The global cryptocurrency market currently sits at a pivotal junction, defined by a massive accumulation of stablecoin liquidity that has yet to fully translate into a sustained, parabolic bull run. Recent on-chain data from mid-2026 reveals a significant shift in how this capital is stored, deployed, and distributed across the ecosystem. As the world’s largest exchange, Binance, continues to consolidate its market share, the underlying composition of its reserves—and the behavior of stablecoin holders globally—is undergoing a profound transformation that could dictate the trajectory of the next market cycle.

Main Facts: The Shift in Reserve Composition

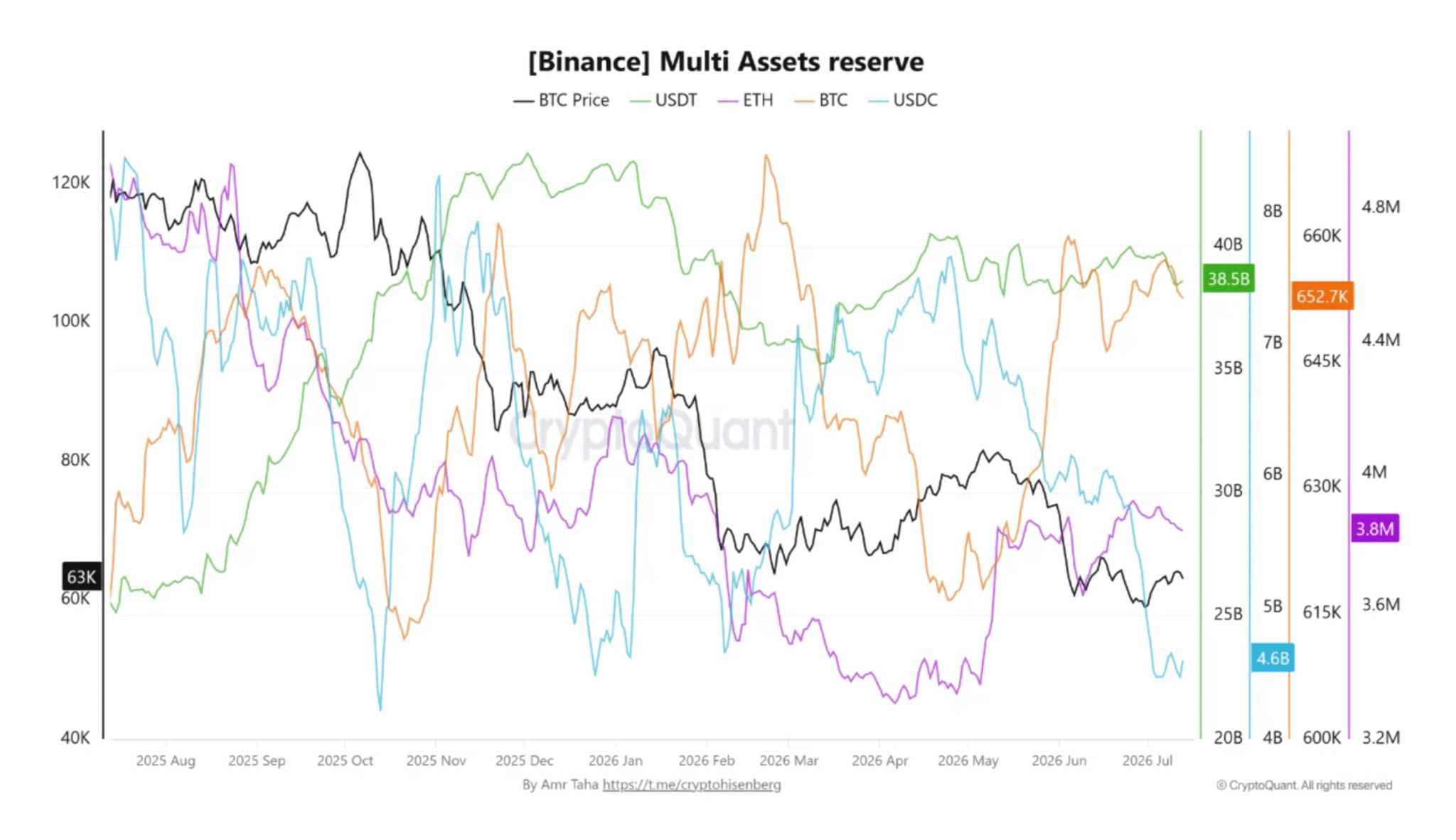

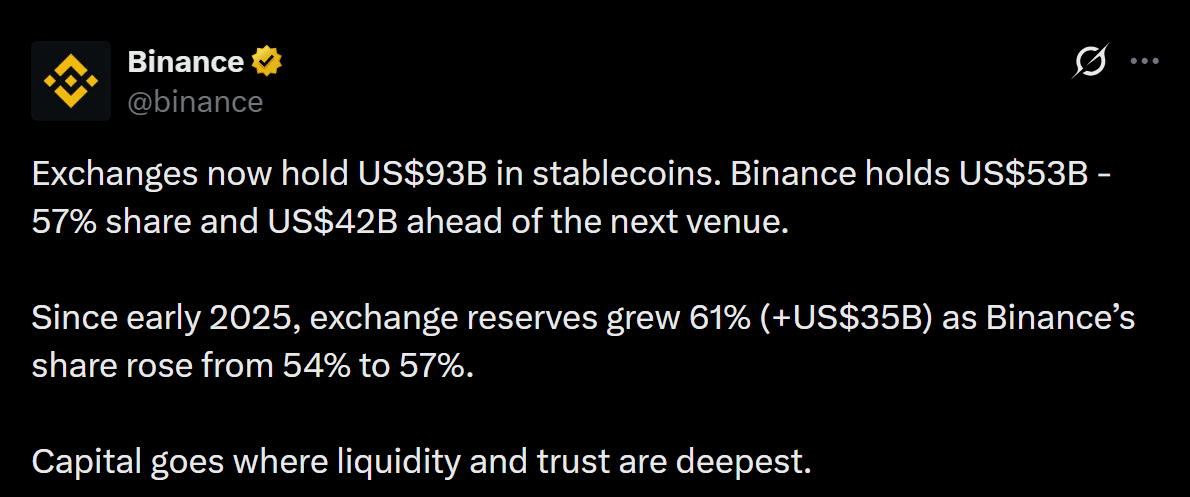

Binance, which currently oversees a staggering $53 billion in stablecoin reserves, remains the central engine of crypto liquidity. This figure represents approximately 57% of the total $93 billion held across major centralized exchanges. However, beneath this headline dominance lies a dramatic divergence between the two industry titans: Tether (USDT) and USD Coin (USDC).

As of July 2026, Binance’s holdings of USDC have undergone a sharp contraction. Reserves of the Circle-issued stablecoin have plummeted by 40.3%, sliding from $7.7 billion to a current valuation of $4.6 billion. This decline effectively reverses the momentum built during the early months of 2026. Conversely, Tether’s position on the exchange has remained remarkably resilient, holding steady at $38.5 billion.

The gap between these two assets on the Binance platform has widened to a cavernous $33.9 billion. This is not merely a statistical anomaly; it serves as a clear signal of market preference. Traders and institutional entities alike are increasingly favoring USDT as their preferred instrument for settlement, liquidity provision, and exchange-based activity, effectively sidelining USDC in favor of its more liquid, legacy-backed counterpart.

Chronology: From Accumulation to Rebalancing

The narrative of stablecoin liquidity since the start of 2025 has been one of explosive growth followed by strategic distribution.

- Early 2025: The market witnessed a rapid expansion in stablecoin reserves held on centralized exchanges, with a cumulative growth of 61%, equating to roughly $35 billion in new capital inflows. During this phase, both USDT and USDC saw significant utility as investors sought shelter from volatility.

- Q1 2026: USDC experienced a brief renaissance as institutional interest favored its regulatory transparency and U.S.-centric backing. Binance’s USDC reserves reached a peak of $7.7 billion, signaling a diversification of the exchange’s balance sheet.

- Q2 2026: The trend began to reverse. A confluence of macro-economic factors and shifting trading pairs saw a flight from USDC back into the high-liquidity environment of USDT.

