real-world commerce. According to Hadick, stablecoins are effectively "collapsing the existing financial infrastructure." By removing the need for correspondent banks, manual settlement processes, and traditional payment rails, stablecoins reduce dependency on slow, expensive intermediaries.

Smaller players are also attempting to capture this wave. For instance, payment infrastructure provider Tempo recently saw a 35% surge in its stablecoin supply in a single week, bringing its total to $30 million. While this is a small drop in the ocean compared to the $300 billion+ market, it serves as a proof-of-concept for the rapid scalability of private stablecoin issuance.

Implications: The Future of Decentralized Finance

The contraction of PYUSD and the simultaneous expansion of USDC and USDT hold significant implications for the future of the crypto-economy.

1. The Consolidation of Liquidity

The "flight to quality" is a well-known phenomenon in traditional finance, and it is now playing out in the stablecoin market. Traders and institutions are increasingly favoring assets with proven transparency, deep liquidity, and multi-chain availability. This suggests that the market may move toward a "winner-takes-most" scenario, where new entrants face an almost insurmountable barrier to entry unless they offer a unique technological edge or superior regulatory compliance.

2. Multi-Chain Interoperability

The aggressive expansion of USDC on Solana and Arbitrum indicates that the future of stablecoins is not tied to a single network. As decentralized applications (dApps) grow more complex, the ability to move stablecoins seamlessly between chains will be the deciding factor in which assets dominate. Circle’s strategic focus on Solana—a chain known for high throughput—shows that they are positioning themselves for the next generation of high-frequency consumer applications.

3. The End of Intermediary Dependency

As noted by market analysts, the ultimate goal of the stablecoin sector is to bypass the inefficiencies of the legacy banking system. When $4.4 billion can be transferred in a single transaction to a decentralized deployer, the value proposition of a traditional SWIFT transfer becomes increasingly obsolete. This shift poses a direct challenge to retail and investment banks, which have historically profited from the friction in global capital flows.

4. Regulatory Vigilance

With a combined market cap exceeding $300 billion, regulators are taking notice. The continued dominance of Tether and the institutional-grade operations of Circle suggest that the sector is entering a phase of "professionalization." Future growth will likely be dictated by which stablecoin issuers can best satisfy global regulatory bodies while maintaining the permissionless, decentralized nature that makes these assets attractive in the first place.

Final Summary: The Path Ahead

The stablecoin sector stands at a crossroads. While the decline of PYUSD might appear to be a setback for institutional adoption, it is more accurately a correction that highlights the necessity of utility and ecosystem depth over pure brand power. Tether and Circle remain the pillars upon which the current digital asset economy is built, and their ability to scale, move, and integrate across various chains remains the gold standard.

As we look toward the potential 10x growth predicted by industry experts, the focus will shift from simple market cap to utility-driven metrics: transaction volume, gas efficiency, cross-chain liquidity, and real-world payment integration. The coming years will be defined by the maturation of these digital assets as they move from the fringes of crypto-trading into the mainstream fabric of global commerce, forever altering how value is transferred across borders.