The promise of decentralization has long been the ideological bedrock of the cryptocurrency industry. Proponents argue that blockchain technology exists outside the purview of traditional institutional control, shielded by cryptographic proofs and immutable ledgers. However, the events of the second quarter of 2026 have provided a sobering reminder: decentralization does not grant immunity from regulatory gravity.

As the market expanded globally, Tether’s USDT—the linchpin of the crypto economy—became the bridge between the chaotic, permissionless world of DeFi and the rigid, compliance-heavy infrastructure of fiat banking. But that bridge is currently under siege. Following Tether’s strategic decision to forgo compliance with the European Union’s Markets in Crypto-Assets (MiCA) regulation, a tectonic shift is underway. With major exchanges delisting the asset for EU residents and liquidity beginning to drain from the ecosystem, the industry is left to grapple with a harsh reality: even the most "decentralized" assets rely on centralized chokepoints to survive.

The Centrality of Decentralized Rails: The Tether Paradox

At the heart of this disruption lies a fundamental tension. While USDT functions on decentralized blockchains, its utility is predicated on its integration with centralized exchanges (CEXs). These platforms serve as the primary on-ramps and off-ramps for global capital. When the EU implemented MiCA—the world’s first comprehensive regulatory framework for crypto—it effectively set a "regulatory moat" around the European market.

Tether’s refusal to seek MiCA approval was a calculated move, likely to avoid the transparency and operational requirements mandated by Brussels. The consequence, however, has been immediate and severe. Major global exchanges, including Binance, Coinbase, and Kraken, have systematically removed USDT pairs for users within the European Economic Area (EEA) to remain in good standing with EU regulators. This has effectively severed the umbilical cord between the world’s largest stablecoin and one of the world’s most significant financial markets.

Chronology of a Regulatory Schism

The unfolding crisis did not happen overnight. It is the culmination of a long-standing standoff between the issuer of the world’s largest stablecoin and the European regulatory apparatus.

- Q1 2026: As MiCA enforcement dates approached, industry analysts speculated on how stablecoin issuers would handle the stringent reserve and operational mandates.

- Early April 2026: Tether officially signals its reluctance to adhere to the full scope of MiCA, citing structural incompatibilities and the potential for regulatory overreach.

