The Indian cryptocurrency market is currently grappling with a significant structural disruption: a persistent and ballooning premium on Tether (USDT). While historical fluctuations in the USDT/INR exchange rate typically hovered within a manageable 3% to 4% range, recent market data indicates that the premium has surged beyond 8.5%. This widening spread is not merely a transient pricing anomaly; it is a clear indicator of a fundamental breakdown in liquidity, driven by an increasingly stringent regulatory environment and the resulting contraction in stablecoin availability.

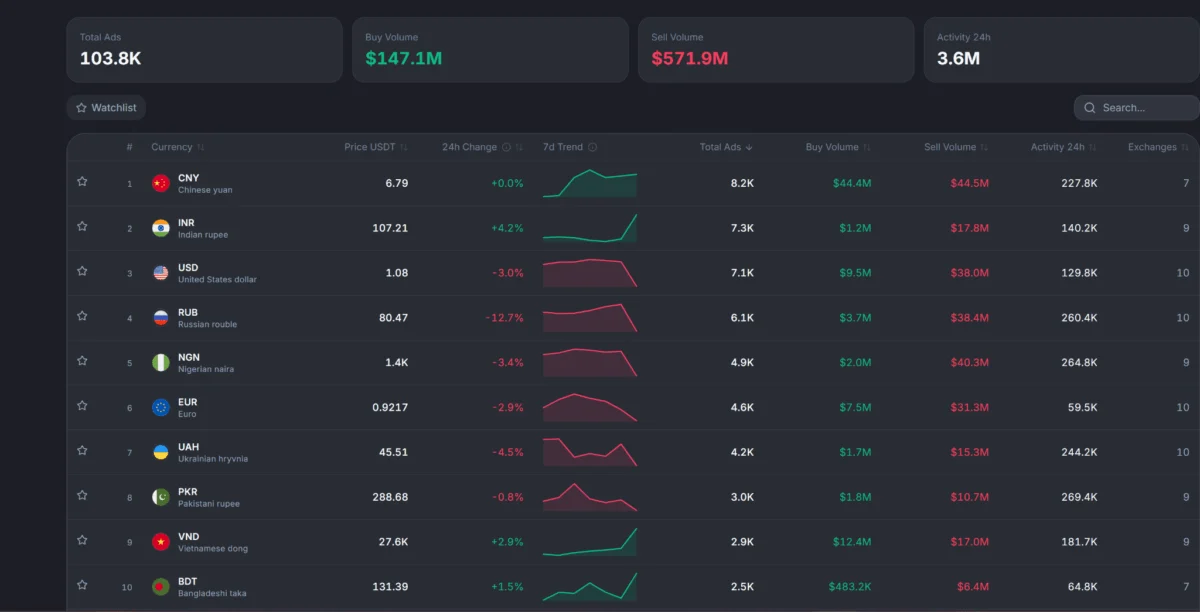

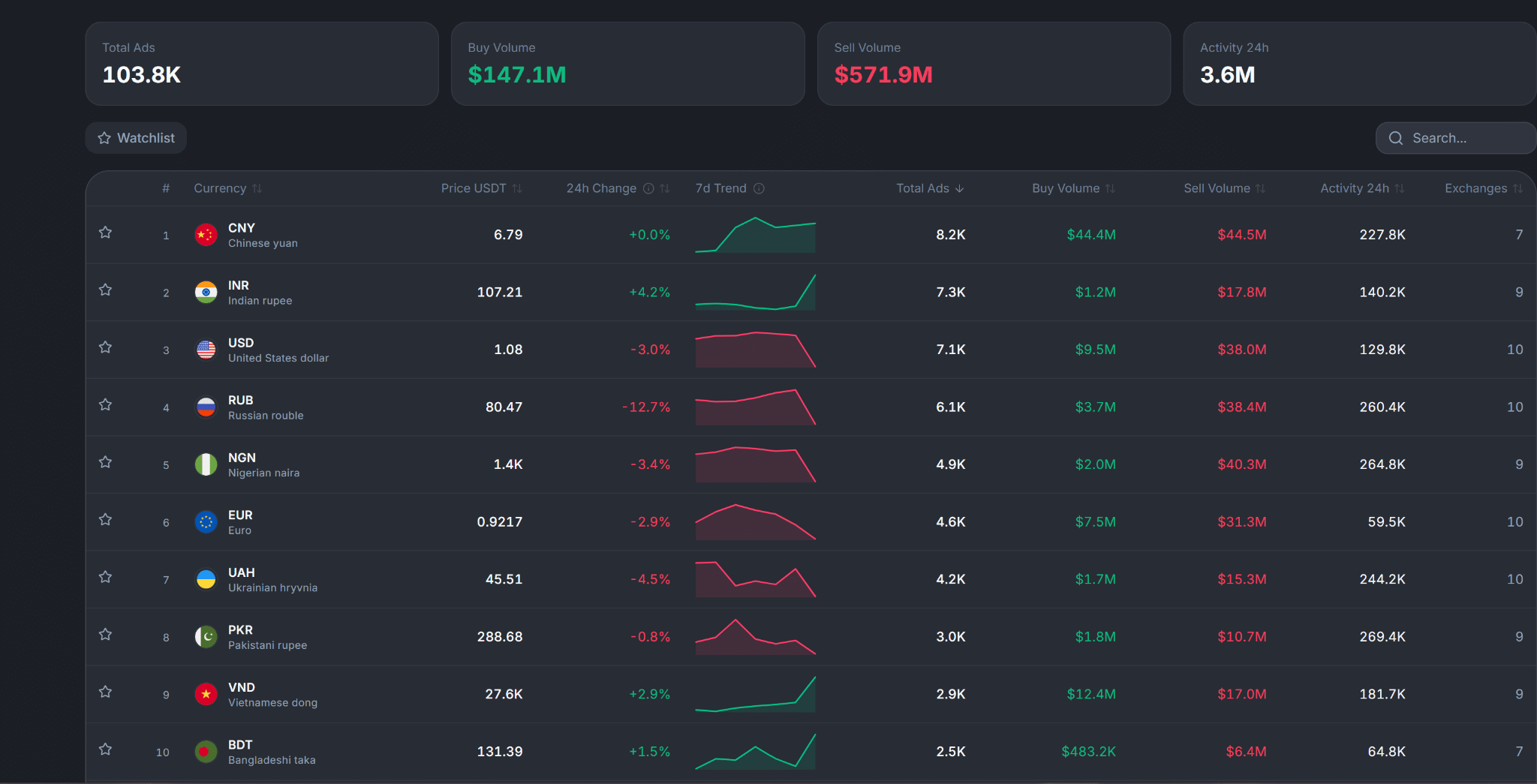

As the official USD/INR exchange rate sits at approximately ₹94.65, the market price for USDT in India has climbed as high as ₹107.21, reflecting a disconnect between local demand and the ability of the market to source dollar-pegged assets.

Main Facts: The Anatomy of a Market Imbalance

The current crisis centers on the scarcity of USDT within the domestic Indian ecosystem. USDT serves as the lifeblood for the country’s crypto-economy, acting as the primary medium for cross-border settlements, trade finance, and a hedge against local currency volatility. However, the mechanism that usually keeps this price in check—arbitrage—is failing.

