The digital asset ecosystem is currently navigating a period of profound transition. While the broader cryptocurrency markets grapple with ongoing volatility and price stagnation, the stablecoin sector—the bedrock of crypto liquidity—is demonstrating remarkable resilience. Rather than succumbing to the broader market malaise, the stablecoin market has stabilized, signaling a shift in how capital is being deployed and utilized across the digital economy.

With a total market capitalization hovering near the $315 billion mark, stablecoins have evolved from mere "on-ramps" for speculative trading into essential infrastructure for global finance. This transition is marked by a clear divergence: while the aggressive, high-velocity capital inflows characteristic of bull markets have slowed, the structural integration of these assets into institutional and real-world payment frameworks has accelerated.

Main Facts: A Market in Transition

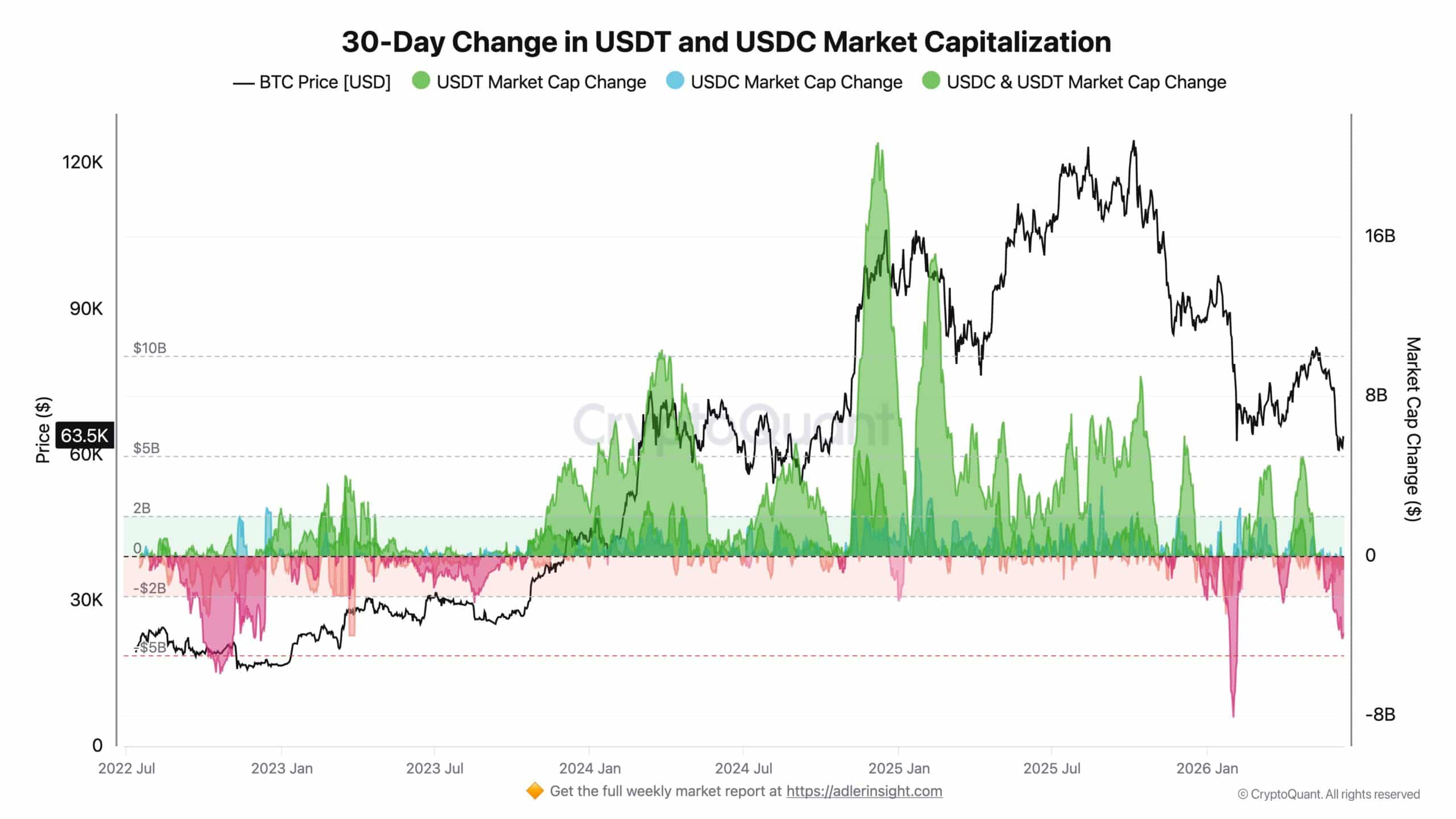

The current state of the stablecoin market is defined by a paradox: slowing exchange-based inflows paired with deepening systemic utility. Earlier this year, in February, the market experienced a significant liquidity crunch, with monthly outflows from major assets like Tether (USDT) and USD Coin (USDC) approaching $8 billion.

