The Decentralized Finance (DeFi) ecosystem, once heralded as the immutable future of global finance, is facing its most significant reckoning to date. As of mid-2026, the sector is grappling with a profound crisis of confidence, characterized by a persistent, systemic drainage of capital and an unprecedented surge in malicious exploitation. The industry, which reached heady heights of over $150 billion in Total Value Locked (TVL) in late 2025, has since retreated into a defensive posture, struggling to retain liquidity in an increasingly hostile security environment.

The State of the Market: A 39% Erosion of Trust

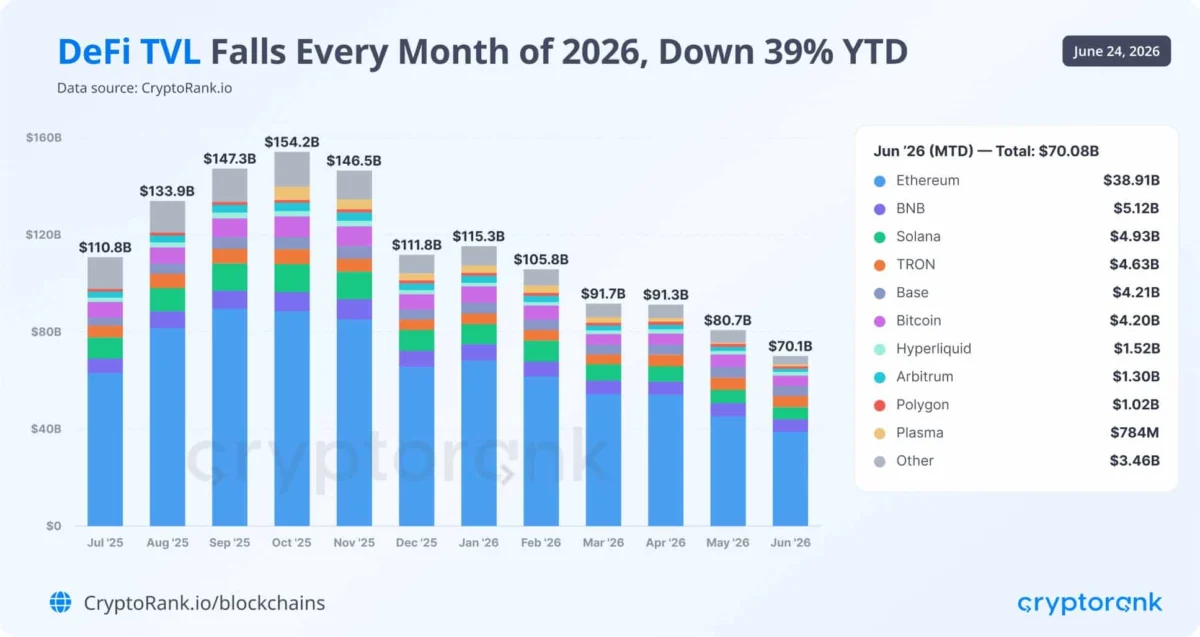

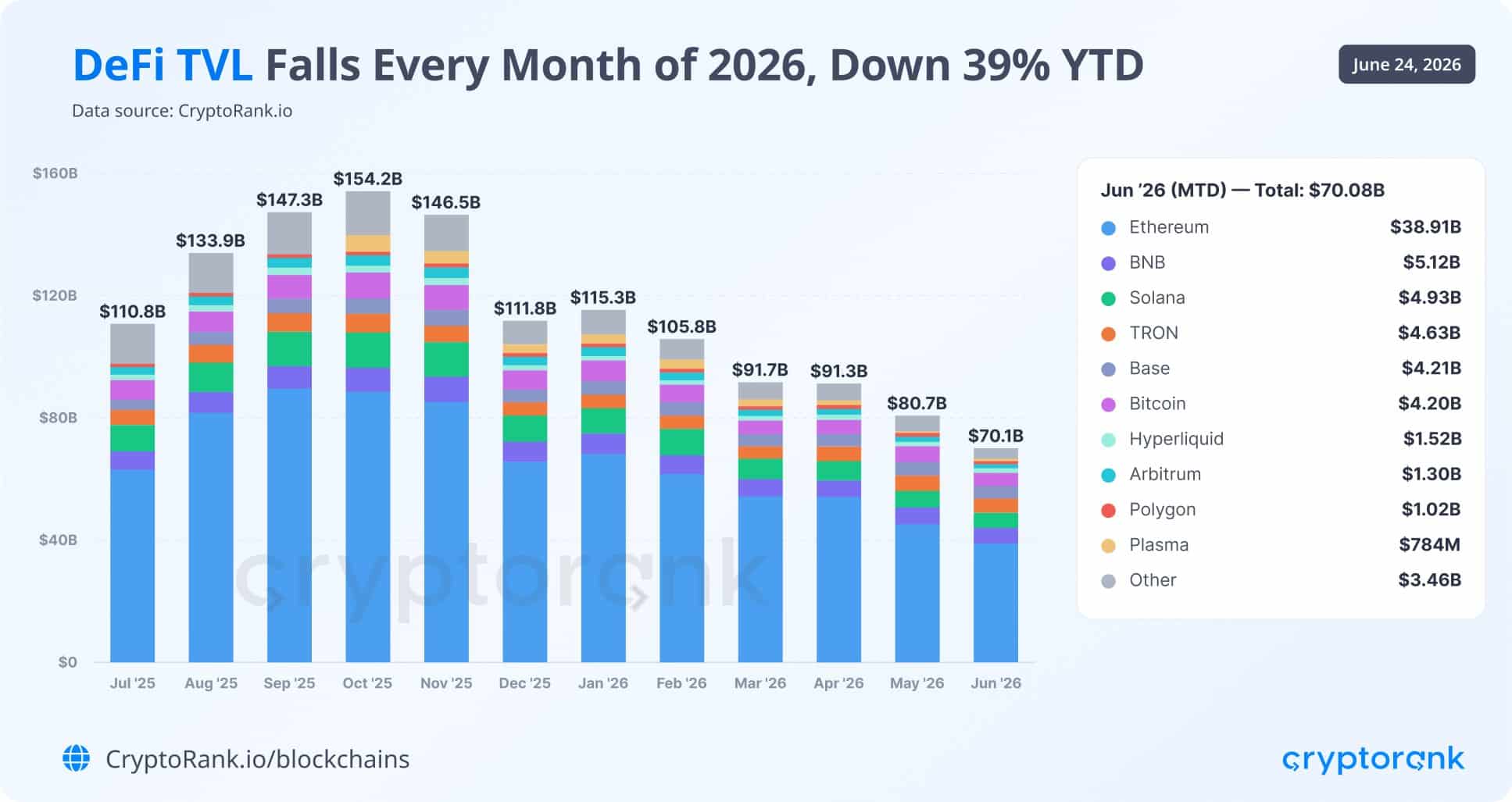

The year 2026 has been marked by a relentless downward trend in the capital base of decentralized protocols. According to comprehensive data from market intelligence firm CryptoRank, the industry has witnessed a consistent month-over-month decline in TVL since January.

At the start of the year, the sector commanded approximately $115 billion in liquidity. By the end of June, that figure had plummeted to roughly $70 billion. This represents a year-to-date (YTD) decline of nearly 39%, a stark indicator that the market’s contraction is not a fleeting volatility event, but a fundamental reallocation of capital.