- July 2026: The current state of play reveals a "settling" of the market. While total reserves remain high, the concentration has shifted away from the top 100 whale wallets, signaling a move toward broader, more decentralized liquidity distribution.

Supporting Data: The Decentralization of Wealth

A critical development in the 2026 landscape is the movement of capital away from "whale" dominance. Data from Santiment indicates that the largest holders—often institutional desks or market makers—are reducing their concentration of stablecoin supply.

Over the past three months, the top 100 USDT wallets have reduced their share of the total supply by 0.6%. More strikingly, the top USDC wallets have slashed their concentration by 4.7%. This trend is indicative of a "democratization" of liquidity. Rather than remaining stagnant in high-net-worth vaults, capital is circulating more freely across decentralized protocols, retail-focused exchange wallets, and institutional lending platforms.

This shift suggests that liquidity is becoming "thinner" in the hands of the few and "deeper" across the broad market. By moving away from a few centralized points of failure or influence, the market is arguably building a more resilient foundation that can better withstand liquidity shocks.

Official Responses and Market Sentiment

While major exchanges have been relatively quiet regarding the specific shift in reserve ratios, the broader crypto-financial community—including researchers from CryptoQuant and various market analysts—has highlighted that this is likely a structural evolution rather than a reactionary one.

Market participants argue that the preference for USDT is driven by its ubiquity in cross-chain ecosystems and its deep integration into DeFi protocols that require high-velocity assets. USDC, while considered a "safer" regulatory bet, is often perceived as a "yield-bearing" or "long-term storage" asset rather than an active trading tool. Consequently, as the velocity of money on exchanges has increased, the natural gravitational pull has been toward USDT.

However, analysts remain cautious. While the total stablecoin supply remains near a massive $312 billion, the anticipated "bull run" fueled by this capital has yet to manifest. The current consensus among analysts is that the capital is waiting for a catalyst—be it regulatory clarity, interest rate pivots, or a breakout in primary assets like Bitcoin.

Implications: The Path to the Next Rally

The most profound implication of these findings is that the availability of capital no longer serves as a guarantee of market movement. The market is currently in a state of "liquidity readiness."

1. The Velocity of Capital

The transition of stablecoins from whale wallets to a broader user base is a bullish signal for market health. It implies that a larger segment of the market is prepared to enter positions at a moment’s notice. However, as the data shows, having the "dry powder" is not the same as pulling the trigger. The market requires active wallet creation and an uptick in daily transactions to convert these reserves into genuine demand.

2. The Dominance of USDT as a Settlement Layer

If the current trend persists, USDT is set to become the undisputed standard for settlement in the crypto-asset class. This poses a potential long-term risk regarding centralization, but in the short term, it provides the efficiency and liquidity depth required for high-frequency trading. Binance’s strategic position as the primary holder of this liquidity effectively makes it the central bank of the crypto-economy.

3. The "Sidelined" Problem

Despite the record-breaking levels of stablecoin reserves, risk asset accumulation remains stagnant. This suggests that the current cycle is defined by hesitation. Investors are keeping their funds in stablecoins to hedge against potential downturns rather than deploying them into higher-beta assets. For a sustainable bull run to occur, we must see a reversal of this behavior, where stablecoin outflows into BTC, ETH, and other altcoins begin to outpace inflows into exchanges.

Conclusion: A Resilient Foundation

The state of the market in mid-2026 is one of quiet tension. The structural shift of reserves—from the wallets of the elite few to the broader user base—and the consolidation of liquidity within the USDT ecosystem on Binance indicate a market that is structurally stronger than it was in 2025.

However, the "Great Rebalancing" has yet to ignite the next rally. The fundamental question remains: Will the current liquidity stay on the sidelines, or will the increasing accessibility of these funds finally catalyze a new wave of market growth? As it stands, the capital is ready, the infrastructure is robust, and the distribution is healthier than ever. The only missing ingredient is the investor sentiment required to turn these reserves into the fuel for the next generation of market expansion. Investors should watch for increased on-chain velocity as the ultimate metric for when this sidelined capital finally enters the arena.