However, recent data indicates that this hemorrhaging of capital has largely abated. Outflows have decelerated to approximately $4 billion per month, suggesting that the "flight to fiat" has reached a plateau. Investors are no longer exiting the ecosystem in a panic; instead, they are holding their positions in stable assets, waiting for clearer signals from the broader macro environment.

Key takeaways from the current landscape include:

- Stabilization of Supply: The total supply of stablecoins has ceased its decline, indicating a floor in market demand.

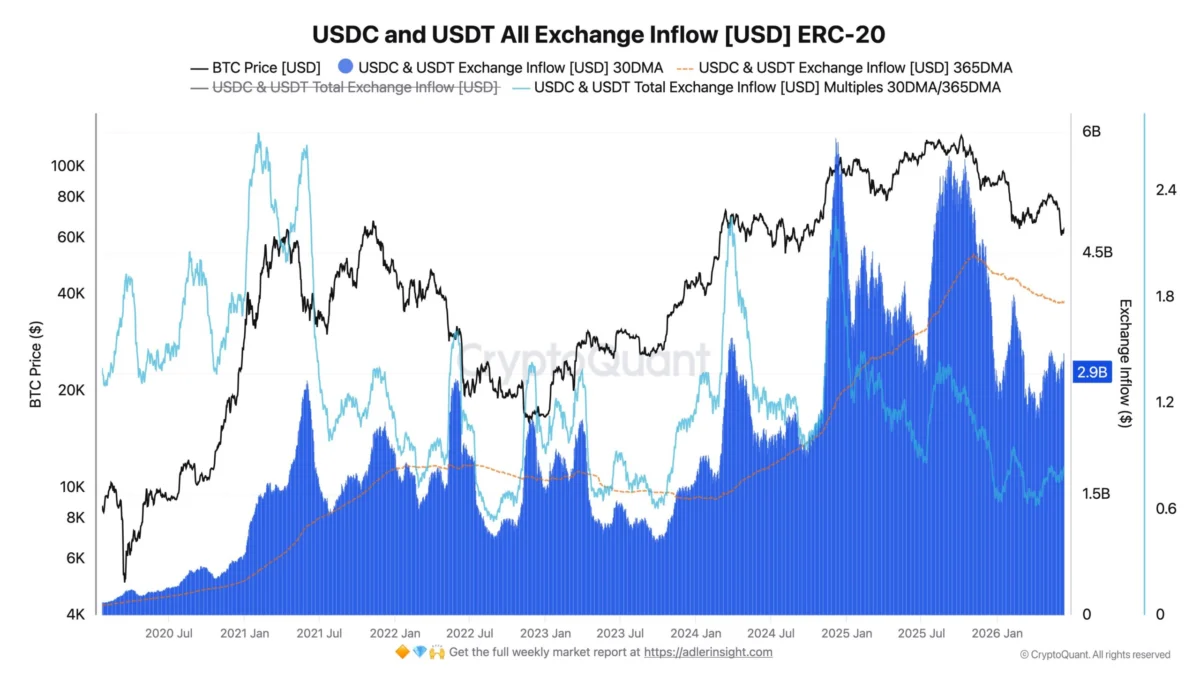

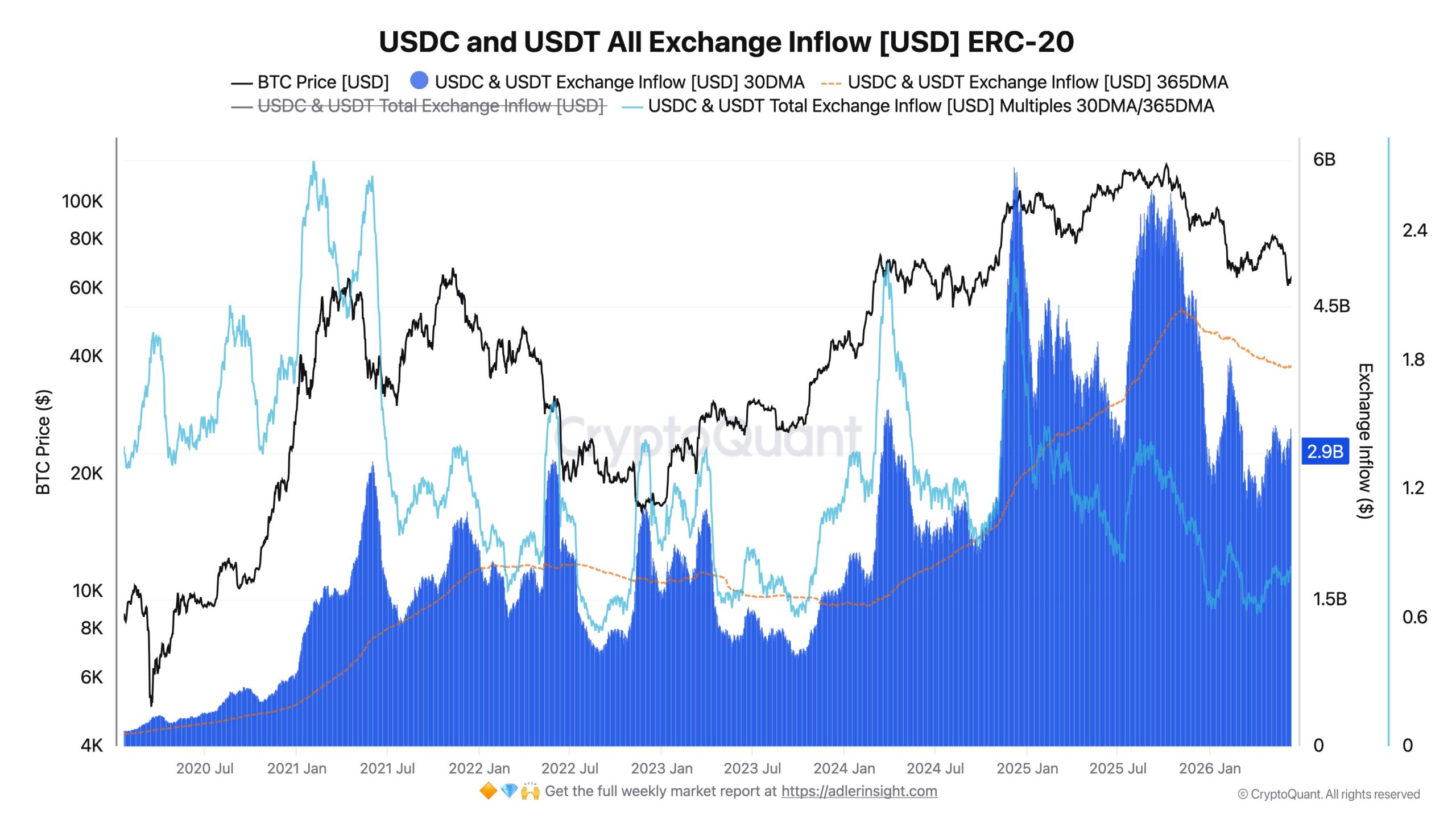

- Reduced Velocity: Exchange-based inflows have dropped from peaks of over $15 billion to a more modest $2.9 billion per month.

- Structural Integration: Stablecoins are increasingly being held in regulated investment vehicles, such as the recently approved T. Rowe Price Active Crypto ETF.

- Real-World Utility: Payments and settlement volumes are decoupling from crypto-market price action, with $390 billion in transaction volume recorded in 2025 alone.

Chronology of Market Shifts

To understand the current state of the market, one must examine the progression of capital flows over the last eighteen months.

The Peak of Speculative Inflow (Q1-Q3 2025)

During the height of the previous market cycle, the influx of capital into centralized exchanges was aggressive. Investors sought to capitalize on Bitcoin’s (BTC) upward trajectory, leading to monthly stablecoin inflows regularly exceeding $15 billion. During this period, stablecoins acted primarily as "dry powder"—capital sitting on the sidelines, ready to be deployed into high-beta assets at a moment’s notice.