This retreat stands in stark contrast to the momentum observed in the final quarter of 2025. During that period, DeFi protocols were flush with capital, fueled by optimism and an influx of retail and institutional interest. However, as the market environment shifted, investors began aggressively de-risking, pulling liquidity from experimental and high-yield protocols in favor of safer assets or off-chain alternatives.

The Landscape of Declining Dominance

Ethereum, long the bastion of DeFi liquidity, has not been immune to this trend. Despite maintaining the largest market share, Ethereum’s dominance has failed to insulate its ecosystem from the broader market malaise. Almost every major blockchain network has felt the pressure of this capital exodus.

There are, however, outliers. TRON (TRX) and Hyperliquid (HYPE) have emerged as rare bright spots, posting growth of 5% and 7% respectively throughout the year. Analysts suggest that these exceptions may be attributed to specific use-case utility or unique liquidity incentive programs that have managed to buck the prevailing industry trend.

Chronology of a Security Crisis

The erosion of TVL is inextricably linked to the rising tide of cybersecurity breaches. The correlation between the frequency of hacks and the outflow of capital has become impossible to ignore.

Q1 to Q2 2026: The Height of Vulnerability

The first half of 2026 has been defined by a relentless series of smart contract exploits and bridge vulnerabilities. The severity of the situation became clear in the second quarter, which recorded a staggering 85 individual hacks—marking it the busiest quarter for crypto exploits by incident count in the history of the sector.