Arbitrageurs rely on the ability to freely move capital in and out of the ecosystem to profit from price discrepancies. When the price of USDT rises in India, traders would typically buy USDT abroad and sell it locally, effectively increasing supply and pushing the price back toward parity. Currently, that flow has been stemmed. Regulatory oversight, enforcement actions targeting Virtual Digital Asset (VDA) platforms, and a general climate of caution have discouraged the influx of capital required to normalize these markets.

Key Drivers of the Premium:

- Supply Contraction: Fresh inflows of USDT into Indian P2P (peer-to-peer) markets and OTC (over-the-counter) desks have plummeted.

- Regulatory Enforcement: Increased scrutiny on VDA transfers, specifically regarding a reported ₹2,500 crore in volume, has forced major liquidity providers to scale back operations.

- Market-Making Failure: The disparity between buy and sell volumes is stark. With buy volumes reaching only $1.2 million against $17.8 million in sell volume, it is clear that market makers are unable to fulfill their traditional role of providing two-way liquidity.

Chronology: How the Spread Widened

The path to the current 8.5% premium was not sudden, but rather a cumulative result of mounting pressures over several months.

Phase 1: Increased Oversight (Early 2024)

Following global trends in crypto regulation, Indian authorities began intensifying their focus on anti-money laundering (AML) and know-your-customer (KYC) protocols for VDA service providers. This created an initial "friction cost" for moving capital into the crypto ecosystem.

