Decentralization has long been the ideological bedrock of the cryptocurrency industry, promising an escape from the constraints of traditional finance (TradFi). Yet, as the industry matures, a harsh reality is coming into sharp focus: even the most decentralized digital assets are tethered to the physical world through centralized chokepoints. Nowhere is this tension more apparent than in the ongoing struggle between Tether (USDT), the world’s dominant stablecoin, and the European Union’s Markets in Crypto-Assets (MiCA) regulation.

As major exchanges purge USDT from their European offerings, the $185 billion stablecoin is facing its most significant existential test to date. This regulatory friction is not merely a bureaucratic headache; it is causing a fundamental shift in global liquidity, threatening the "risk-on" momentum that many investors hoped would carry the market through the third quarter of 2026.

The Core Facts: A Regulatory Collision Course

The tension centers on a simple mismatch: Tether’s decentralized operational model versus the European Union’s demand for transparency, capital reserves, and strict legal accountability under the MiCA framework.

MiCA, which represents the most comprehensive attempt by a major jurisdiction to regulate crypto-assets, mandates that stablecoin issuers operating within the EU must be fully authorized as electronic money institutions (EMIs). These issuers are required to hold 1:1 reserves, subject to rigorous auditing and local regulatory oversight.

Tether, maintaining its stance as a global, permissionless utility, has opted not to seek MiCA compliance. This decision has effectively turned the world’s largest stablecoin into a pariah within the European Economic Area (EEA). Consequently, major exchanges—including Binance, Coinbase, and Kraken—have initiated the mass delisting of USDT for European users to avoid legal repercussions. This move has created an immediate liquidity vacuum, forcing traders to pivot toward compliant alternatives like Circle’s USDC or Ripple’s RLUSD, which are actively seeking to bridge the gap left by Tether’s departure.

A Chronology of the Tether-MiCA Standoff

The current crisis did not happen overnight; it is the culmination of a multi-year regulatory push by the EU.

- Early 2024: As the MiCA framework neared full implementation, analysts began warning that stablecoin issuers would face a "compliance fork." Tether remained notably quiet on its intentions, prioritizing its massive presence in emerging markets over European regulatory alignment.

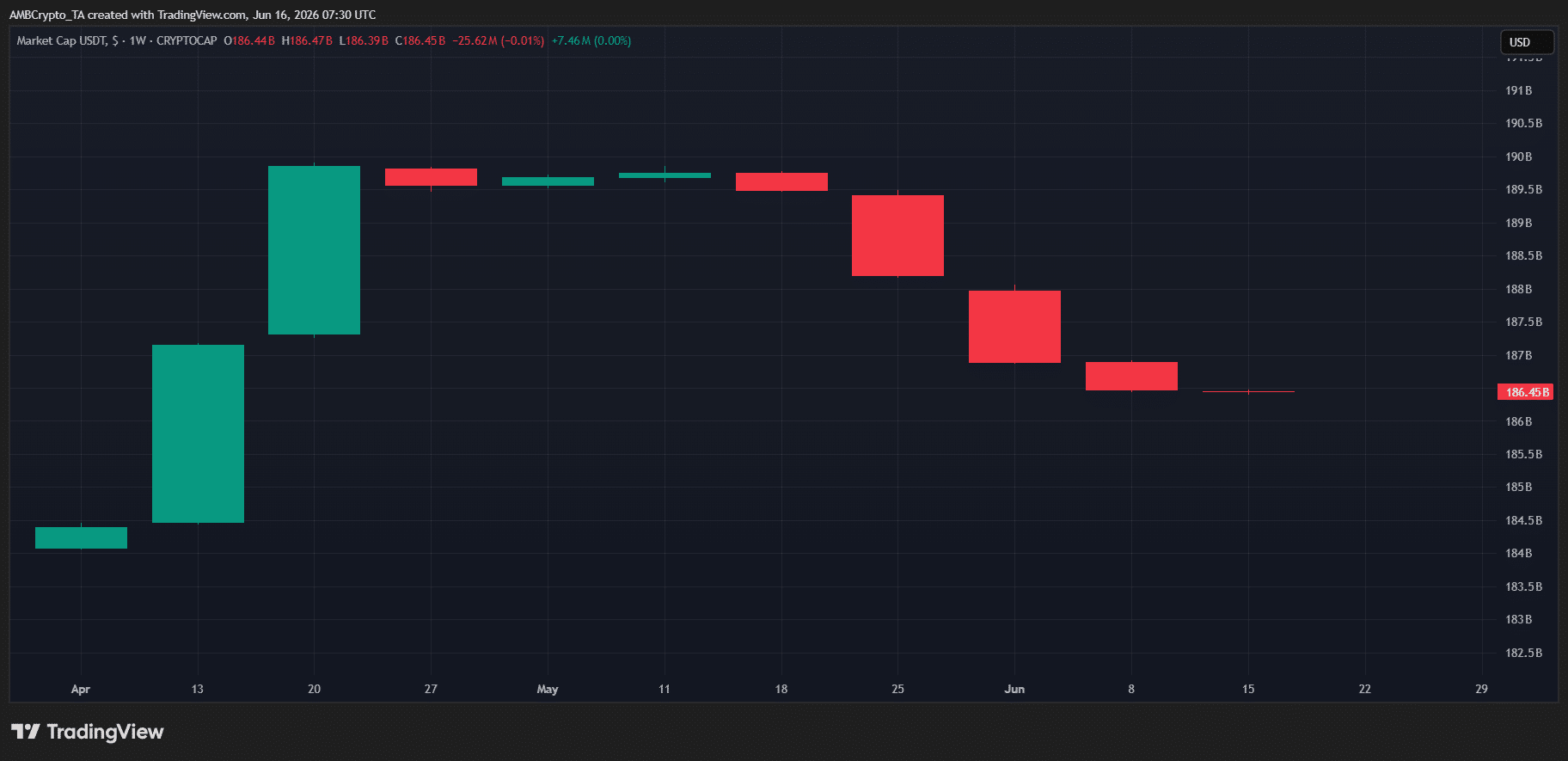

- Q1 2026: Tether’s market capitalization reached a staggering $190 billion, cementing its role as the primary lubricant for the global crypto economy.