The cumulative data for the first half of the year is sobering: 121 confirmed hacks resulting in nearly $1 billion in total losses. While the total dollar value of these losses has not yet surpassed the historical peaks seen in the most catastrophic years of crypto history, the frequency of the attacks has created a persistent state of anxiety among liquidity providers.

The chronological progression of these attacks shows a shift in methodology. Early 2026 exploits focused heavily on minor protocols with underdeveloped audit histories. However, by late Q2, the sophistication of these attacks increased, targeting cross-chain bridges and lending protocols that were previously considered "blue-chip" components of the DeFi stack.

Supporting Data: Why Liquidity is Fleeing

To understand the exodus, one must look at the relationship between TVL and the broader stablecoin economy. Previous reporting by AMBCrypto highlighted a glaring discrepancy: while DeFi TVL has cratered from its highs of $178 billion to approximately $72.5 billion, the total stablecoin supply has remained remarkably resilient, hovering near $315 billion.

This suggests that capital has not necessarily exited the cryptocurrency market entirely; rather, it has shifted from "productive" DeFi assets to "static" stablecoin holdings. Investors are choosing to hold USDT, USDC, and other stable assets in custodial wallets or centralized exchanges rather than risking them in DeFi protocols to earn yield. This behavior is a direct response to the "security tax"—the risk premium that investors now demand before they are willing to lock their funds into a smart contract.

The Security Paradigm: A Professional Analysis

The current crisis has forced a re-evaluation of how security audits are conducted and how code is deployed. The sheer volume of exploits has brought several critical issues to the forefront of industry discourse:

1. The Audit Illusion

Many of the protocols that suffered exploits in 2026 were, in fact, "audited." This has led to a growing consensus among developers and investors that traditional static code audits are insufficient to address the complexities of modern, composable DeFi. The focus is shifting toward "runtime security"—tools that monitor smart contract activity in real-time and can pause operations if an anomaly is detected.

2. The Complexity Trap

As DeFi protocols add layers of complexity, such as automated market makers (AMMs), lending loops, and yield aggregators, the attack surface expands exponentially. Many of the 121 hacks this year were the result of "logical errors" that were too complex to be caught in a standard pre-deployment review.

3. The Institutional Response

Institutional investors, who were just beginning to integrate DeFi into their portfolios, have become significantly more selective. The due diligence process has shifted from analyzing potential Annual Percentage Yield (APY) to performing deep forensic analysis on protocol governance, multisig wallet security, and the track record of the development team.

Implications for the Future of DeFi

The implications of this 39% TVL decline are profound and will likely reshape the industry for years to come.

A Move Toward Regulation and Insurance

The high frequency of hacks is accelerating the demand for on-chain insurance products. Investors are increasingly looking for protocols that bundle security coverage or operate under decentralized insurance covers (like Nexus Mutual). Furthermore, the rising number of exploits is providing additional ammunition for regulators who argue that the DeFi sector lacks the consumer protections necessary for mass adoption.

The Survival of the Fittest

The current market contraction acts as a brutal, yet effective, filter. Protocols that survive the 2026 "bear market in security" will likely be those that prioritize robustness over rapid feature deployment. The industry is witnessing a consolidation phase where "vampire attacks" and aggressive yield farming are losing out to protocols that offer high-security, transparent, and audited infrastructure.

The "Confidence Gap"

Perhaps the most significant implication is the "confidence gap." Trust is an intangible asset that takes years to build and seconds to destroy. With 121 hacks occurring in six months, the industry is struggling to convince the average user that their funds are safe. This trust deficit is likely to keep TVL suppressed until a new generation of security-first protocols can establish a consistent, incident-free record over a sustained period.

Conclusion

The year 2026 will likely be remembered as the year DeFi grew up. The transition from a "move fast and break things" ethos to one of institutional-grade security is proving to be a painful, expensive process.

The $1 billion lost to hackers is more than just a financial figure; it is a signal that the infrastructure of the decentralized web is still in its infancy. For DeFi to reclaim its $150 billion-plus valuation, the industry must solve the paradox of security: it must be as accessible as a centralized bank while maintaining the permissionless nature of a blockchain. Until protocols can demonstrate an ironclad defense against the rising frequency of exploits, capital will remain on the sidelines, and the recovery of the total value locked will remain, as current trends suggest, frustratingly uneven.