Phase 2: Enforcement Spikes

The situation intensified as regulators zeroed in on specific large-scale VDA transfers, notably the investigation into ₹2,500 crore worth of crypto transactions. This led to a "chilling effect" among institutional market makers and OTC desks, who began restricting their exposure to avoid potential legal entanglements.

Phase 3: The Liquidity Crunch

As inflows dried up, the existing supply of USDT became increasingly concentrated. While the number of active wallet addresses and total transaction volumes remained high—suggesting that the need for USDT had not waned—the capacity to satisfy that demand evaporated. By the middle of the second quarter, the premium began to break through the 5% barrier, eventually pushing past the 8% mark as the supply-demand gap widened.

Supporting Data: Analyzing the Market Microstructure

The data provided by P2P platforms paints a bleak picture of market efficiency. At press time, while the daily transaction count exceeded 140,000, the monetary value of those transactions remained disproportionately low. This indicates that retail users are still attempting to transact, but they are doing so in an environment where large-scale liquidity is absent.

The Volume Discrepancy

The most telling metric is the ratio between buy and sell orders. In a healthy market, these should be balanced. In the current Indian context, the $1.2 million buy volume versus the $17.8 million sell volume illustrates a market that is fundamentally "broken."

- Retail vs. Institutional: While retail demand remains robust, the absence of institutional "market makers" means that large orders cannot be filled without triggering massive price slippage.

- On-Chain Evidence: Data from both centralized exchanges and decentralized on-chain flows confirm that there have been minimal "top-ups" to local inventory. The lack of fresh replenishment into the Indian ecosystem suggests that arbitrageurs are actively avoiding the market due to the high compliance risks associated with moving funds in the current regulatory climate.

Official Responses and Regulatory Posture

While there has been no single "ban" on USDT, the cumulative impact of various regulatory initiatives has effectively squeezed the asset out of the mainstream financial path. The government and financial regulators have historically maintained a cautious, and at times hostile, stance toward virtual digital assets.

The focus of current enforcement is primarily on the prevention of capital flight and the curbing of money laundering through decentralized channels. By increasing the compliance burden on exchanges and P2P platforms, authorities have inadvertently created a "regulatory moat" that keeps fresh, low-cost capital from entering the Indian crypto market.

Industry participants argue that the government’s approach is "pro-compliance but anti-liquidity." By failing to provide a clear, sustainable framework for how VDA providers can operate, the current environment has forced the market to rely on informal and fragmented channels.

Implications: The Future of the Indian Crypto Market

The persistence of this elevated premium carries severe, long-term consequences for the Indian digital economy.

1. Shift to Informal Channels

If the premium remains high, traders and businesses will likely bypass traditional, monitored platforms in favor of informal or "underground" trading channels. This is the exact opposite of what regulators typically intend, as it reduces visibility and increases the risks of fraud, scams, and illicit activity.

2. Economic Inefficiency

For businesses that rely on USDT for cross-border settlements, the 8.5% premium acts as an "unspoken tax." This increases the cost of doing business, undermines India’s competitive position in the global digital service economy, and discourages the adoption of blockchain-based financial infrastructure.

3. The Risk of "Digital Isolation"

If the premium becomes a permanent feature, the Indian crypto market risks becoming an isolated "walled garden." When local prices are significantly higher than global benchmarks, the market loses its utility as a bridge to global liquidity. This will ultimately stifle innovation and drive talent and capital toward more crypto-friendly jurisdictions.

Conclusion: The Path to Normalization

The current USDT premium is a symptom of a deeper malaise: a lack of regulatory clarity that prevents the efficient flow of capital. To restore market efficiency, several steps are necessary:

- Clearer Regulatory Frameworks: Moving beyond enforcement-led regulation toward a comprehensive, transparent framework would allow institutional market makers to re-enter the space with confidence.

- Improved Market Access: Establishing compliant "on-ramps" and "off-ramps" that are recognized by regulators would allow for better inventory management, reducing the reliance on volatile P2P markets.

- Encouraging Institutional Participation: By providing a legal "safe harbor" for liquidity providers who adhere to strict AML and KYC standards, the government could stabilize the supply of stablecoins.

Until such changes occur, the Indian stablecoin market will likely remain fragmented, expensive, and increasingly reliant on non-standardized channels. The goal for stakeholders should be to bridge the gap between necessary regulatory oversight and the practical realities of a globalized, digital-first economy. Only by narrowing this pricing gap can India hope to regain its status as a competitive and efficient player in the global digital asset space.