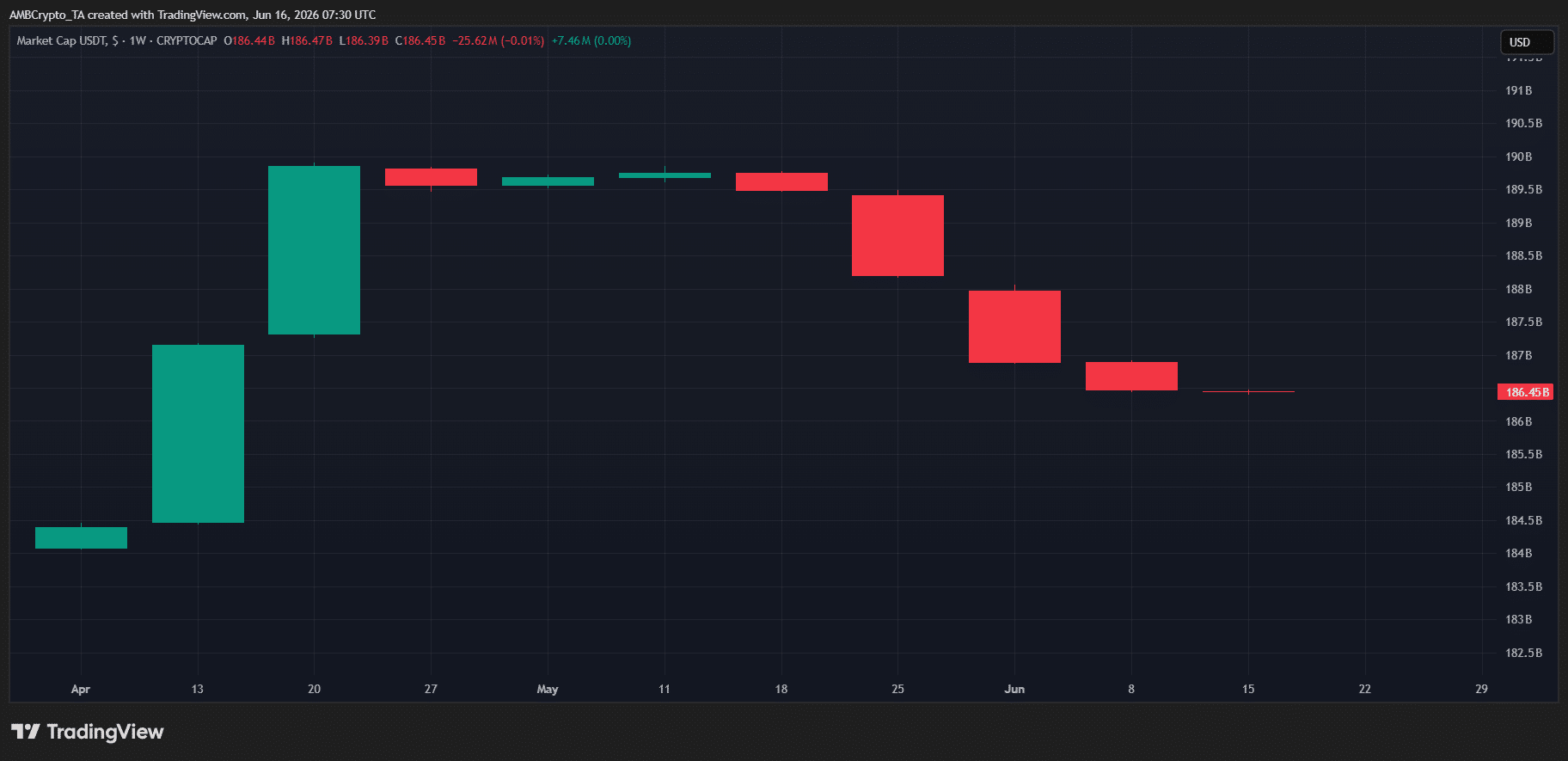

- Late April – May 2026: The stablecoin market reaches an all-time high, peaking at $321 billion in total market capitalization. USDT, commanding the lion’s share, hits a record valuation near $190 billion.

- June 2026 (The Turning Point): With the EU mandate fully enforceable, top-tier exchanges formally announce the delisting of USDT for EU residents.

- Mid-June 2026: Data from on-chain analytics reveals a consistent bleed. USDT market cap begins a downward trend, shedding approximately $3 billion in value in mere weeks.

- Present Day: The market finds itself in a state of flux, with investors pivoting toward "MiCA-compliant" alternatives while simultaneously questioning the broader health of crypto liquidity.

Data Analysis: The Liquidity Bleed

In a "risk-on" market environment, liquidity acts as the lifeblood of price discovery. When liquidity is abundant, traders can execute large orders with minimal "slippage," allowing bullish trends to feed on themselves. Conversely, when liquidity retreats, volatility spikes, and the market becomes brittle.

The current data suggests a troubling contraction. Since the early May peak of $321 billion across the stablecoin sector, the total market cap has shrunk by over $6 billion. While this may seem like a marginal percentage of the total, the concentration of this decline in USDT suggests a targeted retreat from the asset.

Comparative Performance of Stablecoins

The shift in capital has not been uniform. As USDT faces its "EU-exit" induced FUD (Fear, Uncertainty, and Doubt), other assets have attempted to capture the fleeing capital:

- USDC: Despite being viewed as a "compliant" alternative, it has seen a 2.5% monthly decline, suggesting that capital is leaving the stablecoin ecosystem entirely rather than just migrating between tokens.

- RLUSD: A relative outlier, showing a 6.5% increase, though its current liquidity profile is insufficient to offset the total drain caused by the Tether contraction.

This data underscores a critical insight: investors are not simply rotating; they are de-risking.

Official Responses and Strategic Positioning

Tether’s public stance remains one of defiance and focus on global, non-EU markets. Management has consistently argued that their model is designed for global financial inclusion, which they believe transcends the localized regulatory mandates of the European Union. However, their silence on the specific logistical impacts of the EU delisting has fueled market speculation.

Conversely, major exchanges have been vocal about their operational constraints. Their communications have been uniform: compliance with MiCA is not optional. For these entities, the European market is too large to forfeit, and the regulatory penalties for non-compliance are existential. By delisting USDT, they have prioritized regulatory longevity over the preferences of a segment of their user base.

Implications for Q3: A Bearish Setup?

As we look toward the third quarter of 2026, the intersection of geopolitical easing and liquidity tightening creates a complex narrative for crypto investors.

1. The Liquidity Vacuum

The most immediate implication is the tightening of liquidity. With $3 billion in USDT removed from the circulation pool, the "fuel" for the next leg up is arguably lower than it was in Q2. If this trend continues, we may see a "choppy" market where price surges are quickly met with resistance due to a lack of available stablecoin depth.

2. The Fragmentation of the Stablecoin Market

We are entering an era of "balkanized" liquidity. The crypto market is splitting into "MiCA-approved" zones and "off-shore/global" zones. This fragmentation complicates the lives of institutional traders who require seamless, global liquidity to manage their positions.

3. The "Risk-On" Trap

While geopolitical tensions between the U.S. and Iran have eased—historically a signal for risk-on behavior—this macro-tail-wind may be neutralized by the micro-headwind of the stablecoin contraction. If the market continues to see stablecoin outflows, the anticipated Q3 rally could be stifled by an internal lack of capital, even if the external geopolitical environment remains favorable.

Conclusion: The Path Ahead

The Tether-MiCA standoff serves as a watershed moment for the digital asset industry. It proves that while code may be immutable, the on-ramps to the financial system are highly susceptible to the legislative will of sovereign powers.

For the remainder of 2026, the health of the crypto market will be intrinsically tied to the stability of the stablecoin sector. If USDT can weather this period of intense scrutiny and find ways to maintain its market dominance, the industry may return to a period of stability. However, if the "liquidity bleed" accelerates, we may be looking at a structural shift in how crypto markets are capitalized.

Investors should remain cautious. The "decentralization" narrative is powerful, but in the face of multi-billion dollar regulatory shifts, the old-world reality of centralized compliance still holds the whip hand. The Q3 setup is not just about price action; it is about the fundamental plumbing of the digital economy, and for now, that plumbing is leaking.