- May 2026: The total stablecoin market cap peaked at over $321 billion. During this period, signs of regulatory tightening in the EU became unavoidable, with European regulators explicitly signaling that non-compliant stablecoins would be treated as "unauthorized financial products."

- June 2026: Following the formal enforcement phase of MiCA, major exchanges began a phased rollout of USDT delistings. This led to a sharp, immediate contraction in USDT liquidity.

- Present Day: Tether’s market cap has slipped below $185 billion, reflecting a $3 billion outflow in the last few weeks alone, as investors and market makers scramble to rebalance their portfolios in anticipation of further regulatory fragmentation.

Supporting Data: The Liquidity Contraction

To understand the severity of the situation, one must look at the flow of capital. In a bullish market, liquidity is the lifeblood of price discovery. High liquidity lowers the "slippage" costs for traders, allowing for smoother price appreciation. When liquidity is pulled from the ecosystem, volatility often increases, and price momentum becomes fragile.

Data from DeFiLlama confirms that the stablecoin sector is currently experiencing a "liquidity hangover." Despite a global pivot toward a "risk-on" environment following the easing of geopolitical tensions between the U.S. and Iran, the stablecoin market has failed to mirror this optimism. The sector is down over $6 billion from its May peak.

The rotation away from USDT is visible but uneven. While RLUSD has seen a growth of over 6.5% as it positions itself as a "compliant" alternative, USDC continues to struggle, seeing a 2.5% decline in the same period. This suggests that while capital is fleeing USDT, it is not necessarily finding a "safe harbor" in other stablecoins. Instead, it is, in some cases, exiting the crypto ecosystem entirely, returning to fiat currency. This represents a net negative for the total addressable market of the crypto space.

Official Responses and Corporate Positioning

The response from the industry has been bifurcated.

Tether, through various official statements, has characterized its decision to eschew MiCA as a protection of its core mission: serving the unbanked and providing a neutral, global currency. Tether executives have argued that the EU’s requirements would compromise the "decentralized" nature of their operations and impose unnecessary constraints that do not apply to users in Latin America, Africa, or Asia.

Conversely, issuers like Circle have leaned into the "compliance-first" narrative. By securing EMI licenses and working directly with European regulators, Circle is positioning USDC as the institutional-grade standard for the continent.

Exchanges are caught in the middle. Their official statements emphasize "regulatory adherence" and "user safety." However, behind closed doors, many exchange operators admit that the loss of USDT pairs is a significant blow to their trading volume. Tether has long been the primary quote currency for nearly every altcoin pair on the market; removing it creates a fragmented order book, which, in the short term, harms the very users the regulators claim to be protecting.

Implications: The Q3 Outlook and Beyond

The implications of the Tether-MiCA rift are profound and extend far beyond European borders.

1. The Fragmentation of Global Liquidity

We are entering an era of "Geographic Liquidity Segmentation." Instead of a single, global price for Bitcoin or Ethereum, we may see the emergence of "MiCA-compliant" price pools and "offshore" pools. This fragmentation could lead to significant arbitrage opportunities, but it also increases the complexity and cost of trading for retail participants.

2. The "Risk-On" Sentiment vs. Real-World Utility

The market’s hope for a massive Q3 rally relies on a influx of new capital. However, if the primary mechanism for entering the crypto market (USDT) is being dismantled in the world’s second-largest financial market, that capital influx will be hindered. The "FUD" (Fear, Uncertainty, and Doubt) surrounding Tether’s market cap decline is a psychological weight on the market. If investors perceive that the "base layer" of their portfolio (stablecoins) is under regulatory siege, they are less likely to rotate into more volatile risk assets.

3. The Future of Decentralization

This saga proves that while protocols can be decentralized, on-ramps and off-ramps remain centralized. If a stablecoin cannot be converted to fiat at a regulated exchange, its utility for the average consumer drops precipitously. The industry must now grapple with the reality that "permissionless" does not mean "immune to law."

Conclusion: A Bearish or Bullish Setup?

As we look toward the remainder of Q3, the setup remains precarious. If Tether can weather the current $3 billion outflow without a de-pegging event or a loss of confidence, the market may stabilize. However, if the EU’s actions trigger a "domino effect"—where other jurisdictions adopt similar stringent requirements—the era of the $185 billion, omnipresent Tether may be nearing a structural change.

For the investor, the message is clear: watch the stablecoin flows. If the aggregate stablecoin market cap begins to rise again, it indicates that capital is finding new, compliant paths into the ecosystem. If it continues to shrink, we may be facing a cooling period for crypto assets, regardless of broader geopolitical or macroeconomic improvements. The "DeFi rails" are still being built, but the tracks are increasingly being laid by those who play by the rules of the old world.