The Correction and Contraction (Q4 2025 – Q1 2026)

As market sentiment shifted, the pace of inflows began to weaken. The "0.77 ratio"—a key metric tracking the relationship between stablecoin deposits and market momentum—began to signal a cooling-off period. This phase was characterized by a distinct "risk-off" environment, where the annual average of stablecoin deposits dropped from $4.47 billion to $3.87 billion.

The Institutional Pivot (Q2 2026 – Present)

We are currently in the third phase of this evolution: institutional maturation. The narrative has shifted from retail speculative inflows to institutional operational requirements. With the SEC’s approval of new, actively managed crypto ETFs, stablecoins have been legitimized as treasury assets, moving beyond the confines of crypto-native exchanges.

Supporting Data and Technical Analysis

The divergence between exchange inflows and total market supply is the most compelling story in the current data. According to insights from CryptoQuant, the decline in exchange deposits does not necessarily imply a decline in the utility of these assets.

While the monthly deposits of USDT and USDC have fallen to roughly $2.9 billion, the total market cap of the sector remains robust at $315 billion. This indicates that capital is not leaving the ecosystem; it is moving to different venues. Much of this liquidity is being redirected toward:

- DeFi Yield Protocols: Stablecoins are increasingly locked in decentralized lending and liquidity provision.

- Corporate Treasuries: Businesses are using stablecoins for cross-border settlements to avoid the friction and delays of the SWIFT banking network.

- Regulated ETFs: As seen with T. Rowe Price, institutional fund managers are now utilizing stablecoins as a liquid component of their diversified portfolios.

This "stickiness" of capital suggests that the stablecoin market is maturing. It is less dependent on the immediate "buy/sell" cycle of Bitcoin and more reliant on the long-term infrastructure needs of the financial services industry.

Official Responses and Regulatory Tailwinds

The regulatory environment has been a significant catalyst for this shift. For years, the lack of a clear legal framework hindered the institutional adoption of stablecoins. However, the recent decision by the U.S. Securities and Exchange Commission (SEC) to permit the T. Rowe Price Active Crypto ETF to hold stablecoins is a watershed moment.

This approval represents an official acknowledgement that stablecoins possess sufficient liquidity and stability to serve as institutional-grade assets. By allowing these instruments within a regulated fund, the SEC has provided a stamp of approval that reduces the "reputational risk" for other major financial institutions looking to enter the digital asset space.

Furthermore, industry leaders have emphasized that the future of stablecoins lies in payment rails. As one analyst noted, "We are moving away from the era of crypto-to-crypto speculation and into the era of crypto-to-fiat efficiency." This aligns with the findings from the latest McKinsey report, which highlights that the sheer volume of real-world payments—$390 billion in 2025—is the true North Star for the stablecoin industry.

Implications for the Future

The implications of this shift are profound for both the crypto industry and the traditional banking sector.

1. Reduced Reliance on Speculative Cycles

Historically, the health of the stablecoin market was viewed as a proxy for the health of the broader crypto market. If Bitcoin was up, stablecoin inflows were high; if Bitcoin was down, stablecoins were redeemed for fiat. We are now seeing a decoupling. As stablecoins become embedded in payment infrastructure and regulated investment products, their supply will likely become less sensitive to daily price volatility in the crypto markets.

2. The Rise of "Operational Liquidity"

As businesses and institutions adopt stablecoins for settlement, the demand for these assets will become driven by operational volume rather than market sentiment. This creates a "demand floor" that protects the sector from the extreme volatility that has plagued it in the past.

3. Increased Scrutiny and Standardization

With institutional adoption comes increased pressure for transparency. The future of the market will likely be defined by a "flight to quality," where issuers who provide regular, audited proofs of reserves will capture the lion’s share of institutional demand. The era of "black box" stablecoins is likely drawing to a close.

Final Summary

The stablecoin market has proven its resilience. While the frenzied inflows of the past have slowed, the industry has successfully pivoted toward a model of sustainable, utility-driven growth. With a market capitalization of $315 billion and increasing integration into institutional investment funds and global payment systems, stablecoins have effectively graduated from their role as speculative tools.

As we look toward the remainder of 2026, the focus will likely remain on regulatory clarity and the expansion of payment use cases. For investors and developers alike, the message is clear: the stablecoin market is no longer just a feature of the crypto ecosystem—it is becoming a pillar of the global financial architecture. The volatility of the past has been replaced by the steady, albeit quiet, advancement of institutional adoption, marking the beginning of a more mature, stable, and integrated digital asset future.